Introduction

Divestitures are no longer defensive moves. For well-performing enterprises, they are deliberate instruments for sharpening focus, unlocking capital, and creating shareholder value. Indian M&A reached roughly ₹5 lakh crore (USD 60.2 billion) across 963 deals in 2025, up 36% in value year-over-year, with divestitures driven by portfolio rationalization and capital reallocation rather than distress. For Indian divestitures, structure choice materially changes tax exposure, stamp duty, GST treatment, and closing timeline. A slump sale under Section 50B transfers a business as a going concern with lump-sum consideration. A demerger under Section 47(vic) provides tax-neutrality when the resulting company issues shares to shareholders of the demerging company in proportion. A share sale is simplest but preserves target-entity liabilities. An asset sale cherry-picks but attracts 18% GST unless structured as BTA. Every Indian divestiture navigates these four structural levers.

The data bears out this shift: companies engaging in focused divestment outperform inactive peers by 15% in total shareholder return over a decade, and nearly 40% when combined with a repeatable M&A model. Separately, 37% of executives report that activist investor activity prompted a review of strategic alternatives, underscoring the external pressure on conglomerates to rethink portfolio composition.

This guide gives corporate leaders a practical framework for the full divestiture process: from defining the strategic rationale and selecting the right structure, through execution and transition.

TL;DR:

- A divestiture is the strategic disposal of a business unit or asset to achieve defined portfolio objectives

- Four primary types: sell-off, spin-off, carve-out, and split-up

- Planning begins with portfolio review, valuation, and de-integration roadmaps

- Execution spans buyer engagement, due diligence, and transition service agreements

What Is a Divestiture Strategy?

A divestiture strategy is the deliberate decision by a company to dispose of a business unit, subsidiary, asset, or division—either partially or entirely—to pursue a defined strategic or financial objective. What distinguishes a divestiture from an ad hoc asset sale is intentionality: it is goal-driven, planned, and aligned with broader corporate strategy.

Divestitures fall into two broad categories. Voluntary divestitures are company-initiated for strategic reasons, such as shedding non-core units to refocus on high-margin segments. IBM's 2021 spin-off of its managed infrastructure services business into Kyndryl is a clear example — a deliberate move to sharpen focus on hybrid cloud and AI.

Involuntary divestitures, by contrast, are mandated by regulators or courts, typically to remedy antitrust concerns. The European Commission's 2024 order requiring Illumina to divest GRAIL to restore competitive conditions illustrates how external pressure — not internal strategy — can force a company's hand.

Why Do Companies Choose to Divest?

Strategic Realignment

Companies divest when a unit no longer fits their core business direction, when conglomerate structures dilute focus, or when activist investors push for separation to unlock value. Portfolio rationalization is a core driver for large enterprises.

Yet 78% of executives admit they hold onto assets too long — waiting until performance deteriorates rather than acting on a clear strategic signal.

Financial Motivations

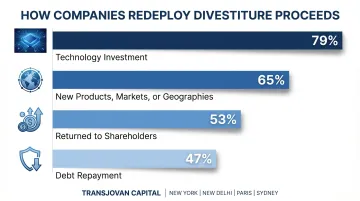

Divestitures generate liquidity that can be redeployed toward higher-return opportunities. According to EY's Corporate Divestment Study, sellers reinvest proceeds as follows:

- 79% in technology

- 65% in new products, markets, or geographies

- 53% returned to shareholders

- 47% used to pay down debt

Selling a non-core unit often yields more than retaining it inside a larger portfolio. Freed from a parent's cost structure and capital allocation constraints, standalone entities typically attract higher multiples from acquirers who value focus.

Operational and Regulatory Drivers

Internally, units that drag on margins or consume disproportionate management bandwidth become prime divestiture candidates. Externally, regulators can compel divestitures as a condition of merger approval. High-profile antitrust-mandated examples include:

- T-Mobile/Sprint (2019): The US DOJ required divestiture of Sprint's prepaid business and spectrum assets to Dish Network to enable a viable competitor.

- 7-Eleven/Speedway (2021): The FTC mandated divestiture of retail fuel assets in 293 local markets across 20 states.

The 4 Main Types of Divestiture Strategies

Most divestitures fall into four main categories: sell-off, spin-off, carve-out, and split-up. Each carries distinct structural mechanics, tax implications, and strategic use cases. Liquidation is sometimes listed separately as an extreme form, reserved for distressed or bankruptcy situations.

Sell-Off (Trade Sale)

A sell-off is the outright sale of a business unit, subsidiary, or asset to a third-party buyer—strategic acquirer or financial sponsor—in exchange for cash or other consideration. The parent company retains its existence post-sale.

A sell-off suits situations where:

- The unit has clear standalone value and can attract competitive bids

- The seller needs immediate liquidity from the transaction

- A strategic buyer can justify a premium through synergies

This is the most common divestiture method across deal sizes and industries.

Spin-Off

A spin-off is the separation of a business unit into an independent, publicly traded company, with shares distributed to the parent company's existing shareholders on a pro-rata basis. No cash changes hands; shareholders gain direct ownership in both entities.

A spin-off is appropriate when:

- The unit has sufficient scale to operate and raise capital independently

- The market is undervaluing it within the conglomerate structure

- Separate capital allocation would unlock a higher equity multiple

eBay's 2015 spin-off of PayPal illustrates the value unlocked: PayPal's debut market cap of $46.6 billion topped eBay's $34 billion, validating the separation thesis.

Carve-Out

A carve-out (equity carve-out) is the partial IPO of a subsidiary, where a minority stake is sold to public market investors while the parent retains a controlling interest. This creates a separately traded entity without full separation.

A carve-out works well when:

- The parent wants to monetize a portion of a high-value unit without full exit

- Establishing a public market valuation for the subsidiary is strategically useful

- Retaining operational control remains a priority while accessing public capital

Carve-outs frequently serve as a precursor to a full spin-off once the market valuation is established.

Split-Up

A split-up is the dissolution of the parent company into two or more independent successor entities, with the original parent ceasing to exist. Shareholders receive proportional stakes in the new companies.

A split-up is suited for scenarios where:

- Separate entities trade at a higher combined valuation than the consolidated whole

- Divergent business cycles or investor bases make a unified structure counterproductive

- Activist pressure or strategic review has concluded that breakup maximises shareholder value

General Electric's three-way breakup — announced in 2021 and completed in 2024 — created three independent companies focused on aviation, healthcare, and energy, and stands as the most prominent recent example of this structure in practice.

Divestiture Planning: Key Steps Before Going to Market

Step 1 — Portfolio Review and Strategic Rationale

Divestiture planning begins with a structured portfolio review to identify non-core, underperforming, or strategically misaligned assets. Decision-makers should assess each unit against criteria including market performance, growth trajectory, operational synergies, and alignment with the company's long-term vision.

Companies that identify misaligned businesses earlier have been shown to increase the chances of delivering a positive return by two times — and five times for public companies.

Yet review frequency remains inconsistent. Nearly two-thirds of respondents evaluated divestiture candidates more than twice per year in 2024, though that cadence fell to fewer than half by the end of 2025.

Step 2 — Business Valuation and Financial Preparation

Before approaching buyers, the selling company must develop a credible valuation of the divestiture candidate. This involves:

- Financial modeling

- EBITDA normalization to adjust for non-recurring items

- Comparables analysis to benchmark against similar transactions

- Identifying value drivers that a buyer would recognize

Poorly prepared financials are one of the leading causes of deal delays and price discounts. Preparation quality continues to be the largest driver of value, influencing proceeds, time to close, buyer engagement, and cost-to-achieve.

Step 3 — De-Integration Planning

De-integration is the process of operationally and legally separating the divested unit from the parent: disentangling shared functions and infrastructure so the business can stand on its own. Ideally, this work begins before a buyer is identified.

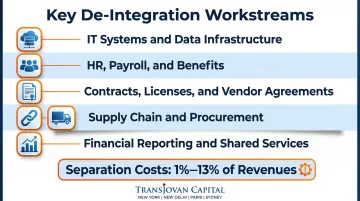

Key separation workstreams typically include:

- IT systems and data infrastructure

- HR functions, payroll, and benefits

- Contracts, licenses, and vendor agreements

- Supply chain and procurement relationships

- Financial reporting and shared services

Separation costs typically range from 1% to 5% of the divested business's revenues, but can reach up to 13% in highly entangled carve-outs. Recovery from stranded costs can take up to three years for the parent company to recover from stranded costs, leaving it with substantially lower profit margins during this period.

Step 4 — Transition Service Agreements (TSAs)

A TSA is a formal agreement where the seller continues to provide specified services — IT, HR, finance, logistics — to the divested unit for a defined post-close period, allowing the buyer time to establish independent operations.

While overall TSAs typically run 6 to 24 months, IT-specific TSAs frequently last 8 to 12 months or longer depending on system complexity. TSAs should have clearly defined scope, pricing, duration, and exit milestones to prevent prolonged dependency.

The Role of an Experienced Corporate Development Partner

Companies without a dedicated internal M&A function often benefit from embedding an external corporate development team to manage the full divestiture planning lifecycle without burdening CXO bandwidth. Transjovan Capital's Corporate Development as a Service (CDaaS) model is built for exactly this — providing embedded, partner-led support across each planning step, from portfolio review through TSA design, without the overhead of building an internal function.

Executing a Divestiture: From Buyer Engagement to Close

Buyer Identification and Outreach

Building a targeted buyer list requires distinguishing between strategic buyers—who may pay a premium for synergies—and financial sponsors/PE firms, who evaluate standalone cash flow potential. The process centers on three workstreams:

- Preparing a Confidential Information Memorandum (CIM) that frames the asset's value story

- Running a controlled, competitive process to surface the best-fit buyers

- Sequencing outreach to maintain leverage without leaking sensitive information

Due Diligence Management

Sellers must prepare a virtual data room (VDR), coordinate responses across multiple bidders, and ensure disclosures are complete and well-organized. Proactive sell-side diligence surfaces issues before buyers do—giving sellers the opportunity to address them directly or build a negotiation position around them.

A tightly managed diligence process typically delivers better pricing and fewer post-close disputes.

Negotiation, Deal Structuring, and Legal Close

Key deal structuring considerations include:

- Asset sale vs. share sale

- Representations and warranties

- Indemnification provisions

- Earnout clauses

- Regulatory approvals

In multi-jurisdiction deals, regulatory timelines can add 12–18 months to the sign-to-close period. For example, EU Phase II investigations run 90 working days, extendable to 105 if remedies are offered. Overall, sign-to-close timelines have lengthened by roughly 6% since 2020, with median closes taking about three months, though complex deals can extend to 10 months or more.

Post-Close Review and Value Capture

A rigorous post-close review—comparing actual outcomes against the original strategic and financial objectives—reveals where outcomes diverged from plan and validates whether the divestiture achieved its intended purpose. The most useful reviews go beyond financial metrics: they examine execution gaps, buyer selection rationale, and how proceeds are being deployed—informing how the next transaction is structured from the outset.

Common Divestiture Pitfalls and How to Avoid Them

Reactive Rather Than Proactive Divestiture Decisions

Many companies wait too long to divest—only acting when a unit is deeply underperforming or when a crisis forces their hand. Proactive portfolio reviews and pre-divestiture preparation (carve-out readiness, financial clean-up) consistently yield better buyer interest and higher valuations. Separations completed within 12 months of their announcement delivered higher excess total returns to shareholders than those that took longer.

Underestimating Separation Complexity

Companies frequently underestimate the time and cost involved in de-integration—particularly for units with deeply entangled IT systems, shared supply chains, or joint customer contracts. TSAs often run well beyond their intended duration, creating ongoing costs and management distraction.

To contain this risk, sellers should plan for operational independence from day one:

- Build detailed de-integration roadmaps with tracked milestones

- Identify shared IT systems and customer contracts early

- Set clear TSA exit timelines and enforce them contractually

Talent and Employee Uncertainty

Key employees in the divested unit often leave during the uncertainty of a sale process, which directly erodes the asset's value at the point of sale. A retention strategy and clear communication plan for the divestiture unit's workforce should be in place well before the sale process goes live. Incentives such as retention bonuses also help keep employees engaged through TSA delivery.

This people risk extends beyond the divested unit. 63% of companies acknowledge not placing enough emphasis on RemainCo during their last carve-out or spin-off—amplifying both talent loss and operational disruption on the parent side.

Indian Divestiture Landscape (2026)

Indian divestitures span five distinct structural paths:

- Slump sale under Section 50B: transfers a business undertaking as a going concern for lump-sum consideration. Taxed as capital gains under Section 50B using net worth methodology. BTA-eligible for GST exemption.

- Demerger under Section 47(vic) and Companies Act Sections 230 to 232: statutory demerger requiring NCLT approval, allotment of shares of the resulting company to shareholders of the demerging company in proportion (subject to 3-year holding), and 75% shareholder value threshold. Provides tax neutrality for both entities and shareholders.

- Sale of entire subsidiary via share sale: cleanest exit for a discrete legal entity, taxed as capital gains. Simple SPA structure but liabilities transfer with shares.

- Asset sale: cherry-picks specific assets. Attracts 18% GST unless structured as BTA (business transfer agreement) as a going concern. Stamp duty applies per state.

- Reverse merger or listing via SPAC: less common in India post-SEBI 2021 framework; still relevant for cross-border Indo-US divestitures of Indian subsidiaries.

Landmark 2022 to 2025 Indian divestitures include the Holcim exit from Ambuja Cements and ACC via sale to Adani Group at approximately ₹80,000 crore combined, which triggered SEBI SAST open offer economics; and various Reliance, Tata, and L&T demergers structured under Companies Act Section 230 to unlock focused-play valuations.

Regulatory pathway involves SEBI (SAST) for listed sellers, Companies Act Sections 230 to 232 for schemes of arrangement, IBC for stressed carve-outs, FEMA for cross-border share transfers, CCI merger notification when applicable, Section 47(vic) tax neutrality for qualifying demergers, Section 50B for slump sale accounting, and state-specific stamp duty. Rule 11UA valuation applies for related-party divestitures.

Frequently Asked Questions

What is a divestiture strategy?

A divestiture strategy is a company's deliberate plan to sell, spin off, or otherwise dispose of a business unit or asset to meet specific strategic or financial goals—such as refocusing on core operations, raising capital, or improving shareholder returns.

What are the 4 types of divestitures?

The four primary types are sell-off (outright sale to a buyer), spin-off (pro-rata distribution to shareholders), carve-out (partial IPO with parent retaining control), and split-up (dissolution of the parent into separate entities). Liquidation is sometimes added as a fifth, applied in distressed or bankruptcy scenarios where no buyer exists for the business as a whole.

What are the steps in a divestiture process?

The key stages are: portfolio review and strategic rationale → business valuation → de-integration planning → buyer engagement → due diligence → negotiation and close → post-close review.

What happens to employees in a divestiture?

Employees in the divested unit typically transfer to the new owner as part of the transaction, though terms depend on deal structure. Uncertainty during the process can lead to attrition, making early, transparent communication and retention plans essential.

What is the difference between liquidation and divestiture?

Divestiture transfers a business unit or asset to another party as a going concern. Liquidation winds down operations and sells off individual assets to pay creditors, typically when a company is insolvent and no viable buyer exists for the whole.

What is an example of a divestiture strategy?

eBay's 2015 spin-off of PayPal is a classic example, separating the two businesses to let each pursue independent shareholder value. GE's three-way breakup into aviation, healthcare, and energy entities (completed 2023–2024) illustrates a split-up driven by conglomerate restructuring.

What is a demerger under Section 47(vic) and how does it provide tax neutrality?

A demerger is a scheme of arrangement under Companies Act Sections 230 to 232 that splits a company (demerging company) into two entities. The resulting company issues its shares to shareholders of the demerging company in proportion, splitting an integrated business into focused entities. Section 47(vic) provides tax neutrality when the demerger meets specific conditions: (1) transfer of all liabilities and assets of the undertaking, (2) shares of the resulting company are issued to shareholders of the demerging company on a proportionate basis, (3) the shareholders holding at least 75% (in value) of the demerging company become shareholders of the resulting company, (4) transfer is not a mere change of legal form, and (5) resulting company is an Indian company. When these conditions are met, no capital gains tax arises for either entity or shareholders. Indian conglomerates including Reliance, Tata, and L&T have used this to unlock focused-play valuations for their business units.

How does a slump sale under Section 50B differ from an asset sale?

Both structures transfer business or assets, but with material tax, GST, and legal differences. Slump sale under Section 50B: transfers an "undertaking" (defined as an unit or division carrying on business activities) as a going concern for lump-sum consideration without assigning individual asset values. Taxed under Section 50B as capital gains, computed as consideration minus net worth of the undertaking (net worth being the aggregate of book values of assets minus liabilities). GST exempt when qualifying as BTA (business transfer as a going concern) under Notification 12/2017 Entry 2. Stamp duty applies per state to the composite transfer. Asset sale: cherry-picks specific assets, with individual asset values assigned. Attracts 18% GST on individual assets (higher for some categories) unless the transfer qualifies as a going concern. Depreciation recapture applies to fixed assets. More complex closing due to individual asset transfers. Structure choice materially changes tax outcome, stamp duty exposure, and buyer indemnity preferences.

Which Indian M&A advisor is best for a corporate divestiture or carve-out?

For Indian corporate divestitures and carve-outs, best-fit advisors span three categories. Domestic full-service banks (Kotak Mahindra Capital, ICICI Securities, Axis Capital, JM Financial) anchor sell-side execution for large-cap listed divesting entities, with integrated ECM and structuring support. Sector-focused boutiques like Avendus Capital lead consumer, tech, and healthcare divestitures. For Indo-X cross-border carve-out and divestiture mandates with embedded CDaaS support, Transjovan Capital serves Indian conglomerates and PE-backed businesses across 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials) and 7 corridors (Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European). Partner-led execution, sector track record, and structuring depth (Section 47(vic), Section 50B, Section 230 to 232, SEBI SAST, GST BTA) matter more than league-table position at this deal type.