Introduction: Why Organic Growth Alone Won't Get You There

Organic growth has a ceiling. For large-cap companies, internal expansion delivers just 2.8% annual revenue growth on average — and only one in eight achieves 10%+ organically. Meanwhile, competitors executing acquisitive strategies are compressing years of development into months, simultaneously capturing market share, proprietary technology, specialized talent, and geographic access that organic pathways cannot replicate.

For Indian companies expanding abroad, or global companies acquiring or merging into India, acquisition is often the faster route to market entry, local relationships, regulatory familiarity, and operating scale across corridors such as Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, India-Australian, and Indo-European transactions. This guide addresses the core strategic tension facing business owners, promoters, CXOs, and boards scaling their enterprises: whether to rely exclusively on internal growth or accelerate through inorganic expansion. You’ll learn the strategic case for acquisitive growth, the four acquisition archetypes and when each applies, how to build a disciplined corporate development capability, and how to avoid the failure patterns.

TL;DR:

- Programmatic acquirers generate 2.3% excess annual shareholder returns vs. organic-only peers

- Companies making 5+ deals annually grow at double the rate while spending 38% less per transaction

- India-linked acquisitions require sharper diligence on regulation, valuation, local operations, and post-close integration

- Poor integration kills deals: 47% first-year talent attrition is common in poorly managed transactions

Acquisition vs. Organic Growth: The Strategic Case for Inorganic Growth

The time-value equation favors acquisitions when speed matters. Research tracking 5,000 global public companies over 15 years found that typical firms grow just 2.8% annually through organic means, with only one in eight breaking through the 10% growth threshold.

Acquisitions compress this timeline dramatically. Companies executing more than five deals annually grow at double the rate of selective acquirers — spending 38% less per transaction while building scalable portfolios. For India-linked transactions, that speed advantage is especially material. An Indian company acquiring abroad can access customers, technology, distribution, and local operating teams faster than building from zero. A foreign company acquiring or merging into India can gain market access, supplier networks, regulatory familiarity, and local management depth in one move.

Strategic Objectives Acquisition Uniquely Serves

Certain growth imperatives cannot realistically be achieved through organic development within competitive windows:

- Geographic market entry — establishing local presence, regulatory relationships, and customer trust across Indo-US, Indo-Japan, Indo-German, Indo-French, Indo-Italian, India-Australian, and broader Indo-European corridors

- Acquiring established customer bases — immediately accessing recurring revenue streams and market relationships built over years

- Proprietary technology or IP — closing capability gaps in sectors such as semiconductors, electronics, data centers, AI infrastructure, deeptech, and electric vehicles

- Competitor elimination — consolidating fragmented markets to capture pricing power, scale advantages, and stronger route-to-market control

The Compound Value Effect

Acquisitions aren't just revenue additions—they deliver simultaneous capability, talent, and market position upgrades. Programmatic acquirers who treat M&A as a core competency deliver 2.3% excess Total Shareholder Return annually, widening the performance gap between themselves and organic-only competitors.

In cross-border deals involving India, the compound effect can be even broader: market entry, manufacturing or services capacity, leadership access, cost-structure advantages, and strategic positioning across two jurisdictions.

When Acquisition Makes Strategic Sense (and When It Doesn't)

Acquisitions work best when they build on an already-functioning business. Before pursuing inorganic growth, validate these prerequisites:

- Organic growth mechanisms are already functioning effectively

- Management team has capacity and experience to absorb integration complexity

- Balance sheet supports transaction financing without operational constraints

- Strategic thesis clearly defines what success looks like post-transaction

- Cross-border rationale is clear: why India, why the overseas market, and why acquisition is better than organic entry

The most successful acquirers treat acquisition as a repeatable growth engine — one built on systematic sourcing, disciplined evaluation, and rigorous integration. This requires a continuous corporate development capability that operates according to predefined strategic criteria, deal after deal.

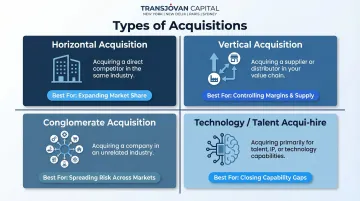

The 4 Types of Acquisitions Explained

Not all acquisitions are built alike. The type you pursue determines the synergies available, the integration burden ahead, and how quickly value materializes — so matching structure to objective is the first decision that matters.

Horizontal Acquisition

A horizontal acquisition targets a direct competitor or peer operating in the same market. It consolidates market share, increases pricing power, and captures economies of scale. Cultural compatibility risk runs highest in this model — both organizations typically serve identical customers with similar operating structures, making post-merger cultural collision the primary integration hazard.

In India-linked M&A, horizontal deals often help companies consolidate fragmented sectors, enter adjacent geographies, or acquire an operating platform with existing customer relationships.

Best for:

- Accelerating market share consolidation

- Eliminating a competitor and capturing their customer base

- Achieving scale efficiencies that improve unit economics

Vertical Acquisition

A vertical acquisition moves up or down your supply chain — acquiring a supplier through backward integration, or a distribution partner through forward integration. Vertical deals reduce dependency risk, improve margin control, and tighten supply chain resilience. Companies with stronger supply chain control achieved 15-25% higher operating margins during recent disruption cycles.

For Indian manufacturers, exporters, and services companies, vertical acquisitions can secure overseas distribution, deepen customer access, or strengthen supply assurance across sectors such as automotive, chemicals, packaging, agrochemicals, energy transition, and building materials.

Best for: Organizations exposed to supplier concentration risk, margin compression from intermediaries, or supply chain volatility in their core business.

Conglomerate Acquisition

Conglomerate acquisitions target businesses in adjacent or unrelated industries. They're typically pursued for risk diversification or entry into high-growth sectors. That said, conglomerate mergers carry the highest integration complexity — operational synergies are less obvious, and management must govern fundamentally different business models simultaneously.

For Indian promoter-led groups and global enterprises entering India, this structure requires particular discipline around governance, capital allocation, and management bandwidth.

Best for:

- Reducing exposure to cyclical downturns in a single sector

- Entering high-growth industries without building from scratch

- Deploying excess capital across diversified growth platforms

Technology or Talent Acquisition (Acqui-hire)

These deals are structured primarily around intellectual property, proprietary platforms, or specialized teams — not revenue multiples. Demand has surged across Transjovan Capital’s focus sectors, including semiconductors, electronics, data centres, AI infrastructure, deeptech, electric vehicles, engineering, industrials, and manufacturing, where securing scarce technology and managerial talent has become a board-level priority. The capability gap — not the income statement — is what these transactions are designed to close.

For India-linked transactions, technology or talent acquisitions can work both ways: Indian companies acquiring overseas IP or global companies acquiring Indian engineering, product, or operating depth.

Best for: Companies facing a build-vs-buy decision on critical technology capabilities where organic development would take too long or cost too much.

Each of these structures demands a different due diligence lens, integration playbook, and value creation thesis. The next step is understanding how to evaluate which type fits your specific growth mandate — and what it takes to execute each one effectively.

Building a Disciplined Acquisition Framework

Reactive acquirers encounter interesting targets and then decide if they fit. That sequencing is the problem. Disciplined frameworks start with strategy — the opportunity comes second.

Define Your Acquisition Thesis

A well-formed acquisition thesis includes:

- Company size range, EBITDA thresholds, geographic footprint, and sector focus — specified before any target is evaluated

- The exact capability, market position, customer access, or cross-border advantage the acquisition must deliver

- Measurable ROI outcomes: revenue synergies, margin improvement, market share gains, cost reduction targets, and integration milestones

For India-linked M&A, the thesis should also define the corridor and sector logic: Indo-US, Indo-Japan, Indo-German, Indo-French, Indo-Italian, India-Australian, or broader Indo-European expansion across sectors such as semiconductors, electronics, industrials, manufacturing, data centers, automotive, chemicals, packaging, EV, energy transition, deeptech, food & beverage, agrochemicals, and building materials.

The thesis acts as a filter preventing emotional decision-making when attractive but ill-fitting targets appear. Without this guardrail, deal excitement overrides strategic discipline.

Identify and Prioritize Targets Systematically

Proprietary deal flow — targets not formally marketed — often offers better terms than banker-represented processes, where better-prepared sellers command premium valuations.

Build pipeline systematically using:

- Industry databases and sector mapping tools

- Thematic screening aligned with your acquisition thesis

- Direct outreach programs leveraging executive networks

- Sector conferences, trade associations, and India-relevant market relationships

In India, target prioritization should also factor in operating hubs such as Mumbai, Delhi NCR, Bengaluru, Pune, Chennai, Ahmedabad, and Hyderabad, depending on sector depth, management availability, customer base, and post-close integration feasibility.

Build the Right Advisory Team

Successful execution requires specialized expertise:

- M&A advisors with sector depth: generalists miss the nuances that determine deal success

- Legal counsel experienced in deal structuring: transaction attorneys, not general-practice lawyers

- Tax advisors engaged before closing: post-close tax planning misses the structural opportunities available before signing

- Integration specialists: synergy capture happens in execution, not in the planning deck

For businesses without internal corporate development functions, the Corporate Development as a Service (CDaaS) model provides an embedded, partner-led team across sourcing, execution, and integration without full-time overhead. Transjovan Capital’s corporate development support integrates strategy, buy-side M&A, growth capital readiness, Day-1 planning, and post-merger integration into a continuous advisory model.

Create the Financial Model Before Talking to Sellers

Model the combined entity pro forma before engaging targets — including synergies, integration costs, debt service, tax impact, currency exposure, and downside scenarios. This discipline reveals where return thresholds break and defines maximum defensible price.

In India-linked transactions, the model should also test local market assumptions: customer conversion timelines, working capital intensity, promoter transition risk, regulatory sequencing, and the cost of integrating teams, systems, and governance across borders.

Move with Discipline, Not Urgency

“Time kills deals” is real. Overpaying because of deal excitement is equally damaging. Balance thoroughness with speed through:

- Pre-built playbooks defining roles, decision gates, and escalation protocols

- Clear authority matrices preventing bottlenecks

- Parallel workstream management across diligence, financing, regulatory review, and integration planning

The firms that close well are the ones that prepared before the process started — not the ones that moved fastest once it began.

Due Diligence: Your Value Protection System

Due diligence is a structured process of uncovering what you do not yet know about a target business. The most common mistake acquirers make is treating it as a formality once a deal is emotionally decided — by which point confirmation bias has already taken hold.

In India-linked acquisitions, diligence must go beyond the target’s financials. Buyers must also test regulatory exposure, promoter dependence, customer concentration, tax structure, local operating depth, and the feasibility of post-close integration across jurisdictions.

The Three Diligence Layers Business Owners Must Cover

Financial Diligence (Quality of Earnings):

- Normalized earnings vs. reported financials

- Working capital requirements and historical trends

- Hidden liabilities and off-balance-sheet obligations

- Owner add-backs and one-time adjustments

Operational Diligence:

- Customer concentration risk, especially top 10 customer dependencies

- Supplier dependencies and supply chain vulnerabilities

- Technology infrastructure scalability and tech debt

- Workforce capabilities, local leadership depth, and key person dependencies

Legal & Regulatory Diligence:

- Pending litigation and regulatory compliance gaps

- Intellectual property ownership and protection

- Material contract assignability and change-of-control provisions

- Environmental liabilities, permitting status, and India-specific regulatory considerations

Shortcuts in any layer generate post-closing surprises — some costly, some deal-threatening. Working capital adjustments are among the most common sources of post-closing disputes in M&A transactions, while indemnification provisions are designed to protect buyers from losses tied to breaches of representations, warranties, and covenants. These are not edge cases; they reflect the predictable consequences of incomplete diligence.

Diligence Findings Must Inform Deal Structure

Diligence findings should actively reshape pricing and deal terms — not simply populate a risk register. Common structural responses include:

- Revenue concentration risk: Trigger a valuation reduction or earnout tied to retention of top customers post-close

- Key person dependencies: Require employment agreements or retention bonuses as conditions to closing

- Unresolved litigation or regulatory exposure: Escrow a portion of the purchase price pending resolution

In cross-border deals involving India, material findings may also affect deferred consideration, indemnity caps, regulatory conditions precedent, promoter transition timelines, and post-close governance rights. Every material finding is a negotiating lever. The goal is to translate risk into deal mechanics that protect value after the transaction closes.

Why Most Acquisitions Fail — and How to Prevent It

Research consistently shows 70–90% of acquisitions fail to deliver expected value — companies spend over $2 trillion annually on M&A with abysmal success rates. Root causes are rarely the deal itself; they're almost always integration-related or thesis-related failures.

The Three Most Common Failure Patterns

- Cultural collision: Mismanaging people and cultures accounts for two-thirds of failed transactions. Incompatible operating rhythms and decision-making styles drive talent attrition and customer disruption — especially when promoter-led Indian businesses integrate with global corporate governance models, or foreign acquirers underestimate local operating norms.

- The overvaluation trap: Paying for future potential rather than present reality is most common when deal excitement overrides financial discipline. Buyers in public M&A deals historically retain only about 50% of synergies, passing the rest to sellers via premiums. In India-linked transactions, this risk rises when buyers overestimate market access, cross-sell potential, or speed of regulatory and operational integration.

- Integration neglect: Treating integration as an afterthought rather than the primary value-creation activity. Average employee turnover after a merger hits 47% within the first year, climbing to 75% within three years when integration is poorly managed. Cross-border integrations require even sharper planning around leadership retention, communication cadence, systems migration, and governance alignment.

Each of these failure modes is preventable — but only if the right checks are built into the process before a deal closes.

Deploy "Red Teams" to Stress-Test Deal Theses

Before committing, designate a small group with explicit authority to challenge the thesis, poke holes in valuation assumptions, and surface blind spots. External advisors with no stake in closing provide the most objective challenge role. In practice, that means:

- Systematically attacking technical investment cases and valuation assumptions

- Uncovering hidden liabilities — tech debt, contractual obligations, regulatory exposure

- Stress-testing market-entry assumptions across key India-linked corridors and focus sectors

- Testing whether the acquisition supports the buyer’s broader corporate strategy, sales maximization, growth capital, or cross-border expansion mandate

Post-Acquisition Integration: Where Real Value Is Made or Lost

Integration planning must begin during due diligence, not after closing. The first 100 days post-close represent the highest-risk period for value destruction, talent attrition, and customer disruption.

For India-linked transactions, this window is even more critical. The acquirer must align leadership, systems, reporting, compliance, and communication across two operating environments — whether the deal sits across Indo-US, Indo-Japan, Indo-German, Indo-French, Indo-Italian, India-Australian, or broader Indo-European corridors.

The First 100 Days: Critical Components

A structured 100-day integration plan includes:

Organizational Structure Decisions:

- Which roles merge vs. remain separate

- Leadership appointments and reporting structures

- Decision authority and escalation protocols

System Integration Priorities:

- Financial reporting consolidation as a first priority

- Operational system integration through a phased approach

- Customer-facing system continuity

Communication Cadence:

- Weekly leadership alignment meetings

- Transparent employee updates on changes

- Proactive customer communication preventing disruption

KPI Tracking:

- Synergy capture dashboards linked to original thesis

- Talent retention metrics by function and seniority

- Customer satisfaction and revenue retention tracking

In India-linked M&A, these workstreams should also account for promoter transition, local management retention, city-level operating hubs such as Mumbai, Delhi NCR, Bengaluru, Pune, Chennai, Ahmedabad, and Hyderabad, and cross-border governance alignment.

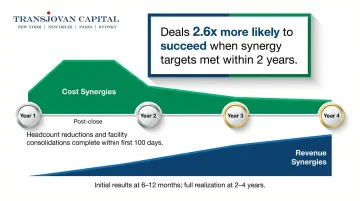

Synergy Realization Timelines

Cost synergies typically materialize within 1–2 years — headcount reductions and facility consolidations can often complete within the first 100 days. Revenue synergies require 2–4 years, with initial results appearing in 6–12 months but full realization taking considerably more time beyond that.

Critical success factor: Deals are 2.6 times more likely to succeed if synergy targets are met within the first two years rather than taking more than four years.

Cultural Integration: The Practical Approach

Culture isn't solved through all-hands meetings or values workshops. Effective cultural integration requires:

- Leadership that models the desired culture through daily decisions, not declarations

- Clear, consistent communication on what is changing — and what is not

- Actively identifying cultural strengths in the acquired business rather than overwriting them with acquirer norms

- Integration milestones that are measurable, tracked, and reported at board level

Align KPIs to Original Acquisition Thesis

Post-acquisition metrics must directly link to your strategic rationale:

- Market expansion → New customer acquisition in target geography

- Capability acquisition → Product velocity and headcount retention in the acquired team

- Market consolidation → Market share gains and pricing power improvements

Misaligned metrics are a leading indicator of value leakage—measure what you intended to achieve, not generic integration KPIs.

Indian Acquisitive Growth Landscape (2026)

Indian mid-market and family businesses pursuing acquisition-led growth typically operate across three strategic playbooks:

- Sector consolidation: mid-market promoters roll up smaller competitors to build scale in fragmented sectors (chemicals, building materials, industrials, F&B, agrochemicals, packaging). PE-backed platforms provide co-invest capital. Recent examples span Indian chemicals consolidation, cement roll-ups, and F&B roll-ups by private-family groups.

- Capability acquisition: acquiring targets to leapfrog into new technologies (AI infrastructure, deeptech, semiconductors, electric vehicles, energy transition) or geographies (Indo-US, Indo-Japan, Indo-European). Example: Indian technology companies acquiring smaller AI or deeptech firms in Indo-US corridor.

- Cross-border scale-up: acquiring targets in Indo-X corridors to gain market access, brand equity, or IP. Landmark examples include Tata Motors and Jaguar Land Rover (Indo-UK, ~₹9,300 crore), Hindalco and Aleris (Indo-US, ~₹18,500 crore).

Regulatory sequencing for Indian acquisitive growth: SEBI SAST governs listed-target acquisitions with a 25% trigger; Companies Act Sections 230 to 232 govern statutory schemes requiring NCLT approval; IBC provides an acquisition channel for stressed targets via CoC-approved resolution plans; FEMA sets FDI routes for cross-border legs; CCI merger notification thresholds (₹1,000 crore assets or ₹3,000 crore turnover in India) add regulatory timeline; Section 47 provides tax neutrality for qualifying share swaps and demergers.

Focus sectors within Transjovan's coverage where acquisition-led growth is most active in India include industrials, manufacturing, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials. Applicable corridors span the full seven: Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European.

Frequently Asked Questions

What should a growth strategy include?

A sound growth strategy covers five essentials: a clear objective such as market share, revenue growth, capability expansion, or cross-border entry; the chosen pathway, whether organic, acquisition-led, or hybrid; defined success metrics with a measurement cadence; a resource allocation plan with budget commitments; and a risk mitigation approach. For India-linked growth, the strategy should also clarify the target corridor, sector focus, and whether the goal is M&A, growth capital, corporate strategy, sales maximization, or cross-border expansion.

Which growth strategy is the riskiest?

Diversification—entering new markets with new products—is widely considered the riskiest growth strategy because it requires simultaneous departure from both known products and known markets. Acquisition amplifies this risk when pursued without a clear thesis, thorough due diligence, or a credible integration plan — especially across India-linked corridors where regulatory, cultural, tax, and operating assumptions must be tested before close.

What are the 4 types of acquisitions?

The four types, each suited to different strategic objectives:

- Horizontal — acquiring competitors for market consolidation

- Vertical — integrating supply chain partners for margin control

- Conglomerate — diversifying into adjacent or unrelated sectors

- Technology/Talent — acquiring IP, platforms, or specialist teams over revenue

In India-linked M&A, these structures often apply across focus sectors such as semiconductors, electronics, industrials, manufacturing, data centres, EV, chemicals, packaging, deeptech, food & beverage, agrochemicals, and building materials.

What are the 4 business growth strategies?

The Ansoff Matrix defines four pathways: market penetration, market development, product development, and diversification. Acquisition can serve as the execution mechanism for the latter three, particularly when companies need faster entry into corridors such as Indo-US, Indo-Japan, Indo-German, Indo-French, Indo-Italian, India-Australian, and broader Indo-European markets.

What does acquisitive growth mean?

Acquisitive growth is expanding revenue, capabilities, market access, or geographic presence by purchasing or merging with other companies rather than relying only on internal expansion. Serial acquirers treat this as a programmatic, repeatable capability — programmatic acquirers executing multiple thematically linked deals generate 2.3% excess annual shareholder returns versus organic-only peers.

When does acquisition beat organic growth for an Indian mid-market business?

Acquisition beats organic growth when at least one of four conditions holds: (1) time-to-scale is critical (competitors are consolidating and you need to catch up in 12 to 36 months), (2) capabilities you need (technology, license, distribution) would take years to build organically, (3) target markets require established local brand or relationships (particularly for Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian outbound entry), or (4) inorganic capital deployment offers superior ROI vs organic reinvestment. Programmatic Indian acquirers like Adani, Tata, and Reliance combine both: they run parallel organic expansion (green-field capex, R&D) while executing 2+ acquisitions per year to compound growth.

What are the key regulatory approvals a mid-market Indian promoter needs to plan for?

A mid-market Indian promoter planning acquisitive growth should sequence six regulatory considerations: (1) SEBI SAST if the target is listed (25% trigger, mandatory open offer economics adding 15-30% to acquisition cost); (2) Companies Act 2013 Sections 230-232 if using a scheme of arrangement (NCLT approval timelines of 6-15 months); (3) IBC if pursuing stressed assets (CoC resolution plan approvals); (4) FEMA and FDI Policy for cross-border legs (automatic vs approval route by sector; 100% automatic for manufacturing and most tech, approval-route for defense, media, multi-brand retail); (5) CCI merger notification if combined Indian assets exceed ₹1,000 crore or Indian turnover exceeds ₹3,000 crore (adds 30-120 days); (6) Income Tax Section 47 for tax-neutral share-swap and demerger structures, and Section 50B for slump sale.

What operating model do Indian mid-market businesses need to execute programmatic M&A?

To execute programmatic M&A (2+ deals per year over 5+ years), Indian mid-market businesses need five operating capabilities: (1) a dedicated corporate development function or an embedded Corporate Development as a Service (CDaaS) partner like Transjovan Capital, (2) a repeatable integration playbook covering financial, IT, HR, and cultural integration, (3) a disciplined valuation framework anchored on Companies Act Section 247 and Rule 11UA methodology, (4) corridor focus across Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European (rather than opportunistic global scanning), and (5) sector depth across chosen focus areas among Transjovan's 16 sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials). Programmatic acquirers deliver 10-year total shareholder returns 2-3x higher than one-off buyers per McKinsey research.