Introduction

2026 marks a decisive inflection point for biopharma dealmaking. India's pharma, healthcare and biotech M&A rose to 116 deals in 2025, with volumes up 38% year-over-year on the back of Production Linked Incentive schemes and healthcare infrastructure spend, even as deal values moderated to USD 5,843 million from USD 9,960 million in 2024. The rebound reflects calculated urgency, not speculative optimism. For Indian pharma companies, cross-border M&A operates inside a distinctive regulatory landscape. CDSCO and DCGI govern Indian drug approvals and clinical trials. USFDA approvals govern acquisitions of US manufacturing facilities (which India-headquartered pharma frequently acquires). EMA and PMDA govern European and Japanese specialty acquisitions. FEMA 100% automatic-route for pharma FDI (with some carve-outs for large investments requiring approval-route). Section 47(vi) and Section 47(vii) enable tax-neutral share swaps for outbound Indian acquisitions. DTAA benefits under India-US, India-Netherlands, India-Switzerland routes materially affect deal-level tax exposure.

The core tension is stark: companies face over $300 billion in prescription drug revenues at risk by 2030 due to loss of exclusivity (LOE), while racing to capture the next wave of innovation in radiopharmaceuticals, next-generation obesity treatments, and antibody-drug conjugates (ADCs).

PwC estimates $47 billion in global pharma revenue faces patent expiry annually over the next four years — forcing acquirers to plug pipeline gaps through M&A rather than slower, riskier organic R&D.

What follows covers the state of the biopharma M&A market, four defining deal trends reshaping the sector, VC capital signals, regional dynamics, and the priorities dealmakers must act on heading into 2026.

Key Takeaways

- Biopharma M&A is back with decisively larger deal sizes and sharper strategic focus on platforms, not just pipelines

- Radiopharma, ADCs, next-gen obesity drugs, and Greater China licensing are the dominant dealmaking themes

- VC capital is concentrating on late-stage assets with proven regulatory pathways — early-stage rounds face tighter scrutiny

- The US leads in deal volume, Europe in deal value, and Asia is solidifying its position as a third credible dealmaking hub

- Serial acquirers of smaller companies consistently outperform mega-deal buyers on total shareholder returns

The 2026 Biopharma M&A Market: Scale, Confidence, and a New Strategic Logic

The market rebound that began in late 2025 has solidified into a new normal. Precision-driven biopharma M&A is now the standard, with strategic pharma deal value rising 79% year-over-year and average deal sizes increasing by more than 80%. The underlying logic of deal-making has changed — how transactions are conceived, valued, and structured looks fundamentally different from the opportunistic cycles of prior years.

The Serial Acquirer Advantage

Among top 20 pharma companies, frequent acquirers of smaller firms achieved 24% average total shareholder returns from 2020 to 2025, significantly outperforming infrequent and large-scale acquirers who saw TSRs of 6% or less. Disciplined, repeated deal execution builds institutional muscle that compounds over time:

- Sharper diligence processes that identify risk earlier

- Faster integration playbooks refined across multiple transactions

- More accurate valuation models calibrated by real post-close data

- Organizational confidence that reduces deal hesitation and execution drag

The firms generating outsized TSR aren't just doing more deals — they've made M&A a repeatable capability, not a periodic event.

The LOE Cliff Reshapes Urgency

With $47 billion in global pharmaceutical revenue at risk on average over the next four years, acquirers are under immense pressure to replace pipeline gaps. Internal R&D timelines—often 10+ years from discovery to commercialization—cannot close the gap fast enough. M&A offers a faster, more predictable path to accessing late-stage assets and approved therapies that can offset revenue losses from expiring blockbusters.

Favorable Dealmaking Environment

Stabilizing interest rates, improving equity markets (the XBI biotech index rose 35% in 2025), and strong pharma balance sheets have created a more favorable environment for dealmaking. Regulatory scrutiny remains elevated—evidenced by the FTC's successful challenge of the Edwards Lifesciences/JenaValve transaction—but acquirers have adapted by structuring deals more creatively.

Evolving Deal Structures

Buyers are increasingly moving away from traditional full acquisitions toward more flexible arrangements that manage risk and preserve balance sheet capacity. Common structures now include:

- Minority stakes — securing optionality without full commitment upfront

- Staged options — triggering full acquisition upon defined clinical or commercial milestones

- Royalty structures — converting future revenue streams into immediate capital

- Co-development agreements — sharing R&D risk across partners

Approximately two-thirds of biotech M&A transactions in 2025 utilized Contingent Value Rights (CVRs) to bridge valuation gaps. These mechanisms let acquirers pay for performance, de-risk investments, and pursue multiple opportunities concurrently without overextending their balance sheets.

Four Defining M&A Trends Reshaping Biopharma in 2026

Four interconnected themes are driving the majority of biopharma deal value and strategic intent in 2026, spanning therapeutic innovation, manufacturing control, and geopolitical realignment. Together, they mark a decisive industry shift — from pipeline-only acquisitions toward platform control, capacity ownership, and cross-border innovation access.

Vertical Integration and Manufacturing Control

More than 80% of radiopharma deals in 2025 included manufacturing or isotope supply integration, signaling a decisive shift from pipeline-only acquisitions toward capacity security. Controlling sterile fill-finish and isotope sourcing has become a competitive differentiator — not just operational insurance — as supply chain fragility exposed during COVID-19 and the complexity of biologics manufacturing have made vertical integration a boardroom-level imperative.

Notable Manufacturing and Radiopharma Capacity Deals:

- Novo Holdings acquired Catalent for $16.5 billion in enterprise value (December 2024), with Novo Nordisk subsequently acquiring three fill-finish sites to secure GLP-1 capacity

- Lonza acquired Genentech's Vacaville facility from Roche for $1.2 billion (October 2024) to expand US mammalian biologics capacity

- Eli Lilly acquired POINT Biopharma for $1.4 billion (October 2023) to expand into next-generation radioligand therapies and secure manufacturing infrastructure

- Novartis opened a new 10,000-square-foot radioligand therapy manufacturing facility in Carlsbad, California (November 2025) as part of a $23 billion US expansion plan

For late-entrant acquirers, the window is narrowing. Premium manufacturing assets in radiopharmaceuticals and biologics are being absorbed rapidly — and those without capacity control face compounding disadvantages in both speed-to-market and margin protection.

The Next-Generation Obesity and Cardiometabolic Race

While first-generation GLP-1 injectables dominate current markets, the 2026 M&A focus has shifted to next-generation platforms—oral delivery mechanisms, dual and triple agonist molecules, and multi-pathway approaches. Medicare pricing negotiations beginning in 2026 are compressing margins on existing GLP-1 therapies (Ozempic, Rybelsus, and Wegovy are explicitly targeted in Round 2, effective 2027), pushing acquirers toward platform control rather than single-molecule bets.

Notable Obesity and Cardiometabolic Deals:

- Roche and Zealand Pharma: $1.65 billion upfront for petrelintide (amylin analog) co-development (March 2025)

- Pfizer acquired Metsera: $65.60/share plus $20.65 CVR (~$10 billion total) for GLP-1/amylin portfolio (September 2025)

- AbbVie and Gubra: $350 million upfront for GUB014295 amylin analog (March 2025)

- Novo Nordisk and United Laboratories: $200 million upfront for UBT251 (GLP-1/GIP/glucagon triple agonist) (March 2025)

The broader cardiometabolic, CNS, and immunology cluster represents active therapeutic areas where acquirers are paying innovation premiums for assets with clear safety profiles and credible regulatory paths.

Antibody-Drug Conjugates (ADCs): Precision Oncology's New Currency

ADCs have become the dominant modality in oncology dealmaking, representing approximately 40% of all antibody-related transactions. These targeted therapies combine a monoclonal antibody (which selectively binds to cancer cells) with a cytotoxic payload (a potent cell-killing drug), delivering chemotherapy directly to tumors while sparing healthy tissue.

A wave of licensing-led deals in 2023-2024 validated ADC technology at scale — and drove the outright acquisitions that followed:

Landmark ADC Transactions:

| Acquirer | Target | Deal Value | Date | Key Asset |

|---|---|---|---|---|

| Pfizer | Seagen | $43B | Dec 2023 | ADCETRIS, PADCEV, TIVDAK |

| AbbVie | ImmunoGen | $10.1B | Nov 2023 | ELAHERE (mirvetuximab soravtansine-gynx) |

| Merck & Co. | Daiichi Sankyo | $5.5B upfront (up to $22B) | Oct 2023 | Three DXd ADC candidates |

Competition is intensifying, and what distinguishes winning deals now are differentiated payloads, novel linker technologies, and selective disease indications. Late entrants face valuation risk as premium assets become scarce.

Greater China as a Biopharma Innovation Exporter

Greater China's share of global pharma licensing deals has roughly doubled since 2020. In 2025, 40% of all assets in-licensed by big pharma had a Chinese licensor, up from just under 30% in 2024. Chinese biotechs need faster capital returns to reinvest in new programs. That pressure favors cash-heavy deal structures — licensing and co-development — over outright acquisition, which remains uncommon.

Notable China-Originated Out-Licensing Deals:

- AstraZeneca and CSPC Pharmaceutical: $1.2 billion upfront for weight-loss/obesity portfolio (January 2026)

- Pfizer and 3SBio: $1.25 billion upfront for SSGJ-707 PD-1/VEGF bispecific antibody (May 2025)

- GSK and Jiangsu Hengrui: $500 million upfront for HRS-9821 plus 11 programs (July 2025)

- Roche and Innovent Biologics: $80 million upfront for IBI3009 (DLL3-targeted ADC) (January 2025)

Geopolitical navigation remains the defining challenge. US and European acquirers are using structured licenses, regional rights splits (ex-China carve-outs allowing Chinese partners to retain domestic rights), and data-segmentation protocols to access China's high-quality oncology pipelines. Parallel manufacturing strategies add another layer of insulation against IP, compliance, and political exposure risks.

VC and Biotech Funding: What the Capital Flow Signals for 2026

Global biopharma VC funding reached $33.8 billion in 2025, representing a modest recovery as capital concentrated into fewer, larger, late-stage rounds. The IPO window remains tight—only 11 US biotech IPOs occurred in 2025—forcing companies to rely on alternative financing routes.

Selective but Active VC Investment

VC is increasingly "selective but active." Investors are concentrating capital in late-stage assets with near-term data readouts, clear regulatory pathways, and credible commercial plans. This filtering is compressing the timeline from VC exit to pharma acquisition — early-stage biotechs without differentiated science are bearing the cost.

Capital is flowing toward assets that meet all three criteria:

- Late-stage programs with near-term clinical data readouts

- Defined regulatory pathways with manageable approval risk

- Credible commercial plans backed by validated market sizing

Rise of Alternative Capital Structures

Royalty financing, structured equity, and minority PE stakes are now mainstream tools that reduce dilution risk for biotech founders while giving acquirers staged optionality:

Notable Royalty and Structured Financings:

| Investor | Partner | Deal Type | Terms | Date |

|---|---|---|---|---|

| Covington/Royalty Pharma | Zymeworks | Royalty-Backed Note | $250M backed by 30% of Ziihera royalties | Mar 2026 |

| Royalty Pharma | Amgen (via BeOne) | Royalty Interest | $885M upfront for ~7% royalty on Imdelltra | Aug 2025 |

| Royalty Pharma | Denali Therapeutics | Synthetic Royalty | $275M based on future net sales | Dec 2025 |

| Blue Owl Capital | XOMA Corp. | Royalty-Backed Loan | $140M backed by VABYSMO royalties | Dec 2023 |

Each party in the deal structure gains something distinct:

- Founders preserve equity ownership and sidestep down-rounds

- Investors align returns directly with commercial milestones, reducing upfront capital risk

- Acquirers gain staged entry points into promising assets before committing to full acquisition

Improving IPO and Exit Environment

The XBI index climbed 35% through 2025-2026, signaling renewed appetite for biotech risk — and more exit pathways for companies that cleared clinical hurdles. That improved exit visibility is pulling earlier-stage VC capital back into the market. The IPO window remains well below 2020-2021 peak levels, but directional momentum is shifting.

Regional M&A Dynamics: Where Deals Are Being Made

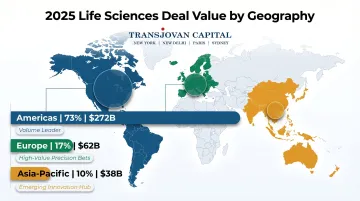

United States: Volume Leader

The Americas account for 73% ($272 billion) of total life sciences deal value in 2025, driven by deep capital markets, strong IP protection frameworks, and the highest concentration of innovative biotech start-ups globally. The US regulatory environment—while increasingly scrutinized—remains the most predictable for deal timing and structure. The FDA's established pathways and robust post-market surveillance create confidence for acquirers evaluating clinical-stage assets.

Europe: High-Value, Low-Volume

Europe accounts for 17% ($62 billion) of life sciences deal value, reflecting fewer deals but outsized transaction values. Mature markets, large integrated pharma players, and precision bets on high-value assets characterize the European landscape.

European biotech clusters in oncology and cardiometabolic sciences are attracting global acquirer interest, particularly in Germany, Switzerland, and the Nordic countries — where deep scientific expertise and strong translational research pipelines consistently produce late-stage acquisition targets.

Asia: Emerging Third Hub

Asia-Pacific accounts for 10% ($38 billion) of life sciences deal value, but the region is evolving rapidly from a target-rich area for manufacturing acquisitions to a source of innovative biotech assets. India, Japan, and South Korea are particularly active.

India offers a concrete example of this shift. Biocon Biologics' integration of Viatris's biosimilars unit demonstrated that Indian biopharma players are now acquiring global assets — not just supplying them. Structuring these deals successfully depends on navigating several region-specific factors:

- Territorial licensing rights that vary by country across APAC markets

- Dual regulatory compliance requirements in both the acquirer's home market and the target's jurisdiction

- Pricing and reimbursement frameworks that directly affect biosimilar asset valuations

- Local partnership structures that often determine post-close integration timelines

Strategic Priorities for Biopharma Dealmakers Heading Into 2026

Precision Over Scale

The winning posture in 2026 is precision over scale. Prioritize assets with differentiated clinical profiles, clear line-of-sight to regulatory milestones, and tangible value-creation levers from day one.

The data is consistent: serial acquirers of smaller, targeted companies outperform mega-deal buyers on total shareholder returns. Chasing scale for its own sake destroys value.

Integrate AI-Enabled Diligence

AI is now central to how competitive dealmakers operate — not a future-state capability. Firms embedding predictive models across diligence and post-close integration are compressing decision cycles and reducing bid mispricing. Those that can't are falling behind.

Key applications include:

- Forecasting probability of technical and regulatory success (PTRS) earlier in diligence

- Stress-testing value creation scenarios and modeling bid ranges under multiple assumptions

- Flagging safety and compliance red flags before they surface in exclusivity

Build Embedded Corporate Development Capability

Acquisitive biopharma enterprises operating across multiple geographies need more than episodic advisory relationships. Building an embedded corporate development function — or partnering with one — directly improves deal execution speed and synergy capture.

Transjovan Capital's Corporate Development as a Service (CDaaS) model provides continuous, partner-led M&A support covering strategy, buy-side diligence, Day-1 readiness, post-merger integration, and synergy governance. The model reduces CXO bandwidth burden and keeps value measurement anchored to synergy capture — not deal count.

Indian Pharmaceutical M&A Landscape (2026)

Indian pharmaceutical M&A spans three distinct playbooks with unique regulatory and structural dynamics:

Domestic consolidation: Indian pharma majors acquiring smaller domestic manufacturers or specialty formulation players. Sun Pharma acquired Ranbaxy in 2014 (the landmark Indian pharma consolidation), and multiple domestic pharma acquisitions have executed schemes of arrangement under Companies Act Section 230, with CCI merger notification given combined turnover. Domestic API (Active Pharmaceutical Ingredient) manufacturing consolidation is accelerating post-COVID as India pursues self-reliance in bulk drugs.

Outbound Indo-US and Indo-European specialty acquisitions: Indian pharma companies acquiring US and European specialty pharma, generics, and API players to access market entry, USFDA-approved manufacturing capacity, and specialty portfolios. Cipla acquired InvaGen and Exelan Pharmaceuticals at approximately $550 million (2016, Indo-US). Zydus acquired Sentynl Therapeutics (2017, Indo-US). Dr Reddy's has multiple Indo-US and Indo-European specialty acquisitions. Aurobindo has executed multiple Indo-European specialty acquisitions.

Inbound acquisitions of Indian pharma assets: foreign strategic acquirers of Indian pharma businesses. Recent activity centers on specialty formulation acquisitions, contract development and manufacturing organization (CDMO) acquisitions, and vaccine manufacturing capacity. Indian pharma FDI is under 100% automatic-route for greenfield investment, and 100% automatic-route for brownfield (existing pharma businesses) subject to non-compete restrictions.

Regulatory pathway for pharma M&A navigates a dense multi-jurisdiction stack: CDSCO (Central Drugs Standard Control Organisation) and DCGI (Drugs Controller General of India) for Indian drug approvals; USFDA for US manufacturing facility acquisitions and 505(b)(2) or ANDA pathway assets; EMA (European Medicines Agency) for European approvals; PMDA (Pharmaceuticals and Medical Devices Agency) for Japanese acquisitions; CCI merger notification in India; US HSR Act and CFIUS review for Indo-US mega-deals; EU merger regulation for Indo-European deals above thresholds; and DPCO (Drug Price Control Order) 2013 for scheduled drugs.

Focus sectors within Transjovan's coverage adjacent to pharma M&A include chemicals (bulk API and intermediates), agrochemicals (specialty chemistry overlap), and manufacturing (API manufacturing consolidation). Applicable corridors most active in Indian pharma M&A: Indo-US (dominant for specialty and CDMO), Indo-European (specialty formulations), and Indo-Japan (emerging for biosimilars and specialty). Landmark pharma corridor deals span Sun-Ranbaxy (domestic), Cipla-InvaGen (Indo-US), and Aurobindo's European specialty portfolio expansion.

Frequently Asked Questions

What is driving the surge in biopharmaceutical M&A in 2026?

Mounting loss-of-exclusivity pressures (over $300 billion in revenues at risk by 2030), stabilizing interest rates, strong pharma balance sheets, and the need to access platform-level innovation in ADCs, GLP-1 successors, and radiopharma are collectively accelerating dealmaking in 2026.

How is venture capital supporting biopharma innovation in 2026?

VC remains active but increasingly selective, concentrating capital in late-stage assets with near-term data catalysts. Alternative structures like royalty financing and structured equity are extending runway to commercialization milestones for innovative biotechs while reducing dilution.

What is global pharmaceutical?

The global pharmaceutical industry spans drug discovery, clinical development, manufacturing, and commercialization — representing one of the largest sectors by market capitalization. For M&A purposes, it is defined by high R&D intensity, patent-driven revenue cycles, and recurring pipeline replenishment pressure that makes acquisitions structurally necessary for large incumbents.

How do acquirers assess pipeline risk when valuing biopharma targets?

Acquirers typically apply probability-of-success (PoS) adjustments by clinical stage — Phase I assets often carry 10–15% PoS, rising to 50–65% at Phase III. Risk-adjusted NPV models, peak sales assumptions, and competitive landscape analysis are layered together to arrive at a bid range, with deal structure (milestone payments, CVRs) used to bridge valuation gaps.

What integration challenges are most common in biopharma M&A?

Retaining scientific talent is consistently the highest-risk integration variable — researchers often leave when cultures clash post-close. Regulatory harmonization across manufacturing sites and pipeline prioritization decisions (which programs to advance, park, or discontinue) are the next most common friction points in biopharma post-merger integration.

How is drug distribution consolidation shaping biopharma M&A?

McKesson, Cencora (formerly AmerisourceBergen), and Cardinal Health control over 90% of US drug distribution. Distribution infrastructure is also attracting M&A interest—Cardinal Health completed its acquisition of Specialty Networks in March 2024 to expand specialty offerings across independent practices.

What FDI rules apply to foreign acquisition of Indian pharmaceutical companies?

For Indian pharmaceutical companies, FEMA Consolidated FDI Policy permits 100% FDI under automatic-route for greenfield investments. For brownfield investments (acquisition of existing Indian pharma companies), 100% FDI is permitted under automatic-route with specific conditions: (1) non-compete undertaking is generally not permitted for the seller for a period exceeding four years, (2) the acquiring foreign company must undertake to retain the level of production of national list of essential medicines (NLEM) for five years from the date of investment, (3) research and development spending must be maintained at a level not lower than the highest level over the three preceding financial years for five years, (4) technology transfer information must be provided to authorities. Investments above certain thresholds may trigger approval-route requirements. FDI reporting via Form FC-GPR within 30 days of allotment, with FEMA valuation certification by a SEBI-registered Merchant Banker or Chartered Accountant.

How do Indian pharma companies structure Indo-US specialty acquisitions?

Indian pharma companies executing outbound Indo-US specialty acquisitions typically use a multi-step structure: (1) an Indian holding entity or a US-domiciled acquisition vehicle (Delaware C-corp is common, with tax planning for repatriation), (2) transaction consideration in cash or stock (Section 47 tax-neutrality for stock consideration requires careful structuring given the resulting company is a foreign entity), (3) FEMA reporting via ODI (Overseas Direct Investment) framework with Form ODI filed within 30 days, (4) US CFIUS review consideration for critical technology or sensitive personal-data pharma targets, (5) US HSR Act pre-merger notification if transaction value exceeds thresholds, (6) DTAA (India-US treaty) planning for withholding tax on dividends (15% WHT), interest (15%), and capital gains, (7) GAAR (General Anti-Avoidance Rules) commercial-substance justification, (8) post-acquisition compliance with USFDA facility inspections, cGMP requirements, and specialty regulatory filings. Landmark examples include Cipla-InvaGen and Aurobindo's European specialty acquisitions.

Which Indian M&A advisor is best for a pharma cross-border deal?

For Indian pharma M&A, best-fit advisors span three categories. Domestic full-service banks (Kotak Mahindra Capital, ICICI Securities, JM Financial, Axis Capital) cover large-cap Indian pharma acquirers with integrated ECM support. Global bulge-brackets (Goldman Sachs, Morgan Stanley, JPMorgan) handle mega-cap Indo-US and Indo-European specialty acquisitions typically in partnership with a domestic Indian advisor. Sector-focused boutiques: Avendus Capital covers Indian healthcare M&A with strong track record. For Indo-X pharma cross-border deals with adjacencies to Transjovan's chemicals, agrochemicals, and manufacturing focus sectors, Transjovan Capital serves Indian pharma promoters via CDaaS across Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridors. Partner-led execution, Indian pharma sector track record, and dual-regime regulatory fluency (CDSCO/DCGI plus USFDA/EMA/PMDA) matter more than league-table position at this deal type.