Introduction

India's M&A activity crossed ~₹5 lakh crore (USD 60.2 billion) across 963 transactions in 2025 per the Grant Thornton Annual Dealtracker 2026 — up 36% by value and 41% by volume year-over-year — with 14 billion-dollar mega-deals contributing USD 34.3 billion (over 50% of total value). Cross-border flow strengthened into semiconductors, industrials, EVs, and AI infrastructure. Landmark 2024–25 deals like the Reliance–Disney India JV, the HDFC–HDFC Bank merger and the Adani–Ambuja/ACC acquisition have reset market expectations for scale, valuation, and regulatory sophistication.

Choosing the right M&A advisor has never carried higher stakes for Indian promoters. The right firm navigates SEBI (SAST) takeover regulations, structures deals under Companies Act 2013 Section 230, manages IBC-driven acquisition opportunities, works within FEMA constraints for foreign buyers, secures CCI clearance where applicable, and structures for tax-neutral outcomes under Section 47 of the Income Tax Act — while the wrong one costs time, capital, and deal momentum.

This guide covers the top M&A advisory firms serving Indian mandates in 2026 across the Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridors — what sets each apart and how to match the right firm to your specific mandate, whether you are raising growth capital, executing an M&A, devising corporate strategy, maximising sales, or expanding cross-border.

Key Takeaways

- Indian M&A advisory spans domestic full-service investment banks, sector-focused boutiques, and global bulge-brackets partnering on cross-border mandates

- Firm selection hinges on deal size (₹100 crore mid-market vs. ₹8,000 crore+ large-cap), sector expertise across India's focus sectors, corridor experience, and whether you need transactional support or an embedded corporate development model

- Domestic leaders Kotak Mahindra Capital and ICICI Securities dominate by deal count in India, while Axis Capital, Avendus Capital, and JM Financial anchor mid-market and sector-boutique execution

- Cross-border specialists like Transjovan Capital offer Indo-X corridor depth (Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, Indo-European) that generalist domestic banks rarely match

- Prioritize partner-led execution, sector track record in your industry, regulatory fluency (SEBI/CCI/FEMA), and post-deal integration capability

What Do M&A Advisory Firms Do?

M&A advisory firms act as strategic and financial intermediaries guiding companies through acquisitions, divestitures, and partnerships from first contact to closing. Their role extends well beyond matchmaking:

- Assess strategic fit between potential acquirers and targets

- Quantify synergies and build valuation models

- Manage confidentiality and data room processes

- Create competitive tension among bidders to maximize value

- Coordinate legal, financial, and operational workstreams through signing and close

The two primary advisory roles are buy-side (advising the acquirer) and sell-side (advising the seller):

- Buy-side advisors manage target screening, valuation modeling, due diligence coordination, and synergy evaluation

- Sell-side advisors prepare marketing materials, manage data rooms, contact prospective buyers, and run auction processes

Corporate Development as a Service (CDaaS) is a newer model where advisors act as a continuous, embedded extension of a company's corporate development team rather than stepping in for individual transactions. It covers the full deal lifecycle — from strategy and target identification through execution and post-merger integration — without the cost of building an in-house team.

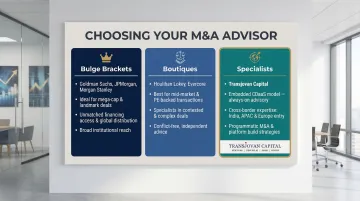

The M&A advisory landscape spans domestic full-service investment banks (Kotak, ICICI Securities, Axis Capital, JM Financial), sector-focused boutiques (Avendus, Ambit), and global bulge-brackets partnering on Indo-X cross-border mandates. Choosing the right category — and the right firm within it — depends on deal size, corridor, sector, and how much ongoing M&A capability your organization needs.

Indian M&A Advisory Landscape (2026)

Any M&A transaction involving an Indian buyer or seller sits inside a specific regulatory and structural framework that shapes deal timing, cost, and structure. Advisors serving Indian mandates need fluency across:

- SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 — the "SAST" trigger threshold of 25% of voting rights obligates the acquirer to make an open offer for an additional 26%, materially changing the economics of listed-company acquisitions. Recent applications include the Adani group's takeover of Ambuja Cements via a mandatory open offer following the Holcim exit.

- Companies Act, 2013 — Section 230 to 232 — the mechanism for schemes of arrangement (mergers, demergers, restructurings) requires NCLT approval and creditor consent. The HDFC Ltd → HDFC Bank merger — India's largest ever at ₹40 lakh crore combined balance sheet — was structured under Section 230.

- Insolvency and Bankruptcy Code (IBC), 2016 — a driver of India's stressed-asset M&A. The ArcelorMittal–Nippon Steel acquisition of Essar Steel for ₹42,000 crore (Indo-Japan Indo-European trilateral) was closed via the IBC resolution process and set precedent for foreign-consortium bids on Indian distressed assets.

- FEMA and FDI Regime — foreign buyers face either automatic-route or approval-route FDI depending on sector and stake. Sensitive sectors (defence, telecom, print media, some financial services) require government approval; construction, manufacturing, and most services are under automatic route.

- Competition Commission of India (CCI) — merger notification thresholds (asset/turnover-based, currently ₹1,000 crore of assets in India or ₹3,000 crore of turnover in India, among others) require pre-transaction clearance. Timelines add 30–120 days depending on Phase I/II review.

- Income Tax Act — Section 47 — provides tax-neutral treatment for qualifying mergers, demergers, and slump sales, but structural choices (share purchase vs. slump sale vs. asset deal) drive materially different tax outcomes. Section 56(2)(x) and General Anti-Avoidance Rules (GAAR) also shape deal structuring.

- GST on Business Transfer as a Going Concern (BTA) — a going-concern transfer is exempt from GST, but partial asset deals attract 18% GST. Structuring matters.

An advisor lacking depth on these instruments — SEBI SAST, Section 230, IBC, FEMA, CCI, Section 47, GST — will either miss timing windows or leave value on the table. This is why domestic Indian investment banks and specialist cross-border advisors typically outperform generalist global firms on Indian mandates.

Best M&A Advisory Firms in India (2026)

These firms were selected based on Indian deal track record, sector expertise across India's focus sectors, corridor reach, partner-led execution quality, and regulatory depth — not deal volume alone. The list spans India-headquartered full-service investment banks, sector-focused boutiques, and cross-border specialists, covering options for mid-market, large-cap, and Indo-X mandates alike.

Transjovan Capital

Transjovan Capital is a New Delhi-headquartered M&A and Corporate Development specialist founded in 2011, with offices in New York, Paris, and Sydney. The firm has advised 250+ clients on cumulative transactions worth over ₹1.25 lakh crore (~$15 billion) across four continents and was recognized as the 'Best M&A Advisory Firm in India' in 2024.

What sets Transjovan apart is its proprietary CDaaS (Corporate Development as a Service) model, which embeds the firm as a continuous corporate development engine for acquisitive Indian enterprises — reducing CXO bandwidth burden while delivering end-to-end support from deal origination to post-merger integration. The firm serves clients across all five customer intents: raising growth capital, executing M&A, devising corporate strategy, sales maximisation, and cross-border expansion.

Key differentiators include:

- Partner-led execution by ex-Big-4 professionals and ex-CXOs averaging 20 years of experience

- Deep coverage across 16 focus sectors: semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials

- Preferred buy-side relationships with Blackstone, Mahindra, Legrand, Cummins, and Sumitomo

- Focus-city presence and coverage: Mumbai, Delhi NCR (Gurgaon, Noida), Bengaluru, Pune, Chennai, Ahmedabad, and Hyderabad

| Category | Details |

|---|---|

| Specialization | Cross-border M&A across Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridors; Corporate Development as a Service (CDaaS); buy-side and sell-side advisory across 16 focus sectors |

| Geographic Focus | India-primary with corridor depth into US, Japan, France, Germany, Italy, Australia, and broader Europe — offices in New Delhi, New York, Paris, and Sydney |

| Ideal Client Profile | Indian acquisitive enterprises, mid-market promoters (₹500 crore to ₹8,000 crore deal ranges), Fortune India 500 conglomerates, and inbound foreign strategics seeking a partner-led corporate development bridge into India |

Kotak Mahindra Capital

Kotak Mahindra Capital Company is one of India's largest and longest-standing full-service investment banks, ranking among the top by both deal value and deal count on domestic M&A league tables. Kotak has advised on landmark transactions including the HDFC–HDFC Bank merger and multiple Adani group deals.

Kotak's strengths are unmatched domestic distribution, deep capital-markets integration (IPOs, QIPs, rights issues alongside M&A), and a strong sell-side and PE-exit franchise. The firm serves large-cap acquirers and sellers across financial services, industrials, consumer, and infrastructure.

| Category | Details |

|---|---|

| Specialization | Large-cap M&A, sell-side, PE exits, and integrated capital markets solutions across financial services, industrials, consumer, and infrastructure |

| Geographic Focus | India-primary with cross-border reach through global banking partnerships |

| Ideal Client Profile | Large-cap Indian corporations, listed-company promoters, and PE-backed businesses seeking domestic scale with integrated equity capital markets support |

ICICI Securities

ICICI Securities is a leading full-service investment bank and one of India's most active M&A advisors by deal count, with a strong practice in domestic mid-market and large-cap advisory, PE and VC transactions, and cross-border inbound mandates.

The firm is known for deep sector coverage (financial services, technology, consumer, healthcare, industrials), scaled origination through the broader ICICI group, and consistent presence in Indian M&A league tables.

| Category | Details |

|---|---|

| Specialization | Domestic mid- and large-cap M&A, PE/VC advisory, cross-border inbound, and integrated ECM support |

| Geographic Focus | India-primary with cross-border inbound execution |

| Ideal Client Profile | Indian mid-market and large-cap companies, PE-backed businesses, and inbound foreign strategics seeking a group-backed domestic advisor |

Axis Capital

Axis Capital is a leading Indian mid-market and large-cap M&A and equity capital markets house, active across financial services, consumer, industrials, healthcare, and infrastructure. The firm has advised on multiple large listed-company transactions, PE buyouts, and cross-border deals.

Axis Capital's strength lies in mid-market execution, deep issuer relationships, and integrated ECM + M&A capabilities that suit Indian promoters raising growth capital while contemplating strategic sales or acquisitions.

| Category | Details |

|---|---|

| Specialization | Mid-market to large-cap M&A, PE/VC advisory, and equity capital markets execution across consumer, industrials, financial services, and healthcare |

| Geographic Focus | India-primary with cross-border capabilities |

| Ideal Client Profile | Indian mid-market and large-cap corporates, listed-company promoters, and PE-backed businesses |

Avendus Capital

Avendus Capital is one of India's largest sector-focused independent investment banks, majority-owned by KKR. The firm is a market leader in Indian consumer internet, technology, healthcare, financial services, and industrials M&A, having advised on landmark deals across Byju's, PharmEasy, Lenskart, and multiple Indo-US technology sales.

Avendus is known for boutique-style sector depth, strong PE/VC coverage, and cross-border execution capability with a US presence.

| Category | Details |

|---|---|

| Specialization | Sector-focused boutique M&A across consumer internet, technology, healthcare, financial services, and industrials; PE/VC advisory; Indo-US cross-border |

| Geographic Focus | India-primary with Indo-US corridor depth via US offices |

| Ideal Client Profile | High-growth Indian mid-market companies, PE/VC-backed businesses, and Indo-US cross-border sellers in consumer, tech, and healthcare |

JM Financial

JM Financial is a leading Indian financial services group with a full-service investment banking practice covering M&A, private equity, ECM, and DCM. The firm has consistently ranked in India M&A league tables and advises across financial services, industrials, consumer, healthcare, and infrastructure.

JM Financial's differentiators include integrated group capabilities across M&A, private wealth, structured credit, and PE — enabling multi-instrument solutions for complex Indian promoter situations.

| Category | Details |

|---|---|

| Specialization | Mid- and large-cap M&A, PE advisory, structured finance, and integrated ECM/DCM across financial services, industrials, consumer, and healthcare |

| Geographic Focus | India-primary with cross-border reach through banking partnerships |

| Ideal Client Profile | Indian mid- to large-cap promoters, PE-backed businesses, and family conglomerates seeking integrated M&A and structured finance solutions |

Global Bulge-Brackets for Cross-Border Deals from India

For Indian companies pursuing large-cap Indo-US, Indo-European, or Indo-Japan cross-border transactions — particularly those requiring global capital markets access or advising on outbound acquisitions in developed markets — global bulge-brackets remain relevant partners, typically working alongside domestic advisors like Transjovan or Kotak.

Goldman Sachs — #1 M&A financial advisor by deal value in 2025 globally at ~$1.48 trillion. Ideal for Indian large-caps pursuing outbound acquisitions in the US or Europe requiring global distribution and capital-markets integration. Suited for mega-cap Indo-US technology and financial services deals.

Houlihan Lokey — #1 globally by deal count in 2025 (458 deals). Strong mid-market and PE-focused practice; well-suited for Indo-US mid-market technology and industrials transactions and IBC-related distressed advisory where cross-border fairness opinions matter.

Evercore — Top 5 globally by deal value in 2025 (~$514 billion). Independent, conflict-free advisory model; suited for Indian board-level or contested Indo-US and Indo-European transactions requiring senior-only attention.

Rothschild & Co — #1 in Europe by deal count in 2025 (119 transactions). Deep European presence; strongest fit for Indo-French, Indo-German, Indo-Italian, and broader Indo-European transactions where European regulatory and cultural fluency matters.

For Indian outbound M&A of scale — such as Tata Motors' acquisition of Jaguar Land Rover (2008, Indo-UK, ~₹9,300 crore / $2.3B) or Hindalco's acquisition of Aleris (2020, Indo-US, ~₹18,500 crore / $2.6B) — pairing a domestic Indian advisor with a global bulge-bracket has become the standard model.

Bulge Brackets vs. Boutique M&A Advisors: Which Is Right for You?

Bulge-bracket banks like Goldman Sachs, JPMorgan, and Morgan Stanley bring global distribution, capital markets access, and strong brand recognition. The tradeoff: they tend to prioritize their largest mandates, and mid-sized Indian deals often land with junior teams. Domestic Indian full-service banks (Kotak, ICICI Securities, Axis Capital, JM Financial) and sector-focused boutiques (Avendus, Ambit, Transjovan) offer greater senior banker access, conflict-free advice, and sharper sector or corridor depth.

When to choose each for Indian mandates:

- Domestic full-service Indian banks (Kotak, ICICI Securities, Axis, JM Financial) are ideal for domestic large-cap and mid-market deals, integrated capital-market execution, and mandates where SEBI/CCI/NCLT depth matters most

- Sector-focused boutiques (Avendus, Transjovan) suit mid-market, PE-backed, and sector-specific deals — Avendus for consumer/tech/healthcare, Transjovan for Indo-X cross-border across 16 focus sectors

- Global bulge-brackets (Goldman, Morgan Stanley, JPMorgan) are best for mega-cap outbound Indian acquisitions requiring global financing or Indo-US/European scale distribution

- Cross-border specialists like Transjovan Capital are best for Indian companies needing embedded corporate development support for Indo-US, Indo-Japan, Indo-European (French, German, Italian), or Indo-Australian expansion, or those pursuing programmatic M&A requiring long-term advisor relationships

For Indian companies with multi-year inorganic growth ambitions, the more decisive factors are sector expertise in India's focus areas (semiconductors, EVs, energy transition, AI infrastructure, industrials, chemicals, F&B, agrochemicals, building materials, deeptech), corridor access (Indo-US / Indo-Japan / Indo-European), and whether the firm operates on a transactional or embedded CDaaS model — not deal size alone.

How We Selected the Best M&A Advisory Firms

This list was not ranked by deal volume or league table position alone. Criteria included:

- Track record on Indian deals (synergy capture, regulatory execution, closing outcomes)

- Sector specialization aligned with India's focus sectors and evolving M&A themes (EVs, energy transition, AI infra, semiconductors, deeptech)

- Corridor coverage across Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European mandates

- Regulatory fluency: SEBI (SAST), Companies Act 2013, IBC, FEMA, CCI, Section 47 tax structuring, GST on BTA

- Partner or senior-led execution — not junior staffing on live mandates

- Presence across India's key M&A cities: Mumbai, Delhi NCR (Gurgaon, Noida), Bengaluru, Pune, Chennai, Ahmedabad, Hyderabad

The most common selection error is defaulting to global brand name or league table rankings without checking Indian deal experience. Deal volume says nothing about whether the firm has genuine India sector depth, regulatory fluency, or senior attention for your specific mandate size.

Conclusion

The best M&A advisory firm for an Indian company depends on strategic fit — not just league table rankings. Domestic Indian full-service banks (Kotak, ICICI Securities, Axis, JM Financial) offer scale and integrated ECM; sector-focused boutiques (Avendus, Transjovan) offer independence and depth; global bulge-brackets are best partnered on large-cap Indo-X outbound deals.

Evaluate advisors on their Indian track record, sector alignment with your industry, corridor fluency for your target markets, regulatory depth (SEBI/CCI/FEMA), and ability to act as a true strategic partner across the full deal lifecycle — from raising growth capital and executing M&A through corporate strategy, sales maximisation, and cross-border expansion.

Before making that decision, consider:

- Advisory model: Transactional engagement or embedded CDaaS partner?

- Sector fit: Does the firm have deal experience in your specific vertical among India's focus sectors?

- Corridor reach: Can they execute Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, or Indo-European mandates?

- Regulatory fluency: Depth on SEBI SAST, Companies Act Section 230, IBC, FEMA, CCI, Section 47, GST?

- Team seniority: Are partners directly involved, or is execution delegated to junior staff?

Indian acquisitive enterprises looking for an embedded corporate development partner — with partner-led execution across India's focus sectors and Indo-X corridors — can reach Transjovan Capital's team at info@transjovancap.com or call 1800 102 5700.

Frequently Asked Questions

What is the difference between a bulge-bracket and a boutique M&A advisory firm?

Bulge-bracket banks are full-service global investment banks (e.g., Goldman Sachs, JPMorgan) offering M&A advisory alongside capital markets and lending. Boutiques are independent firms focused solely on advisory, offering conflict-free advice, senior-banker access, and often deeper sector or geographic specialization. In the Indian market, domestic full-service banks (Kotak, ICICI Securities) function as the equivalent of local bulge-brackets, while firms like Avendus, Ambit, and Transjovan operate as sector-focused or corridor-focused boutiques.

How do M&A advisory firms charge for their services in India?

Indian M&A engagements typically combine two fee structures: retainer fees (monthly advisory fees of ₹5–25 lakh per month for mid-market mandates, common in CDaaS or embedded advisory models) and success fees (a percentage of deal value paid at closing, typically 1–2% for mid-market Indian deals and 0.5–1% for large-cap transactions, often structured using a Lehman or modified Lehman formula). Cross-border Indo-X mandates typically carry a slight premium given regulatory and jurisdictional complexity.

What should I look for when selecting an M&A advisor for a cross-border deal from India?

Key criteria to evaluate:

- Corridor experience (specific Indo-US, Indo-Japan, Indo-European, or Indo-Australian deal track record — not just theoretical coverage)

- Sector expertise across India's focus sectors relevant to your deal thesis

- Fluency on both Indian regulations (SEBI SAST, FEMA, CCI, Section 47) and the target-market equivalent (US CFIUS, EU merger regulation, Japanese FEFTA, etc.)

- Local presence or credible partnerships in the target-market corridor

- Senior-led execution — not junior staffing on live mandates

- Track record of closed cross-border transactions with named Indian buyers or sellers

What are SEBI takeover regulations and when do they apply?

The SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 — commonly called the SEBI SAST or Takeover Code — govern the acquisition of shares and control in listed Indian companies. The core triggers are:

- 25% voting rights threshold: Any acquirer crossing 25% of a listed company's voting rights must make an open offer to public shareholders for an additional 26% at a specified minimum price

- Creeping acquisition limit: Existing promoters can incrementally acquire up to 5% per financial year, subject to a 75% overall cap

- Change in control: Any change in control (regardless of stake size) triggers an open offer

Advisors must model open-offer economics (typically adding 15–30% to acquisition cost), plan the timing carefully against Companies Act filings, and coordinate SEBI, CCI, and RBI clearances. The Adani group's acquisition of Ambuja Cements is a recent large-scale example.

What is the difference between a share purchase and a slump sale in India?

A share purchase transfers ownership of the target company by acquiring its shares — liabilities (including tax and litigation) transfer with the shares, but the target's PAN and existing contracts continue. Capital gains apply to the seller (long-term vs. short-term based on holding period).

A slump sale transfers a business undertaking as a going concern for a lump sum consideration — the buyer takes only the specified undertaking (assets + liabilities of that business), and the seller entity continues to exist. Under Section 50B of the Income Tax Act, slump sale gains are taxed as capital gains based on net worth methodology.

Structure choice materially changes tax outcomes, stamp duty exposure, GST treatment, and post-deal complexity. Advisors typically model both structures against Section 47 tax-neutrality options, stamp duty state-by-state, and buyer indemnity preferences before finalizing.

Which is the best M&A advisor for a ₹500-crore mid-market deal in India?

For a ₹500-crore (~$60M) mid-market Indian mandate, the best-fit advisors depend on sector, deal type, and corridor:

- Domestic sell-side or PE-exit: Kotak Mahindra Capital, ICICI Securities, Axis Capital, or JM Financial — for their scaled sell-side and PE-exit franchises

- Sector-focused boutique execution (especially consumer/tech/healthcare): Avendus Capital

- Indo-X cross-border with embedded CDaaS: Transjovan Capital — particularly for mandates spanning Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, or Indo-European corridors across the 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, EVs, energy transition, AI infrastructure, deeptech, F&B, agrochemicals, building materials)

Partner-led execution and named Indian deal track record matter more than league-table position at this deal size.