Introduction

Corporate acquirers in construction face a compounding challenge: deal competition is rising, labor is scarce, and the window for disciplined acquisitions is narrowing. India's infrastructure management M&A expanded to 31 deals worth USD 2.8 billion in 2025, with volumes surging 82% year-over-year as asset monetisation, PPP frameworks and rising private capital participation drew capital into the sector. Real estate ran alongside it at 53 deals, nearly double the 28 recorded in 2024, forcing buyers to reframe M&A as essential capability acquisition, not just market-share expansion. For Indian construction M&A, the regulatory pathway is distinctive across sub-segments. SEBI SAST applies to listed construction majors (Larsen & Toubro, UltraTech, Shree Cement, Ambuja Cements, DLF, Godrej Properties, Oberoi Realty). RERA (Real Estate Regulatory Authority) compliance transfers with real-estate targets (RERA registrations, project completion timelines, escrow accounts). Environmental Clearance under EIA Notification 2006 transfers with construction projects, requiring re-notification for capacity expansion. CCI merger notification applies for combined turnover above ₹3,000 crore in India, common in cement and construction roll-ups. FEMA 100% automatic-route for construction and real-estate development (subject to lock-in and completion norms).

This update examines the macro demand catalysts driving deals—principally data center construction, which surged to $77.7 billion in 2025 starts—alongside who is buying, at what price, and what variables acquirers must evaluate before committing capital.

For the first time, private equity buyers now represent the majority of construction M&A activity and are paying premium multiples. Corporate acquirers that fail to recalibrate both valuation expectations and due diligence priorities will find themselves consistently outbid.

Key Takeaways

- Construction Services M&A hit 562 transactions in 2025—up 18.2% YoY—marking three consecutive years of volume growth fueled by PE consolidation

- Data center construction starts surged 190% YoY to $77.7B, with costs topping $1,033/sq ft and driving sustained contractor backlog demand

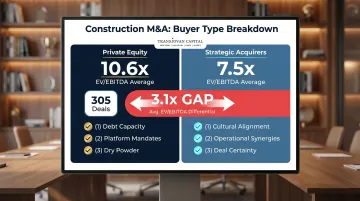

- PE buyers now hold 50%+ of construction M&A deal share, outbidding strategics at 10.6x vs. 7.5x EV/EBITDA

- Subcontractor M&A rose 38.6% YoY, capturing 65.1% of all deals as buyers target skilled workforce capacity over revenue multiples

- Sound diligence means reconstructing margins at the project level—backlog conversion risk, cash flow, and workforce depth matter as much as headline EBITDA

Construction M&A Activity in Early 2026: The Market Pulse

Construction Services M&A totaled 562 transactions in 2025, representing 18.2% growth over 2024 and marking the third consecutive year of expansion. This sustained momentum reflects structural factors that have made construction a magnet for acquirer capital since 2022: severe skilled labor shortages forcing inorganic workforce acquisition, fragmented market structure offering roll-up opportunities, and exposure to high-growth end markets like data centers and energy infrastructure.

These structural tailwinds held even as macroeconomic headwinds intensified—including tariff-driven input cost inflation (construction material costs rose 3.3% year-over-year by December 2025), persistent labor constraints, and elevated financing costs. Rather than suppressing deal activity, those pressures accelerated consolidation as a response strategy for scale.

Buyers recognized that achieving operational efficiency and securing scarce talent required acquiring capabilities and workforce, not betting on near-term revenue growth alone.

Total U.S. construction spending ended 2025 at a seasonally adjusted annual rate of $2,190.4 billion, holding steady despite input cost pressures. Deal volume and construction spending can diverge because M&A activity reflects acquirers buying future capacity and specialized expertise, not necessarily current market expansion.

That distinction matters. With over 91.9% of firms reporting difficulty filling hourly craft positions, buyers are paying for immediate access to skilled superintendents, project managers, and field labor.

Subcontractor M&A: The New Frontline

The subcontractor segment recorded 366 transactions in 2025, a 38.6% year-over-year increase, propelling subcontractors to 65.1% of all Construction Services M&A. Labor acquisition—not just capability expansion—is now the primary motive. Private strategic and sponsor-backed buyers together represented the majority of subcontractor segment deals, with residential and data center/power infrastructure subcontractors receiving disproportionate buyer interest.

Why subcontractors dominate deal flow:

- MEP subcontractors hold specialized labor that cannot be hired at scale in the open market

- Data center work demands MEP credentials and security clearances that take years to build organically

- Residential subcontractors offer recurring revenue and geographic density tied to the housing demand pipeline

- Workforce depth in subcontractors delivers immediate project staffing capacity that general contractors cannot replicate quickly

What's Fueling Construction M&A: Key Demand Catalysts

Data center construction has emerged as the single most powerful demand catalyst. Total U.S. data center construction starts reached $77.7 billion in 2025, a 190% increase from the previous year, with average costs surpassing $1,033 per square foot. This surge creates sustained contractor backlog visibility—a critical variable in acquirer underwriting confidence. When contractors hold multi-quarter backlogs with creditworthy hyperscaler customers, buyers gain earnings predictability that justifies premium valuations.

AI-driven power infrastructure is the ripple effect. U.S. data centers consumed substantially more grid power year-over-year, and projections suggest data center power demand could nearly triple by 2030. This is triggering investments in renewable energy plants, grid upgrades, and related construction—all generating new M&A targets.

Acquirers targeting contractors with master service agreements with hyperscalers or utility-scale infrastructure credentials are positioning for multi-year tailwinds.

Geographic concentration drives targeted acquisitions:

| Top U.S. States | 2025 Data Center Spending | Strategic Implication |

|---|---|---|

| Louisiana | $12.5 billion | Leading frontier market |

| Virginia | $7.4 billion | Traditional hub expansion |

| Mississippi | $6.0 billion | Emerging power-rich market |

| Texas | $5.7 billion | Projected to overtake Virginia by 2030 |

| Arizona | $2.6 billion | Western regional hub |

Acquirers are using this geographic data to target bolt-on acquisitions in high-density markets, prioritizing contractors with existing customer relationships and regulatory approvals in these states.

Industrial Reshoring and Infrastructure Maintenance Demand

Beyond data centers, three additional demand drivers are generating durable contractor acquisition targets across multiple geographies: industrial reshoring to the U.S., deferred maintenance backlogs across transportation and utility infrastructure, and energy transition capital expenditures. These tailwinds are globally distributed, making them particularly relevant to cross-border acquirers.

Key data points by region:

- United States: Manufacturing nearshoring and infrastructure maintenance cycles are expanding contractor demand beyond coastal tech corridors

- Europe: €584 billion in grid investments are required by 2030 to meet REPowerEU objectives, creating sustained demand for electrical and civil contractors

- India: The PM Gati Shakti National Master Plan has sanctioned 300 railway projects spanning 13,808 km over three years, anchoring a multi-decade logistics infrastructure build-out

These government-backed capex cycles create parallel acquisition opportunities across the US, Europe, India, and APAC. Transjovan Capital's cross-geography coverage—with active advisory presence in New York, New Delhi, Paris, and Sydney—enables acquirers to source and evaluate targets across all four of these markets within a single mandate framework.

Buyer Profiles, Valuations, and Deal Structures

For the first time, private equity buyers accounted for 54.3% of construction M&A transactions in 2025, driving 305 deals. Structural reasons made construction attractive to PE at this scale: fragmented sector landscape offering roll-up platforms, recurring service revenues with predictable cash flows, exposure to high-growth markets like data centers, and LP pressure to deploy elevated dry powder balances.

PE firms paid an average of 10.6x EV/EBITDA between 2018 and 2025, compared to strategics' 7.5x average — a three-turn gap (roughly 3x EBITDA higher) driven by debt financing capacity, platform build mandates, and intense competition for quality assets. Corporate acquirers cannot close that gap on price. To win competitive auctions, strategics need to lead on:

- Cultural alignment and management retention commitments

- Operational synergies that PE platforms cannot replicate

- Speed and deal certainty (fewer financing contingencies)

Recent transactions illustrate current structures and pricing:

- Dycom Industries / Power Solutions: Dycom acquired Power Solutions for $1.95 billion (approximately $1.64 billion cash plus stock), representing approximately 9.7x trailing four-quarters Adjusted EBITDA

- Legence / The Bowers Group: Legence acquired mechanical contractor Bowers for approximately $475 million ($325 million cash, $100 million stock, $50 million deferred consideration), implying 6.6x EV/EBITDA

Deal structures in construction M&A are more complex than in other sectors because execution uncertainty runs high. Earn-outs tied to backlog conversion, escrow provisions for warranty/safety exposure, and management rollover equity are standard mechanisms — tools for realistic risk allocation, not signs of weak conviction.

These mechanics are shifting in measurable ways:

- Earn-outs fell to 18% in 2025 (down from 26% in 2023), as buyers move away from post-close disputes over backlog conversion

- Representations and Warranties Insurance (RWI) reached 63% adoption in 2025, now the default risk mitigation tool

- 58% of transactions require separate escrow for purchase price adjustments, reflecting working capital volatility

Buy-Side Diligence in Construction: What Disciplined Acquirers Examine

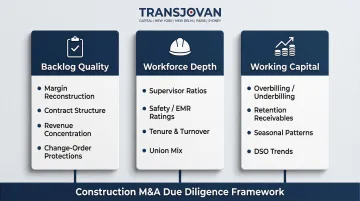

Construction EBITDA is rarely taken at face value. Experienced buy-side advisors reconstruct margins at the project level to assess whether recent profitability reflects sustainable execution or a temporary confluence of favorable factors—deferred maintenance spend, pricing power from capacity constraints, or favorable project timing. Buyers must scrutinize backlog quality, not just size: contract structure, customer concentration, bid assumptions, and change-order protections determine whether backlog converts into earnings or disappointment.

Critical diligence variables acquirers must assess:

- Strip out one-time favorable project mix and reconstruct normalized margins

- Analyze contract structure, payment terms, and historical conversion rates from backlog to revenue

- Assess revenue concentration risk and customer creditworthiness

- Review contract provisions allowing cost recovery for scope changes

Labor is the dominant diligence variable in 2026. With over 92% of contractors experiencing hiring difficulties, buyers must assess workforce depth (not just headcount), supervisor dependency, safety performance, and the company's ability to staff incremental work. Platforms that appear scalable on paper but rely on a founder or a handful of superintendents carry material execution risk that financial models can obscure.

Workforce assessment checklist:

- Evaluate supervisor-to-crew ratios and key person dependency

- Review safety performance: OSHA incident rates and EMR ratings

- Examine workforce tenure and turnover rates

- Assess recruiting pipeline and training programs

- Understand union vs. non-union labor mix and scheduling flexibility

Working capital discipline has become a decisive factor. Billing cadence, change-order timing, retention exposure, and seasonal cash flow swings can materially affect leverage capacity and downside protection. Buyers should assess cash conversion consistency, not just EBITDA margins.

Working capital variables to examine include:

- Overbilling and underbilling positions relative to project completion

- Retention receivables and expected collection timing

- Seasonal cash flow patterns and peak working capital requirements

- DSO trends and billing cycle discipline

For acquirers without dedicated internal construction M&A capacity, diligence gaps in any of these areas can erode deal value before close. Transjovan Capital's Corporate Development as a Service (CDaaS) model addresses this directly: an embedded team of ex-Big-4 advisors and former CXOs covers diligence execution, day-1 readiness, and synergy governance without adding to leadership bandwidth. The model is structured for large enterprises running multiple construction-sector acquisitions annually.

2026 Outlook: Where Opportunity Is Concentrating

Sub-sectors generating outsized acquisition interest through 2026:

- Data center and power infrastructure construction contractors, particularly those with master service agreements with hyperscalers

- Mechanical and electrical subcontractors with data center credentials, security clearances, and specialized MEP capabilities

- Energy transition construction businesses focused on renewable energy plants and grid infrastructure

- Residential subcontractors positioned for housing demand recovery as mortgage rates moderate

Geographic concentration will continue driving deal flow. Certain U.S. states—Louisiana, Virginia, Texas, Mississippi, and Arizona—will attract disproportionate buyer activity due to data center and infrastructure density.

Cross-border opportunities are equally pronounced. India's accelerating infrastructure buildout (driven by the PM Gati Shakti National Master Plan and National Infrastructure Pipeline, outlining $2,227.6 billion in project costs) and Europe's €584 billion REPowerEU grid modernization initiative are creating parallel acquisition opportunities for globally-minded acquirers.

Risks that could temper activity:

- Sustained tariff-driven input cost inflation squeezing contractor margins

- Mortgage rate headwinds on residential construction if rates rise from current levels

- Macroeconomic volatility disrupting project financing and customer capex

PE firms sitting on elevated dry powder and strategic buyers seeking to bolt on skilled workforces are likely to keep bid competition intense for quality construction targets throughout 2026. Acquirers who move early on targets with proven backlog visibility and data center exposure will face fewer competing bids than those who wait for macro clarity.

Indian Construction M&A Landscape (2026)

Construction and infrastructure M&A in India spans four sub-segments with distinct dynamics:

Cement and aggregates consolidation: driven by scale economics, logistics network, and clinker capacity access. Landmark Adani-Ambuja Cements and ACC acquisition from Holcim at approximately ₹80,000 crore combined (Indo-Swiss, 2022) was a defining moment. Domestic cement M&A active with UltraTech and Shree Cement acquiring smaller regional players. CCI review is intensive given post-deal market share concentration in cement sub-markets.

Real-estate developer M&A (post-RERA): consolidation across Indian residential and commercial real-estate developers post-2016 RERA implementation. Listed developer M&A (DLF, Godrej Properties, Oberoi Realty, Prestige Estates, Sobha, Brigade Enterprises) triggers SEBI SAST. Real-estate consolidation via schemes of arrangement under Companies Act Section 230 unlocks post-deal REIT-listing pathways.

EPC contractors and infrastructure PPPs: mid-market M&A across Indian EPC firms, roads and highways contractors, water infrastructure players, and specialized industrial construction firms. Larsen & Toubro (L&T) is the dominant Indian EPC player. Cross-border interest is strongest in Indo-Australian corridor (mining and industrial EPC), Indo-US corridor (specialty construction and pre-engineered buildings), and Indo-European corridor (green building materials and industrial construction).

Building materials adjacent M&A: ready-mix concrete, steel bars and structurals, tiles and sanitary-ware (Kajaria, Somany, Cera, Jaquar), paints (Asian Paints, Berger, Kansai Nerolac), and plywood and laminates (Century Ply, Greenlam). This sub-segment consolidates progressively driven by GST-enabled national distribution and organized retail growth.

Regulatory instruments applicable to Indian construction M&A: SEBI (SAST) Regulations 2011 for listed acquirers, Companies Act Sections 230 to 232 for schemes, IBC 2016 (relevant for stressed real-estate under 2018 IBC amendments for home-buyers), FEMA 100% automatic-route for construction and real-estate development (with lock-in requirements), CCI merger notification (concentrated in cement, tiles, and building materials sub-sectors), Section 47(vii) and Section 47(vic) tax-neutrality for share swaps and demergers, Section 50B slump sale, RERA compliance transfer with real-estate targets, Environmental Clearance under EIA Notification 2006, state-specific stamp duty on immovable-property transfers (Maharashtra, Karnataka, and Tamil Nadu have distinct rates that materially affect deal economics), and specific licenses for aggregate quarrying and river-sand extraction.

Focus sectors within Transjovan's coverage where construction M&A is most active include building materials (direct match), industrials (EPC and industrial construction), manufacturing (construction equipment and pre-engineered buildings), and energy transition (renewable IPPs and green infrastructure). Applicable corridors: Indo-Australian (mining and industrial construction EPC), Indo-US (specialty construction and REIT-linked), Indo-European (green building materials), and Indo-Japan (industrial construction and prefabricated modular).

Frequently Asked Questions

What does a buy-side advisor do in construction M&A?

A buy-side advisor helps the acquirer identify and screen targets, conduct sector-specific due diligence covering backlog quality, labor risk, project-level margins, and cash flow credibility, then negotiate deal structure and manage the transaction to close. In practice, the advisor functions as the acquirer's dedicated deal team throughout the process.

What is the success fee for buy-side M&A?

Buy-side success fees typically range from 1-3% of transaction value, often structured with a retainer plus success fee. Fees vary based on deal size, complexity, and scope of advisory services—and should be evaluated against the value of avoiding overpayment or structural errors.

Is M&A buy-side or sell-side?

M&A encompasses both buy-side (the acquirer pursuing a target) and sell-side (the company or owner seeking a buyer). Advisors typically specialize in one or the other, as the objectives, diligence focus, and negotiation dynamics differ significantly.

What is a buyout in construction?

A construction buyout is the acquisition of a contracting or subcontracting business by a PE firm or strategic acquirer. The buyer typically targets workforce capacity, specialized service capabilities, or access to high-demand end markets such as data centers and infrastructure.

Which construction sub-sectors are seeing the most M&A activity in 2026?

Data center and power infrastructure contractors, electrical and mechanical subcontractors, and residential services platforms are generating the highest buyer interest, driven by AI demand, energy transition investment, and persistent skilled labor shortages.

How do private equity buyers approach construction M&A differently from strategic acquirers?

PE buyers typically pay higher multiples, prioritize recurring service revenue and scalable workforce models, and structure deals with earn-outs and rollover equity. Strategic acquirers focus instead on synergy realization, capability adjacency, and geographic or customer base expansion.

Which Indian construction sub-sectors are seeing the most M&A activity in 2026?

The most active Indian construction M&A sub-sectors in 2026 span five clusters: (1) Cement and aggregates driven by scale economics and post-Adani-Ambuja consolidation momentum; UltraTech, Shree Cement, and other regional players actively acquiring smaller units. (2) Real-estate developer roll-ups post-RERA, with listed developers (DLF, Godrej Properties, Oberoi Realty, Prestige, Sobha, Brigade) driving mid-market consolidation and REIT-linked exits. (3) Building materials (tiles, sanitary-ware, paints, plywood, laminates) with GST-enabled national distribution driving consolidation. (4) EPC contractors and infrastructure PPPs benefiting from the National Infrastructure Pipeline (₹100 lakh crore investment target). (5) Green construction and sustainable building materials aligned to India's energy transition and Net Zero 2070 commitments. Focus sectors within Transjovan's coverage that match include building materials (direct), industrials, and energy transition (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials).

How does RERA compliance transfer in an Indian real-estate M&A transaction?

The Real Estate Regulatory Authority Act, 2016 (RERA) mandates registration of every real-estate project with the state RERA authority before marketing or booking. In an M&A transaction involving a real-estate developer, RERA compliance transfers with the target entity but requires careful DD: (1) confirm that all ongoing projects are RERA-registered with valid registration certificates; (2) verify project completion timelines against RERA commitments (delays trigger buyer refund rights and financial penalties); (3) audit escrow account balances (RERA requires 70% of buyer contributions to be maintained in project-specific escrow accounts, released against project milestones); (4) review buyer complaints and RERA disputes pending against the target; (5) validate registration of the acquiring entity as a promoter if control changes result in a change of promoter identity. Non-compliance carries penalty up to 10% of project cost. Change of promoter or transfer of majority rights typically requires two-thirds consent of the buyers of the project under Section 15 of RERA.

Which Indian M&A advisor is best for a construction and building materials mandate?

For Indian construction and building materials M&A, best-fit advisors span three categories. Large-cap listed construction and cement mandates: Kotak Mahindra Capital, ICICI Securities, Axis Capital, JM Financial anchor scaled execution with integrated ECM. Mid-market real-estate and building materials: sector-specialist advisors and PE-linked boutiques active in tiles, sanitary-ware, paints, and specialty construction. For Indo-X construction and building materials cross-border deals with CDaaS support, Transjovan Capital serves Indian construction and building materials promoters across Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridors (particularly Indo-Australian for mining EPC, Indo-US for specialty construction, Indo-European for green building materials) and 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials). Partner-led execution, sector track record in building materials, and regulatory fluency (RERA, EIA, state stamp duty, sector-specific licenses) matter more than league-table position at this deal type.