Introduction

In M&A, a strong valuation means little if the deal is structured poorly. Structure determines tax outcomes, risk exposure, liability transfer, and post-deal integration success. A misstep here doesn't just reduce deal value — it can trigger unexpected liabilities and quietly dismantle the synergies that justified the acquisition. Deal structure in Indian M&A carries unique tax, regulatory, and stamp duty consequences. A share purchase transfers ownership but not tax history. A slump sale under Section 50B transfers a business as a going concern with lump-sum consideration. A scheme of arrangement under Companies Act Section 230 requires NCLT approval but unlocks tax-neutrality under Section 47. Section 56(2)(x) creates deemed gift-tax exposure for below-FMV transfers. GST exempts business transfer as a going concern (BTA) but attracts 18% on partial asset deals. Every structural decision Indian acquirers make involves trade-offs across these five levers.

This guide is for CFOs, Corporate Development leads, and senior decision-makers at large enterprises and growth-stage companies evaluating acquisitions, mergers, or divestitures. If you're structuring a transaction — or building an acquisition program — the material below is directly relevant to the decisions you'll face.

We'll cover:

- What deal structure means and why it drives transaction outcomes

- The three core structural types (asset purchase, stock purchase, merger)

- How deal consideration is determined and structured

- The phases of structuring a transaction

- Where experienced teams consistently go wrong

Key Takeaways

- M&A deal structure defines the legal form (asset, stock, or merger), payment method, and risk allocation between buyer and seller

- Each of the three primary structures carries distinct tax, liability, and operational consequences—the right choice depends on both parties' objectives

- Consideration can be cash, equity, earnouts, seller financing, or hybrid, each with different risk/reward tradeoffs

- Deal structuring evolves through three phases: negotiation and LOI, due diligence, and the definitive agreement

- Misunderstanding or rushing structure is one of the most common causes of destroyed deal value

What Is an M&A Deal Structure?

An M&A deal structure is the binding framework that governs how a transaction is executed. It covers three core elements:

- What is being acquired — assets, equity, or the entire entity

- How consideration is paid — cash, stock, earnouts, or a combination

- How rights, obligations, and risks are allocated between buyer and seller

The structure is designed to align the commercial, legal, and tax interests of both parties while creating a workable path to closing.

The LOI (Letter of Intent) and Term Sheet formalize these terms before the definitive agreement is executed. While most LOI provisions are non-binding, hybrid LOIs routinely include legally binding clauses for exclusivity and confidentiality to protect the buyer's investment during diligence.

One distinction worth keeping clear: structure refers to the legal mechanism (asset purchase vs. stock purchase), while terms refer to the specific financial conditions — price, earnouts, indemnities. The two must be optimized together, because changing the structure changes the effective price.

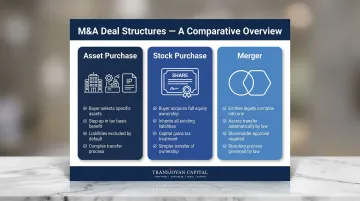

The Three Core M&A Deal Structures

The three legal structures are asset purchase, stock purchase, and merger. In practice, these can be used in combination. The choice directly influences the level of due diligence required, the type of consents needed, and the complexity of closing.

Asset Purchase

In an asset purchase, the buyer selects and acquires specific assets (and, optionally, liabilities) of the target—not the legal entity itself. The seller retains the corporate shell and any excluded assets or liabilities.

Buyer advantages:

- Clean acquisition without inheriting unknown liabilities

- Basis step-up for tax purposes, allowing for accelerated depreciation

- Selective asset picking

Seller disadvantages:

- Potential double taxation on depreciable assets (especially for C-corporations)

- Complex asset-by-asset transfer process

- Need for third-party consents on contracts and licenses

Stock Purchase

In a stock purchase, the buyer acquires the target company's equity directly from its shareholders, stepping into the seller's position. The buyer inherits all assets, liabilities, contracts, and obligations — no separate transfer of individual assets required.

Buyer and seller considerations:

- Sellers generally prefer stock sales for cleaner tax treatment (capital gains vs. ordinary income) and a full exit

- Buyers assume more risk but benefit from continuity of contracts, permits, and customer relationships

- Change-of-control clauses in contracts can still be triggered despite the legal continuity

To bridge the tax gap, parties can use an IRC Section 338(h)(10) election during a stock purchase. This allows the stock sale to be treated as a hypothetical asset deal for tax purposes, granting the buyer the stepped-up basis while maintaining the legal simplicity of a stock transfer.

Merger

In a statutory merger, two entities legally combine into one surviving entity by operation of law. Assets and liabilities transfer automatically without individual conveyance documents.

Key sub-types:

- Forward merger

- Reverse merger

- Reverse triangular merger (the most common structure in corporate acquisitions)

Mergers typically require shareholder consent (often a majority) and may trigger regulatory review depending on deal size and sector. Acquirers prefer mergers when deep integration and operational consolidation are the strategic goal.

In PE-backed mergers, rollover equity is a common companion mechanism. Sellers retain a minority stake post-close — typically between 5% and 20% — preserving upside exposure while giving the buyer operational control.

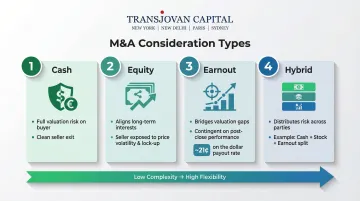

Payment Methods and Consideration in M&A Transactions

"Consideration" refers to what the buyer pays and can take multiple forms: cash, buyer equity (stock), earnouts, or a combination. Choosing the right form shapes valuation risk, tax exposure, and seller incentives as much as the deal structure itself.

Each type carries distinct trade-offs. Here is how they compare in practice.

Cash Consideration

- Simplest form; provides the seller a certain, clean exit

- Places full valuation risk on the buyer

- May require significant debt or equity financing at close

- In cross-border transactions (for example, India-to-US), currency exposure and regulatory approval for remittance add complexity

Equity Consideration

- Buyer pays with its own shares rather than cash

- Aligns long-term interests but exposes the seller to share price volatility, lock-up periods, and illiquidity

- Lockup agreements signal strong fundamentals and are associated with higher deal completion rates

- Typical in mergers or when the buyer's stock trades at a premium

Earnouts

- A portion of the purchase price is contingent on post-close performance milestones — revenue, EBITDA, or customer retention

- Used to bridge valuation gaps when buyer and seller disagree on future performance

- Earnout usage dropped from 26% in 2023 to 18% in 2024/2025, reflecting tighter deal terms

- Watch the payout reality: Earnouts pay out approximately 21 cents on the dollar outside life sciences

- Poorly defined metrics create post-deal disputes — 35% of M&A disputes cite earnouts as a contributing factor

Hybrid Structures

Most mid-to-large transactions combine consideration types to distribute risk between buyer and seller. A $50 million acquisition, for instance, might be structured as $35 million cash at close, $10 million in buyer stock subject to a 12-month lockup, and $5 million earnout tied to 12-month revenue targets exceeding $20 million.

This layered approach lets buyers preserve liquidity while giving sellers upside participation — and gives both parties a shared stake in post-close performance.

The Three Phases of M&A Deal Structuring

Phase 1 — Negotiation and Term Sheet/LOI

Both parties articulate their core objectives, risk tolerances, and preliminary deal parameters. The LOI or term sheet captures the proposed structure, price range, exclusivity period, and key conditions. Most terms are non-binding at this stage but set the commercial tone for everything that follows.

Phase 2 — Due Diligence

The buyer conducts comprehensive financial, legal, tax, and operational review to verify the target's representations and identify risks. In 85% of deals, Quality of Earnings and due diligence findings result in purchase price reductions.

Those findings do more than adjust price — they often reshape the deal structure itself. Uncovered liabilities may shift preference from a stock deal to an asset deal, and the full scope of findings determines the scope of reps, warranties, and indemnities in the final agreement.

Diligence timelines vary by deal size:

- Small transactions (under $50 million): 30-45 days

- Mid-market ($50-500 million): 45-90 days

- Large/cross-border (over $500 million): 90-180 days or longer

Phase 3 — Definitive Agreement and Closing

The final purchase agreement (SPA or APA) is executed, incorporating all negotiated terms, representations and warranties, closing conditions, and post-close obligations. Deal structure decisions made early cascade through all closing mechanics—including escrow arrangements, regulatory filings, and employee transition plans.

Risk allocation at closing has also evolved: 63% of recent private deals now use Representations and Warranties Insurance (RWI) to shift indemnification exposure to third-party insurers.

Key Factors and Common Pitfalls in Deal Structuring

Key Factors That Determine Structure Choice

- Nature of the target entity (corporation, LLC, partnership)

- Tax position of both parties

- Presence of legacy liabilities or contingent claims

- Transferability of key contracts and licenses

- Regulatory requirements in the relevant jurisdictions

- Seller's post-deal involvement preference (full exit vs. continued stake)

In cross-border transactions spanning multiple jurisdictions—such as those Transjovan Capital regularly advises on across the US, Europe, India, and APAC—local tax law, foreign investment approvals, and regulatory compliance add substantial layers to structuring complexity. That complexity is also where the most costly structuring errors tend to occur.

Most Common Deal Structuring Mistakes

Three patterns appear repeatedly in failed or underperforming transactions:

- Choosing structure by familiarity — defaulting to stock or asset deals based on what the team knows, rather than transaction-specific fit

- Treating structure and valuation as separate conversations — they are interdependent; an asset deal with a basis step-up may justify a higher purchase price than a stock deal where the buyer absorbs unknown liabilities

- Delaying integration planning — between 70% and 90% of M&A transactions fail or underperform, and top acquirers begin integration planning during due diligence, not after signing; the structure itself can create operational barriers if integration isn't considered upfront

The Misconception About Deal Structure

Deal structure is not purely a legal or tax decision. It signals intent: how each party values the business, how much risk each is willing to absorb, and what the post-close relationship will look like.

This is why structure choices made early in a transaction carry consequences well beyond the closing table. The wrong structure can undermine workforce retention, delay synergy capture, and erode the long-term value the deal was meant to create.

Conclusion

M&A deal structure is the foundational decision-making layer of any transaction. It shapes tax outcomes, liability allocation, integration complexity, and whether the intended value of the deal is realized or eroded. No single structure fits every deal — the optimal choice depends on each party's objectives, the target's risk profile, and the transaction's strategic rationale.

Getting structure right requires coordinated legal, financial, tax, and strategic input — from the earliest conversations, not as an afterthought. The key dimensions that determine that outcome:

- Transaction type: Asset vs. stock vs. merger, each carrying distinct liability and tax consequences

- Consideration mix: Cash, equity, earnouts, and seller notes affect risk allocation and post-close alignment

- Regulatory and tax positioning: Jurisdictional nuances can materially shift net deal economics

- Integration readiness: Structure should reflect how — and how quickly — the acquirer intends to operate the target

For enterprises managing multiple acquisitions or building a consistent inorganic growth strategy, Transjovan Capital's Corporate Development as a Service (CDaaS) model embeds this structuring discipline across every deal — ensuring it is applied systematically, not improvised transaction by transaction.

Indian M&A Deal Structure Landscape (2026)

Indian M&A structures span statutory mergers, private acquisitions, and specialized frameworks for stressed and cross-border deals:

- Share Purchase Agreement (SPA) — the target company continues to exist, shares change hands. Simple to execute but the buyer inherits all liabilities (tax, litigation, contingent). Long-term capital gains are taxed at 20% with indexation (or 10% without, for listed shares held >12 months); short-term at 15% (listed) or slab rates.

- Slump Sale under Section 50B — transfers an "undertaking" (business as a going concern) for a lump-sum consideration. Buyer receives specific assets + liabilities of that undertaking; seller entity continues to exist. Capital gains taxed under Section 50B based on net worth methodology.

- Asset Purchase Agreement (APA) — cherry-picks specific assets. Attracts 18% GST unless structured as BTA (business transfer agreement) as a going concern. Stamp duty applies per state — Maharashtra, Karnataka, and Tamil Nadu have distinct rates that materially affect deal economics.

- Scheme of Arrangement — Companies Act Sections 230–232 — statutory merger, demerger, or restructuring requiring NCLT approval, creditor consent, and shareholder resolution. Enables tax-neutral structuring under Section 47(vi)-(vii). The HDFC Ltd → HDFC Bank merger used a scheme under Section 230.

- IBC Resolution Plan — for stressed-asset acquisitions under the Insolvency Code, deal structure is defined by the resolution plan approved by 66%+ of the Committee of Creditors and sanctioned by NCLT. The ArcelorMittal-Nippon acquisition of Essar Steel at ₹42,000 crore was executed under this framework.

- Cross-Border Structures for Indo-US Corridors — foreign strategics acquiring Indian targets navigate FEMA reporting (Form FC-GPR for inbound investment), FDI approval-route or automatic-route depending on sector, and DTAA benefits (India-US, India-Netherlands, India-Mauritius routes materially affect withholding tax). Outbound Indian acquisitions in Indo-US or Indo-European targets face CFIUS (US) or EU merger control alongside RBI ODI reporting.

- Section 47 Tax-Neutrality — qualifying share swaps and mergers under Sections 47(vi), 47(vii), and 47(vic) are tax-exempt for the transferor when consideration is in equity. Critical for structuring high-value transactions to defer tax at the deal level.

- GAAR (Chapter X-A) — General Anti-Avoidance Rules empower tax authorities to disregard structures whose primary purpose is tax avoidance. Aggressive structures need to survive commercial-substance and business-purpose tests.

Frequently Asked Questions

What is the deal structure in M&A?

An M&A deal structure defines the legal and financial terms under which a transaction is executed—including what is being acquired, how consideration is paid, and how risks and obligations are allocated between buyer and seller.

What are the common deal structures?

The three primary structures are asset purchase, stock purchase, and merger. Combinations are frequently used in practice depending on the tax, legal, and operational priorities of both parties.

What are the three main phases of deal structuring?

The three phases are: (1) negotiation and LOI/term sheet, (2) due diligence, and (3) definitive agreement and closing. Each phase can reshape structural decisions as findings emerge.

What is the M&A deal flow?

M&A deal flow refers to the pipeline of potential transactions a buyer or advisor identifies, evaluates, and pursues. It spans initial target identification and outreach through LOI, due diligence, and final close.

What is M&A in negotiation?

M&A negotiation encompasses the process of reaching agreement on deal structure, valuation, consideration type, representations and warranties, and closing conditions. Both parties balance commercial priorities, legal exposure, and risk allocation throughout.

What is the difference between share purchase and slump sale in Indian M&A?

A share purchase transfers ownership of the target company by acquiring its shares — all liabilities (including tax, litigation, and contingent obligations) transfer with the shares, but the target's PAN and existing contracts continue. Capital gains tax applies to the seller: long-term (20% with indexation or 10% without for listed) vs. short-term (15% for listed / slab for unlisted). A slump sale under Section 50B transfers a business undertaking as a going concern for a lump-sum consideration — the buyer receives only the specified undertaking (assets + liabilities of that business), and the seller entity continues to exist. Slump sale gains are taxed as capital gains under Section 50B based on net worth methodology. Structure choice materially changes stamp duty exposure, GST treatment, and post-deal complexity — advisors typically model both against Section 47 tax-neutrality options before finalizing.

How does Section 47 tax-neutrality work in Indian mergers?

Section 47 of the Income Tax Act 1961 exempts certain qualifying transfers from capital gains tax when the transaction is structured as a share swap or statutory merger, deferring tax liability at the deal level. Key sub-sections: Section 47(vi) exempts transfers in a scheme of amalgamation where the amalgamated company is an Indian company; Section 47(vii) exempts allotment of shares to shareholders of the amalgamating company in consideration of the merger; Section 47(vic) covers demergers. These provisions enable tax-neutral structuring of mergers, demergers, and share-swap M&A — critical for large-value deals like the HDFC-HDFC Bank merger. However, GAAR (General Anti-Avoidance Rules) can reclassify aggressively structured transactions if they lack commercial substance.

How does GST apply to Indian M&A deal structures?

GST treatment varies materially by deal structure. Business Transfer as a Going Concern (BTA) — transferring an entire business as a going concern is exempt from GST under Notification No. 12/2017 (Entry 2). This makes BTA the preferred structure for full-business acquisitions. Partial asset sales or piecemeal transfers of specific assets attract 18% GST (higher for certain categories). Share purchase attracts no GST as transfer of securities is outside GST scope. Slump sale — treated as supply of business if structured as going-concern transfer, thus exempt; otherwise attracts GST on individual asset components. Cross-border transactions have additional GST complexity around place of supply rules. Advisors typically confirm BTA-eligibility upfront to avoid 18% GST erosion on transaction value.