Introduction

Most acquisitions never deliver their promised value. Research shows 70–90% of M&A deals fail to create shareholder value, with 83% actively destroying investor returns. For Indian acquirers, buy-side M&A is shaped by a unique regulatory topology. SEBI (SAST) governs public-company acquisitions (25% threshold triggers an open offer). Companies Act 2013 Sections 230–232 govern schemes of arrangement requiring NCLT approval. IBC 2016 enables acquisition of stressed assets through resolution plans. FEMA dictates FDI routing (automatic vs approval) for foreign targets. CCI merger notification thresholds (₹1,000 crore asset / ₹3,000 crore turnover) add 30–120 days for clearance. Every buy-side deal in India navigates at least three of these — often all five for Indo-X cross-border acquisitions.

The gap between failure and success isn't random. First-time acquirers succeed only 23% of the time. Serial acquirers hit 54% — and generate 9.6% annual total shareholder returns versus 2.7% for inactive peers.

This guide is for corporate development heads, strategy executives, and senior leaders at acquisitive enterprises evaluating or actively pursuing growth through acquisition. Whether you're building a programmatic M&A capability or executing your next deal, the difference between value creation and value destruction comes down to process discipline.

This guide covers the buy-side M&A process from start to finish:

- How to define acquisition strategy and target criteria

- What rigorous target screening and due diligence looks like

- How valuation and negotiation shape deal outcomes

- Where post-merger integration determines whether value is actually captured

Key Takeaways

- Buy-side M&A is the process by which a company identifies, evaluates, and acquires another business to achieve strategic or financial objectives

- The process runs from acquisition strategy and target screening through due diligence, valuation, negotiation, and post-close integration

- Due diligence and valuation are the most critical stages for protecting deal value and preventing overpayment

- Most deals fail due to overpayment under competitive pressure or integration that never delivers the projected synergies

- Specialized buy-side advisors bring deal flow, valuation discipline, and execution depth that most internal teams lack

What Is Buy-Side M&A?

Buy-side M&A is the acquisition side of a transaction, where the buyer seeks to purchase a majority or full ownership stake in a target company. This contrasts with sell-side M&A, where advisors focus on maximizing valuation for the seller.

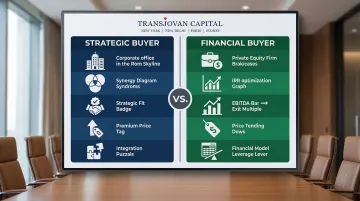

Two distinct buyer types pursue acquisitions, each with different priorities:

| Strategic Buyers | Financial Buyers | |

|---|---|---|

| Who | Corporations | Private equity firms |

| Primary goal | Synergies, market share, new capabilities | IRR optimization within a defined hold period |

| Valuation basis | Strategic fit and competitive positioning | Cash flow, EBITDA growth, exit multiples |

| Premium paid | Higher — operational synergies justify it | Lower — returns depend on leverage and discipline |

| Diligence focus | Integration readiness, capability gaps | Financial model, cost structure, leverage capacity |

These different motivations fundamentally shape how buyers approach valuation, structure diligence, and plan integration. Where a strategic buyer asks "does this strengthen our position?", a financial buyer asks "what does this return in five years?"

Clarity on which type of buyer you are — and what success looks like — shapes every decision in the buy-side process, from target screening through to post-close integration.

Why Companies Pursue Buy-Side M&A

Corporate leaders turn to acquisitions when organic growth cannot match the speed or scale required to meet strategic objectives.

Core strategic drivers include:

- Compress years of market development into immediate presence through acquisition

- Buy proprietary technology or talent that would take too long to build internally

- Enter new geographies with an established local footprint rather than starting from zero

- Consolidate fragmented industries through roll-ups to gain scale advantages

- Control supply chains or distribution channels to reduce cost and protect margin

Typical acquisition triggers:

- A competitive threat demands a faster response than organic growth allows

- A fragmented industry creates a clear consolidation window

- Inorganic growth targets require a formal deal pipeline

- A strategically ideal target becomes available before a competitor moves first

The scale of buy-side M&A activity reflects its strategic importance. Global M&A deal value surged approximately 40% in 2025 to $4.9 trillion, driven by corporate buyers aggressively pursuing inorganic growth. 41% of global CEOs plan to undertake a major acquisition within the next three years — the pipeline of intent is as strong as the deal volumes suggest.

The Buy-Side M&A Process: A Step-by-Step Overview

The buy-side M&A process is sequential but iterative. Timelines vary from months to years depending on deal complexity, cross-border considerations, and regulatory requirements. Skipping or rushing any phase materially increases deal risk.

Notably, the average time from signing to close for deals over $2 billion has stretched to 191 days, with 40% of transactions missing their announced closing windows due to regulatory complexity.

Step 1: Defining Acquisition Strategy and Criteria

Acquisition criteria must specify industry, company size, geography, financial thresholds (revenue range, EBITDA minimum), and strategic fit parameters. Vague criteria leads to wasted pipeline effort and misaligned targets.

Effective criteria answer:

- Which markets or capabilities are we targeting?

- What size targets can we realistically integrate?

- What financial metrics (revenue, EBITDA, growth rate) define our range?

- What strategic attributes are non-negotiable (IP ownership, customer base, geographic presence)?

Step 2: Target Identification and Screening

A long list of potential targets is built through market research, industry databases, and advisor networks, then narrowed through preliminary financial and strategic analysis.

Sourcing channel matters. 39% of closed deals come through proprietary off-market channels, avoiding the inflated premiums that competitive auctions generate. Another 36% come through limited auctions with select buyers, while only 25% result from broad-based processes. Buyers with strong proprietary networks consistently pay less and close faster.

Step 3: Initial Approach and Relationship Building

A direct "is your company for sale?" approach is counterproductive. Effective advisors frame outreach around exploring a "strategic partnership" or "complementary working relationship."

Early dialogue serves multiple purposes:

- Assesses management culture and seller motivations

- Builds trust before formal negotiation begins

- Identifies potential deal structures that align buyer and seller interests

- Surfaces potential obstacles (key-man dependency, family ownership dynamics, regulatory concerns)

Step 4: Due Diligence

Due diligence verifies the financial, legal, operational, and cultural integrity of the target. It covers quality of earnings, contract risk, people dependencies, regulatory exposure, and integration feasibility — typically running 6–12 weeks for mid-market deals.

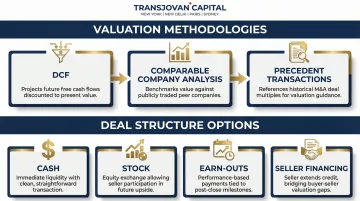

Step 5: Valuation, Deal Structuring, and Closing

Valuation employs multiple methodologies:

- Discounted Cash Flow (DCF) – Projects future cash flows and discounts to present value

- Comparable Company Analysis – Benchmarks against similar publicly traded companies

- Precedent Transactions – References recent acquisitions of similar businesses

Valuation sets the ceiling; deal structure determines how risk and reward are distributed between buyer and seller:

- Cash – Clean, immediate transfer but requires capital deployment

- Stock – Aligns seller with acquirer's future performance

- Earn-outs – Defers payment based on post-close performance targets

- Seller financing – Demonstrates seller confidence in business sustainability

Running regulatory filings in parallel with negotiation — rather than sequentially — is what separates deals that close on schedule from those that drag. For transactions above $1 billion, antitrust review alone accounts for a significant share of the 191-day average close window.

Due Diligence and Valuation: Where Deals Are Won or Lost

Due diligence is the make-or-break phase. It validates assumptions underpinning the acquisition rationale, surfaces hidden liabilities, and establishes the data foundation for final pricing. Deals that compress or skip this phase consistently underperform.

Financial Due Diligence: EBITDA Normalization

Financial diligence requires rigorous verification of revenue quality, EBITDA normalization, working capital dynamics, off-balance sheet liabilities, and customer concentration.

Critical focus areas:

| Adjustment Category | What to Verify |

|---|---|

| One-Time Items | Restructuring charges, legal settlements, system implementation costs, COVID relief funds |

| Non-Cash Transactions | Stock compensation, capitalized costs, impairment charges, unrealized gains/losses |

| Out-of-Period Items | Changes in estimates, year-end adjustments, revenue recognition shifts |

| Pro-Forma Run-Rate | Recent acquisition impacts, discontinued operations, stand-alone costs for carve-outs |

The difference between reported EBITDA and adjusted EBITDA directly impacts pricing. A target reporting $10 million EBITDA might show only $7 million normalized EBITDA after adjusting for one-time benefits and unsustainable margins—a gap that fundamentally changes valuation.

Legal and Operational Due Diligence

Legal and operational diligence reviews contracts, IP ownership, pending litigation, regulatory compliance, key-man dependency, and supply chain vulnerabilities. Each can materially alter deal terms or become post-close liabilities.

Key areas include:

- Contract review – Customer contracts, supplier agreements, lease terms, change-of-control provisions

- IP ownership – Patent validity, trademark registrations, licensing agreements, employee IP assignment

- Regulatory compliance – Industry-specific regulations, environmental permits, data privacy compliance

- Organizational structure – Key-man risks, management depth, employee retention concerns

- Operational infrastructure – IT systems, manufacturing capacity, supply chain resilience

Cultural Due Diligence: The Most Commonly Skipped Element

Cultural due diligence is the most frequently overlooked aspect of M&A, and statistically one of the most expensive omissions. Approximately 30% of M&A deals fail to achieve financial targets specifically due to cultural misalignment, with 44% of M&A leaders citing cultural friction as the top integration hurdle.

These risks rarely surface through contract reviews or financial models. Cultural diligence must move beyond vague notions of "values" to assess concrete management practices:

- Decision-making processes (centralized vs. decentralized, data-driven vs. intuition-based)

- Performance management systems (individual vs. team-based, short vs. long-term incentives)

- Communication norms (formal vs. informal, transparent vs. hierarchical)

- Risk tolerance (innovative vs. conservative, aggressive growth vs. steady optimization)

Identifying these differences before closing allows buyers to plan integration approaches that preserve value-creating aspects of the target's culture while aligning critical operational elements.

Buy-Side Valuation Discipline

Buy-side valuations carry a different mandate than sell-side work: they must account for synergy realization timelines, integration costs, and the acquirer's required return on invested capital — not just justify the highest defensible price.

The synergy trap: Roughly 70% of merging companies announce higher synergy estimates than realistic. Overestimating revenue synergies is one of the most cited reasons for deal failure. This overestimation fuels overpayment and sets the stage for future write-downs.

Disciplined buyers counter this by:

- Assign probability-weighted values to synergies based on difficulty and timeline

- Separate "Day 1" synergies from those requiring 12-24 months to realize

- Factor integration costs as offsets to gross synergy value

- Apply conservative realization percentages (60-70% for cost synergies, 30-50% for revenue synergies)

Common Challenges That Derail Buy-Side M&A Deals

Overpayment: The Synergy Trap

Competitive bidding dynamics and synergy overestimation lead buyers to exceed defensible price levels. The financial impact is staggering: in 2024, total goodwill impairments in the U.S. increased approximately 16%, jumping from $83 billion to $96 billion.

These write-downs reflect acquisitions where buyers paid premiums for synergies that never materialized — a pattern that repeats when deal pressure overrides valuation discipline.

Warning signs of overpayment:

- Valuation relies heavily on revenue synergies (historically the hardest to realize)

- Synergy estimates lack detailed implementation plans or timelines

- Purchase price exceeds comparable transaction multiples without clear justification

- Competitive pressure drives price above initial walk-away threshold

Integration Failure: The 83% Problem

When deals fail to deliver value, the root cause is rarely the strategic rationale—it's almost always execution. Fully 83% of M&A practitioners who have experienced a failed deal point to problems in post-close integration as the primary cause.

Integration planning cannot wait until signing. Acquirers who start during due diligence — by establishing an Integration Management Office (IMO) — consistently outperform those who begin after close. The IMO's mandate includes:

- Confirms ability to integrate systems, processes, and organizations

- Identifies pivotal decisions requiring immediate attention post-close

- Prepares Day-1 operational readiness plans

- Defines KPIs and synergy tracking mechanisms

- Establishes clear ownership and accountability for integration workstreams

What happens in the first 100 days post-close largely determines the outcome. Without structured governance, organizational drift, employee attrition, and operational disruption erode deal value before synergies have any chance to materialize.

Cross-Border and Regulatory Complexity

Cross-border acquisitions add layers of complexity including foreign investment screening, currency exposure, and jurisdictional compliance.

Key regulatory frameworks:

| Jurisdiction | Regulatory Body | Key Requirements |

|---|---|---|

| United States | CFIUS | Mandatory declarations for foreign acquisitions involving critical technologies or substantial government contracts |

| European Union | DG COMP | Notification required when combined worldwide turnover exceeds €5B with €250M EU-wide turnover for at least two firms |

| India | DPIIT / RBI | Investments from countries sharing land borders with India require prior government approval |

Navigating these frameworks adds months to deal timelines when managed reactively. Cross-border acquirers reduce that risk by engaging advisors with market-specific regulatory experience early — before term sheets are submitted, not after clearance delays emerge.

What to Look for in a Buy-Side M&A Advisor

A specialized buy-side advisor adds capabilities most internal corporate development teams can't replicate. Proprietary deal flow from industry networks, independent valuation benchmarking, and negotiation expertise are table stakes. The real differentiator is protecting senior management bandwidth — keeping your leadership focused on running the business while the deal gets done.

Key Selection Criteria

When evaluating advisors, press on four areas:

- Industry depth: Ask for completed transactions in your specific sector. Advisors without it will miss value drivers, misread regulatory risk, and negotiate from a weaker position.

- On-the-ground presence: Cross-border deals require physical presence in target markets — not just familiarity. Regulatory frameworks and business practices in India, APAC, Europe, and the US differ enough that remote advisory creates blind spots.

- Partner-led execution: Confirm that senior professionals lead the mandate. If the pitch team won't be running the deal, that's a red flag worth surfacing early.

- Verifiable deal history: Request specifics — off-market targets sourced, deal structures negotiated, synergies realized post-close. Volume of transactions is less useful than evidence of outcomes at similar scale and complexity.

The Corporate Development as a Service (CDaaS) Model

CDaaS is a structural alternative to one-off transactional advisory. It embeds a continuous corporate development function alongside the acquirer's leadership over multiple years — managing live pipeline, running target screening, and executing mandates without the overhead of a full in-house team.

CDaaS typically includes:

- Ongoing strategic advisory on capital allocation and growth priorities

- Continuous pipeline management across multiple concurrent deals

- Sustained post-merger integration oversight

- Multi-deal execution without rebuilding context for each transaction

- Joint venture evaluations and integrations

- Annual portfolio reviews to assess acquisition performance

Firms like Transjovan Capital offer this model for large acquisitive enterprises seeking end-to-end M&A support across the US, Europe, India, and APAC — without building a full in-house function.

Over time, a multi-year engagement compounds in value: advisors internalize the acquirer's strategic logic, organizational constraints, and sector dynamics. That institutional knowledge translates directly into sharper target identification and faster diligence cycles on each successive deal.

Warning Signs in Advisor Selection

Three patterns signal misaligned incentives before a mandate begins:

| Warning Sign | What It Signals |

|---|---|

| Fee-on-close only (no retainer) | Advisor is incentivized to close — not to protect your valuation |

| Success measured by deal count | Transaction volume is the goal, not synergy capture |

| No physical presence in target markets | Cross-border deals need local intelligence; remote advisory creates blind spots |

When any of these appear, probe deeper before signing an engagement letter. Incentive misalignment tends to surface at the worst possible moment — usually during negotiations, when it's too late to course-correct.

Indian Buy-Side M&A Landscape (2026)

Every Indian buy-side transaction sits inside a defined regulatory pathway that shapes deal timing, cost, and structure:

- SEBI (SAST) Regulations, 2011 — any acquisition crossing 25% of voting rights in a listed Indian company triggers a mandatory open offer for an additional 26% at a regulator-computed minimum price. The Adani group's takeover of Ambuja Cements/ACC followed this framework post-Holcim exit.

- Companies Act 2013, Sections 230–232 — mergers, demergers, and schemes of arrangement require NCLT approval, creditor consent, and shareholder resolutions. The HDFC Ltd–HDFC Bank merger, India's largest with ₹40 lakh crore combined balance sheet, was executed under Section 230.

- IBC 2016 — the Insolvency and Bankruptcy Code is a major buy-side channel for stressed-asset acquisitions. The ArcelorMittal-Nippon Steel acquisition of Essar Steel at ₹42,000 crore (Indo-Japan-European trilateral) set the template for foreign-consortium bids.

- FEMA and FDI Regime — cross-border buy-side transactions involve automatic or approval-route FDI depending on sector and stake. Sensitive sectors require government approval; construction, manufacturing, and most services are under automatic route across all seven Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian corridors.

- CCI Merger Notification — pre-transaction clearance is required when either the target or combined entity exceeds ₹1,000 crore in Indian assets or ₹3,000 crore in Indian turnover; Phase I/II review adds 30–120 days.

- Section 47 of Income Tax Act — provides tax-neutrality for qualifying mergers, demergers, and slump sales — critical for structuring cross-border and domestic acquisitions.

Indian acquirers pursuing outbound Indo-US or Indo-European deals additionally navigate US CFIUS, EU merger control, and Japanese FEFTA — pairing an Indian advisor with a global bulge-bracket has become the standard model for such mandates.

Frequently Asked Questions

What is buy-side M&A?

Buy-side M&A refers to the process by which a company, investor, or private equity firm acquires another business. The buyer's goal is strategic growth, synergy realization, or financial return through ownership of the target company.

What is the difference between buy-side and sell-side in M&A?

The buy-side represents the acquiring party focused on identifying targets and maximizing deal value through acquisition. The sell-side represents the company being sold, focusing on marketing the business and maximizing valuation for the seller.

What is the difference between a buy-side advisor and a sell-side advisor?

A buy-side advisor works exclusively for the acquirer—sourcing targets, conducting diligence, and structuring deals to protect buyer value. A sell-side advisor works for the seller, preparing the business for sale and running a process designed to attract the highest possible offer.

What is the average buy-side M&A fee?

Buy-side advisory fees typically include a retainer and a success fee calculated as a percentage of deal value. Fee structures range from 3-6% for deals between $10 million and $25 million, down to 1-2% for transactions exceeding $100 million. Monthly retainers typically range from $5,000 to $50,000 and are usually credited against the final success fee at closing.

What are the 4 P's of due diligence?

The 4 P's framework evaluates four dimensions of a target company:

- People — management quality and key-man risk

- Performance — financial health and growth trajectory

- Processes — operational efficiency and scalability

- Positioning — competitive standing and market dynamics

What triggers SEBI takeover regulations in an Indian buy-side deal?

The SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 — the SAST or Takeover Code — trigger when any acquirer crosses 25% of voting rights in a listed Indian company. The trigger obligates the acquirer to make an open offer to public shareholders for an additional 26%, at a minimum price computed under Regulation 8(2) (highest of negotiated price, 60-day VWAP, and 26-week highest price). Existing promoters can incrementally acquire up to 5% per financial year (creeping acquisition), subject to a 75% overall cap. Any change in control — regardless of stake size — also triggers an open offer. Advisors typically model 15–30% price premium for the open-offer leg when planning listed-company acquisitions.

How do IBC acquisitions differ from open-market buy-side M&A in India?

Under the Insolvency and Bankruptcy Code (IBC), 2016, buy-side acquisitions of stressed Indian companies happen through a Resolution Plan approved by the Committee of Creditors (CoC) and the NCLT (National Company Law Tribunal). Key differences from open-market M&A: (1) the target is under moratorium, so competing suitors bid via structured resolution proposals rather than negotiated deals; (2) two Registered Valuers independently determine Fair Value and Liquidation Value; (3) haircuts on creditor claims are typical; (4) the resolution plan must be approved by 66%+ of the CoC by voting share; (5) prior existing management is typically replaced. Notable IBC acquisitions include ArcelorMittal-Nippon's ₹42,000 crore acquisition of Essar Steel and Tata Steel's acquisition of Bhushan Steel.

Which Indian M&A advisor is best for a ₹500-crore mid-market buy-side mandate?

For a ₹500-crore (~$60M) mid-market Indian buy-side mandate, the best-fit advisors depend on sector, target geography, and structural complexity. Domestic full-service banks — Kotak Mahindra Capital, ICICI Securities, Axis Capital, JM Financial — anchor scaled buy-side execution with integrated ECM support. Sector-focused boutiques like Avendus Capital lead in consumer, tech, and healthcare buy-side. For Indo-X cross-border acquisitions with embedded CDaaS support across the 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials), Transjovan Capital serves Indian acquirers pursuing Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridor deals. Partner-led execution, sector track record, and regulatory fluency (SEBI SAST, Companies Act, IBC, FEMA, CCI) matter more than league-table position at this deal size.