Introduction

When a business is bought, sold, merged, or restructured, the single most critical question is: "What is this actually worth?" Getting that answer wrong can cost millions or derail a transaction entirely. A single percentage point error in discount rate assumptions can swing a valuation by tens of millions. Misvalued intangible assets — brands, customer contracts, IP — lead directly to overpayment, post-close write-downs, and deal regret. In the Indian context, valuation is not just an analytical exercise — it is a legal one. Companies Act 2013 Section 247 requires a Registered Valuer for statutory valuations under schemes of arrangement, share issuances, and NCLT-supervised transactions. Income Tax Rule 11UA prescribes valuation methodology for unquoted shares under Section 56(2)(x). SEBI (SAST) Takeover Regulations dictate minimum offer price computation for listed-company acquisitions. And under FEMA, cross-border deals require Chartered Accountant or Merchant Banker valuation certification. Every India-inbound or Indo-X outbound transaction touches at least one of these frameworks.

Choosing the wrong valuation method remains one of the most common and costly errors in M&A. According to Kroll's 2025 U.S. Goodwill Impairment Study, U.S. public companies recorded $96 billion in goodwill impairments in 2024 — a 16% increase from 2023 — evidence that valuation missteps at deal close create accounting pain for years.

This guide breaks down the core valuation methods, how to apply them, and the judgment calls that determine whether a deal is priced right — or expensively wrong.

Key Takeaways

- Asset valuation determines the fair market or present value of a business's assets using structured, method-driven analysis

- Three core approaches — Cost, Market, and Income — suit different asset types and deal contexts

- No single method captures the full picture — advisors cross-check multiple approaches, especially in M&A

- Intangible assets are the hardest to value and the most likely source of error

- The valuation purpose (acquisition, due diligence, fundraising, or exit) determines which method takes priority

What Is Asset Valuation?

Asset valuation is the structured process of determining the current economic worth of a company's assets — both tangible (property, equipment, inventory, cash) and intangible (brand value, patents, customer relationships, goodwill) — using a combination of accounting data, market evidence, and financial modeling.

Two main asset categories:

- Tangible assets: Relatively straightforward to value using book values and replacement costs — machinery, real estate, inventory, receivables

- Intangible assets: Require more subjective analysis and specialist expertise — brand equity, IP, workforce, contracts, goodwill — and are often where the largest disagreements in M&A negotiations occur

Under ASC 805-20-25-10, an intangible asset is recognized separately from goodwill if it meets either the separability criterion (capable of being sold or licensed) or the contractual-legal criterion (arises from legal rights). This distinction carries material weight: intangible assets now constitute approximately 92% of S&P 500 market capitalization, a sharp reversal from 1975, when tangible assets accounted for 83% of value.

Where asset valuation is used:

- Mergers and acquisitions (buy-side and sell-side pricing)

- Business sales and exits

- Equity fundraising and growth capital raises

- Loan applications and balance sheet reviews

- Tax and estate planning

- Financial reporting (impairment testing under ASC 350, IAS 36)

- Litigation and dispute resolution

Each of these contexts calls for a different analytical approach. The purpose of the valuation directly shapes which method is appropriate — a liquidation scenario requires different assumptions and evidence than a going-concern acquisition.

The Main Methods of Asset Valuation

There are three GAAP-recognized approaches (cost, market, income) plus the asset-based approach used in specific circumstances. Each has different inputs, assumptions, and outputs. No single method is universally "correct" — the choice depends on the asset type, business model, and valuation purpose.

The Cost Approach (Book Value / Adjusted Net Assets)

This method values assets based on what it would cost to replace or reproduce them, adjusted for depreciation and obsolescence.

Adjusted net asset method walkthrough:

- Start with balance sheet book values

- Adjust each asset and liability to fair market value

- Include off-balance sheet assets (IP, workforce, contracts)

- Subtract total liabilities

When to use it:

- Asset-heavy businesses (manufacturing, real estate holding companies)

- Liquidation scenarios where the business is worth more dead than alive

- Early-stage companies with limited cash flow history

This method often represents the "floor" valuation — the minimum the business would fetch if sold for parts. It's less useful for service businesses or technology companies where value lies in intangible assets and future earnings power, not physical assets. Where the cost approach anchors on what exists today, the market approach asks what similar businesses have actually traded for.

The Market Approach (Comparables and Multiples)

This method values a business by comparing it to similar companies that have been recently sold or are publicly traded, using valuation multiples such as:

- EV/EBITDA (enterprise value to earnings before interest, tax, depreciation, amortization)

- P/E (price to earnings)

- Price-to-book

- EV/Revenue

The market approach is widely used in M&A because it reflects real market pricing — what acquirers actually paid for similar businesses. Precedent transaction analysis (looking at what acquirers paid for comparable transactions) is a key subset.

Why EV/EBITDA is preferred:

- EBITDA is a pre-interest flow to all capital providers, enabling direct comparison across companies with different debt structures

- Remains consistent across jurisdictions, making it the dominant multiple in cross-border M&A transactions

- Strips out non-cash charges and financing decisions, isolating operating performance

Critical caveat: Quality of comparables matters significantly. Mismatched peers produce misleading results. A B2B SaaS company cannot be accurately valued using consumer marketplace comparables, even if both are "tech."

The market approach tells you what the market has paid. The income approach asks what the business itself will generate — which matters most when no clean comparable exists.

The Income Approach (Discounted Cash Flow)

This method values an asset or business based on the present value of its expected future cash flows, discounted at an appropriate rate (WACC or required rate of return).

Why it matters:

- Projects value from future performance, not historical costs or peer multiples

- Captures the earning power of the business, including intangible assets

- Reflects business-specific growth and risk profiles

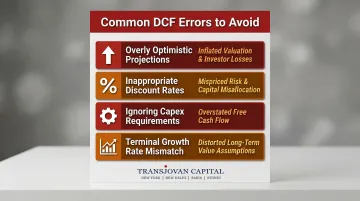

Common DCF errors to avoid:

| Error | Impact |

|---|---|

| Overly optimistic projections | Using hockey-stick growth assumptions not grounded in historical performance |

| Inappropriate discount rates | Failing to adjust WACC for company-specific risk or using equity cost of capital for unlevered cash flows |

| Ignoring capex requirements | Not accounting for reinvestment needed to sustain growth |

| Terminal growth rate mismatch | Using 5% perpetual growth rates for mature businesses instead of normalizing to GDP growth (2-4%) |

According to Wall Street Prep's analysis of common DCF errors, double counting (including affiliate income in cash flows while also including its value in net debt) and multiple mismatches (using equity multiples for enterprise value calculations) are among the most frequent technical mistakes.

When to Use Which Method

Quick decision guide:

- Cost Approach: Asset-heavy or distressed businesses; liquidation scenarios

- Market Approach: Preferred sanity check in M&A; strongest when comparable transactions exist

- Income Approach: Growing businesses with predictable cash flows; intangible-heavy businesses

In practice: Most M&A transactions run all three methods in parallel and reconcile them to arrive at a defensible valuation range, not a single number. The resulting range becomes the anchor for negotiation.

Why Asset Valuation Matters in M&A and Corporate Transactions

Asset valuation is the foundation of every pricing decision, deal structure, and negotiation in M&A — not a compliance formality. Overvaluation leads to overpaying and goodwill write-downs post-close. Undervaluation either kills a deal or hands the other side a structural advantage before negotiations begin.

Acquisition Pricing and Avoiding the Winner's Curse

Buyers who rely on a single method or fail to properly value intangible assets (customer contracts, brand equity, key workforce) routinely overpay. Research shows that between 70% and 90% of M&A deals fail to create shareholder value, with 42% of M&A failures citing overpayment as a primary cause.

The winner's curse describes the tendency for the winning bidder in a competitive auction to overpay, because they most aggressively overestimated the target's value. The data confirms it: 54% of acquirers of publicly-traded firms and 46% of acquirers of privately-held firms experience statistically significant negative abnormal announcement returns at deal close.

Due Diligence and Uncovering Hidden Liabilities

Asset valuation during due diligence must go beyond the balance sheet to identify:

- Off-balance sheet liabilities (pending litigation, regulatory obligations, contingent liabilities)

- Quality of assets (obsolete inventory, uncollectible receivables, overstated IP value)

- Overvalued intangible assets (customer churn rates that undermine relationship value)

Unrecorded liabilities and overstated assets are the most common triggers for deal renegotiation and post-close disputes.

Deal Structuring and Negotiation

Accurate asset valuation gives both buyers and sellers a defensible basis for negotiation on:

- Offer price and walk-away thresholds

- Earn-out structures and working capital adjustments

- Representations & warranties and indemnification caps

Advisors who combine M&A execution experience with financial modelling depth can stress-test assumptions before they become deal terms. Transjovan Capital's partner-led teams, having advised on over $15 billion in transactions, bring that challenge function directly to the negotiating table on behalf of clients.

Post-Merger Integration and Financial Reporting

Asset valuation continues after close. Purchase Price Allocation (PPA) assigns deal value across acquired assets and liabilities, which drives:

- Future amortization schedules

- Impairment testing requirements

- Reported earnings

Poor PPA at close creates accounting headaches for years. A Houlihan Lokey study of 5,346 M&A filings (2019–2020) found that the median allocation of purchase consideration was 47% to goodwill and 34% to identifiable intangible assets. These are not accounting line items — they directly shape reported earnings and impairment exposure for years after close.

How to Conduct Asset Valuation – A Step-by-Step Process

Asset valuation is iterative, not linear. Each step informs the next, and experienced advisors revisit earlier conclusions as new data surfaces.

Step 1 – Define the Purpose and Scope

Clarify the goal: Is this an acquisition, a fundraise, an exit, or a financial reporting exercise?

The purpose determines:

- Which methods take precedence

- Which assets to include

- What standard of value applies (fair market value, investment value, liquidation value)

Without this clarity, even a technically sound model produces results that don't serve the actual decision.

Step 2 – Identify and Classify All Assets

Catalogue all tangible assets:

- Property, plant, equipment

- Inventory

- Receivables

- Cash

Catalogue all intangible assets:

- Patents, trademarks

- Customer lists, non-compete agreements

- Brand value

- Goodwill

Include off-balance sheet assets that GAAP may not capture but that carry real economic value — assembled workforce, favorable lease agreements, regulatory approvals.

Intangible assets are the most frequently overlooked category — and in knowledge-intensive or brand-driven businesses, they often represent the majority of enterprise value.

Step 3 – Gather Data and Normalize Financials

Collect:

- Financial statements (3–5 years historical)

- Asset registers

- Contracts

- Market comparables

Normalize historical financials to remove:

- One-off items (litigation settlements, asset sales)

- Owner adjustments (above-market compensation, personal expenses)

- Non-recurring expenses

Normalization directly determines the reliability of income-based outputs. The three metrics most affected are EBITDA quality, maintainable earnings, and working capital levels — all of which buyers will scrutinize closely.

Step 4 – Apply the Appropriate Method(s)

Run the selected valuation method(s) against the prepared data.

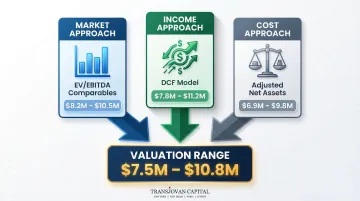

Practical example:

A mid-size industrial company would typically be valued using:

- EV/EBITDA comparables (market approach)

- DCF model (income approach)

- Adjusted net asset calculation (cost approach)

Each method produces a different number. The goal is a credible range, not false precision. The resulting range becomes the negotiation anchor.

Step 5 – Reconcile, Validate, and Stress-Test

Compare outputs across methods and investigate significant divergences.

Stress-test key assumptions:

- Discount rate (WACC): Vary by ±1% and observe impact

- Growth rate: Test conservative, base, and optimistic scenarios

- Exit multiple: Use industry range, not single point estimate

Engage independent appraisers for hard-to-value assets like real estate, specialized equipment, or IP.

A valuation that has been stress-tested is also a valuation that can be defended — in a buyer's data room, a board presentation, or a regulatory review.

Step 6 – Document and Apply the Findings

Translate the valuation into actionable decisions:

- Offer price

- Deal structure (cash vs. earn-out vs. equity)

- Walk-away thresholds

- Financial reporting entries

Asset valuations have a shelf life. Revisit them when market conditions shift, deal terms evolve, or new information surfaces during diligence. In live transactions, a three-month-old valuation can misrepresent value by a meaningful margin.

How Transjovan Capital Can Help

Transjovan Capital is a New Delhi-headquartered M&A and Corporate Development specialist founded in 2011, with offices in New York, Paris, and Sydney. The firm has advised 250+ clients on cumulative transactions worth over ₹1.25 lakh crore (~$15 billion) across four continents and was recognized as the 'Best M&A Advisory Firm in India' in 2024.

Corridor and Sector Coverage

Transjovan serves Indian mandates across all seven focus corridors — Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European — with deep coverage in 16 focus sectors: semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials. The firm supports Indian promoters and inbound foreign strategics across five customer intents: raising growth capital, executing M&A, devising corporate strategy, sales maximisation, and cross-border expansion.

Corporate Development as a Service (CDaaS)

Transjovan's proprietary CDaaS model embeds the firm as a continuous corporate development engine for acquisitive Indian enterprises — reducing CXO bandwidth burden while delivering end-to-end support from deal origination through post-merger integration. Partner-led execution by ex-Big-4 professionals and ex-CXOs averaging 20 years of experience, with focus-city coverage across Mumbai, Delhi NCR (Gurgaon, Noida), Bengaluru, Pune, Chennai, Ahmedabad, and Hyderabad.

Indian Asset Valuation Landscape (2026)

Valuation for Indian M&A operates inside a strict regulatory framework that shapes both methodology and deal timing:

- Companies Act 2013, Section 247 — appoints a Registered Valuer (RV) for all statutory valuations: schemes of arrangement (Sections 230–232), share issuances at premium, buy-backs, and NCLT-supervised transactions. The RV list is maintained by the Insolvency and Bankruptcy Board of India (IBBI).

- Income Tax Rule 11UA — prescribes methodology for valuing unquoted equity shares for tax purposes, especially under Section 56(2)(x) (deemed gift tax on receipt of shares below fair market value). Applicable in secondary sales, ESOP grants, and promoter reshuffles.

- SEBI (SAST) Takeover Regulations, 2011 — Regulation 8(2) prescribes minimum offer price as the highest of: negotiated price, volume-weighted average market price over the 60 trading days preceding the trigger, and highest price paid by the acquirer in the preceding 26 weeks. The Adani-Ambuja/ACC takeover used this framework.

- FEMA Cross-Border Valuation — foreign investment into or divestment from Indian companies requires valuation certification by a SEBI-registered Merchant Banker or a Chartered Accountant, using internationally accepted methodology. Applies to every Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridor deal with an equity leg.

- IBC 2016 — Regulation 27 — under the Insolvency Code, two Registered Valuers independently determine Fair Value and Liquidation Value of a stressed asset. The ArcelorMittal–Nippon Steel acquisition of Essar Steel at ₹42,000 crore was a landmark IBC-valuation resolution.

- Rule 8 of Companies (Registered Valuers and Valuation) Rules, 2017 — codifies valuation standards; the ICAI Valuation Standards are widely followed alongside international standards (IVS, USPAP).

Getting the applicable framework right at the outset materially changes deal timing and outcome. Advisors serving Indian mandates need fluency across all six instruments — not just DCF/comparables theory.

Frequently Asked Questions

What is asset valuation?

Asset valuation is the process of determining the fair market or present value of a company's tangible and intangible assets. It is used in M&A, fundraising, financial reporting, loan applications, and tax planning to establish what a business or its component parts are worth.

What are the main methods of asset valuation?

The three primary GAAP-recognised approaches are the Cost Approach (based on replacement or book value), the Market Approach (based on comparable transactions and multiples), and the Income Approach (based on discounted future cash flows). Most M&A advisors use all three in combination.

What is the asset-based valuation method?

The asset-based method values a company by calculating the fair market value of its total assets minus its total liabilities — including off-balance sheet items. It is commonly used for asset-heavy businesses, holding companies, or in liquidation scenarios where the "floor" value of a business is needed.

How do you calculate the value of an asset?

The formula depends on the method:

- Cost approach: Replacement or reproduction cost, less depreciation

- Market approach: Comparable sales or transaction multiples

- Income approach: Present value of future cash flows at an appropriate discount rate

How do you estimate a business's worth using sales or profit multiples?

Sales multiples (such as EV/Revenue) and profit multiples (such as EV/EBITDA) are derived from comparable public companies or recent M&A transactions in the same sector. These are applied to the target company's financials to estimate enterprise value, which is the foundation of the market approach to valuation.

What are the three important elements of asset valuation?

Three elements determine a defensible valuation:

- Asset identification: Classifying all tangible and intangible assets completely

- Method selection: Choosing the right approach based on asset type and purpose

- Assumption quality: Applying sound, supportable inputs throughout

Errors in any one of these three can distort the final output.

Who is a Registered Valuer under Companies Act Section 247?

A Registered Valuer (RV) is an individual or entity registered with the Insolvency and Bankruptcy Board of India (IBBI) as required under Section 247 of Companies Act 2013 and the Companies (Registered Valuers and Valuation) Rules 2017. RV certification is mandatory for all statutory valuations under schemes of arrangement (Sections 230–232), share issuances at premium, buy-backs, mergers, and NCLT-supervised transactions. RVs must belong to a Registered Valuer Organisation (RVO) and hold specific asset-class registration (Securities/Financial Assets, Plant & Machinery, or Land & Building).

What is Rule 11UA valuation in Indian income tax?

Income Tax Rule 11UA prescribes methodology for valuing unquoted equity shares of Indian companies for tax purposes. It is invoked most commonly under Section 56(2)(x) — the deemed gift-tax provision applicable when shares are received at less than fair market value. Rule 11UA(2) allows two methods: (a) Net Asset Value (NAV) method using audited balance sheet, or (b) Discounted Cash Flow (DCF) method certified by a Merchant Banker or Chartered Accountant. Selection of method materially affects tax exposure in secondary sales, ESOP allotments, promoter share transfers, and M&A share swaps.

How does SEBI (SAST) valuation differ from FEMA valuation for cross-border deals?

The two apply in different contexts and often simultaneously. SEBI (SAST) Regulation 8(2) governs the minimum offer price in open offers triggered by 25%+ acquisitions in listed Indian companies — computed as the highest of negotiated price, 60-day VWAP, and 26-week highest acquisition price. FEMA valuation applies whenever a non-resident buys or sells shares in an Indian company (regardless of listing status) — requires certification by a SEBI-registered Merchant Banker or Chartered Accountant using internationally accepted methodology (typically DCF or Comparable Companies). For a cross-border acquisition of a listed Indian company by a foreign strategic, both apply: SEBI SAST governs the offer price to public shareholders; FEMA governs the certified transaction price for regulatory reporting.