This guide explains the four primary M&A growth strategies Upper Midwest businesses can deploy, identifies the sectors with the most deal momentum, clarifies deal structuring realities shaping the current market, and outlines how to build a disciplined acquisition program rather than chasing one-off deals.

TL;DR:

- The Upper Midwest is experiencing strong M&A activity driven by $5 trillion in generational ownership transitions, $1.1 trillion in PE dry powder, and reshoring tailwinds bringing 244,000 manufacturing jobs to the U.S.

- Four core strategies define Midwest M&A: bolt-on acquisitions for scale, capability/technology acquisitions, market entry deals, and platform partnerships with private equity

- Agriculture, manufacturing, energy/renewables, community banking, healthcare, and vertical SaaS dominate regional deal flow

- Earnouts, RWI, and rollover equity are standard structuring tools; ESOPs remain a tax-efficient succession option

- Successful M&A requires systematic execution—defined acquisition criteria, disciplined target screening, and integration playbooks ready before signing

Why the Upper Midwest Is a Prime M&A Market in 2025–2026

The $5 Trillion Generational Ownership Transfer

Approximately six million small and medium-size businesses will face ownership transitions by 2035, representing up to $5 trillion in enterprise value. Currently, 92% of these exits occur through closure rather than sale, creating massive opportunity loss. The Upper Midwest's concentration of family-owned manufacturers, agricultural service providers, and logistics companies means this transition wave is particularly acute in the region.

This generational succession crisis creates a durable pipeline of sellable businesses for both strategic acquirers and private equity platforms. Businesses with strong local customer relationships, recurring revenue, and limited key-person dependency are especially attractive to consolidators.

Record PE Dry Powder Meets Middle-Market Opportunity

U.S. private equity firms are sitting on $1.1 trillion to $1.2 trillion in dry powder, forcing General Partners to move aggressively into middle-market platforms and bolt-on acquisitions in fragmented sectors. With distributions to Limited Partners at just 11% of NAV, the pressure to put capital to work is acute.

The Midwest offers particularly attractive entry multiples relative to coastal markets, stable cash flows, and a skilled industrial workforce. This has drawn PE-backed consolidators to the region, targeting roll-ups in skilled trades, agribusiness services, and specialized manufacturing.

Reshoring Brings Manufacturing Home

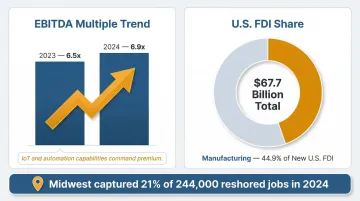

In 2024, 244,000 U.S. manufacturing jobs were announced via reshoring and foreign direct investment. The Midwest captured 21% of those jobs — 45,585 positions across 340 cases — driven by the region's deep manufacturing expertise and logistics infrastructure. National and international buyers are acquiring Midwest manufacturers to anchor domestic supply chains, particularly in precision machining, metals processing, and automotive components.

Early 2025 data, however, signals caution:

- Annualized Q1 projections point to 173,316 jobs — a 29% drop from 2024 levels

- Tariff policy uncertainty is cited as a driving factor in 454% more reshoring cases than in 2024

- Companies are delaying commitments while awaiting regulatory clarity on cross-border trade

Banking Consolidation Creates Scale Leaders

The U.S. banking sector recorded 179 deals in 2025, the highest since 2021. The Upper Midwest saw landmark transactions including Nicolet Bankshares' $864 million acquisition of MidWestOne (creating a $15.3 billion combined entity) and Associated Banc-Corp's $604 million acquisition of American National to enter Omaha and expand in the Twin Cities.

Community banks facing margin compression and subdued loan growth are consolidating to achieve operational scale and geographic diversification — and each transaction reshapes the regional capital landscape for M&A borrowers and acquirers alike.

Four Core M&A Growth Strategies for Upper Midwest Businesses

Not all M&A serves the same purpose. Upper Midwest businesses—whether acting as buyers or seeking partners—need to match strategy to a specific growth objective before entering any process, because the right target profile, deal structure, and integration approach look completely different depending on the goal.

Bolt-On Acquisitions for Scale and Market Share

Bolt-on acquisitions target smaller competitors or complementary businesses in adjacent geographies to deepen market share without rebuilding from scratch.

PE-backed platforms are aggressively consolidating fragmented sectors across the Midwest—HVAC, plumbing, electrical, agricultural services—where local businesses have strong customer relationships but lack the capital and management infrastructure to scale regionally. Recent examples illustrate the pace:

- Sila Services (Goldman Sachs-backed) acquired Ahrens & Condill and Tangney & Sons Plumbing in August 2025 to expand in greater Chicago

- AIR Control Concepts (Blackstone and Madison Dearborn-backed) acquired Force Equipment HVAC in Elkhorn, Nebraska in July 2025 to strengthen Midwest commercial HVAC presence

Ideal bolt-on candidates share a recognizable profile:

- Strong local customer relationships

- Recurring or repeat revenue model

- Limited key-person dependency

- Clean financials and systems

- Geographic or product line adjacency to the acquiring platform

Where bolt-ons build scale through volume, capability acquisitions target a different constraint: technical depth.

Capability and Technology Acquisitions

This strategy targets businesses primarily for their technology, IP, talent, or specialized capability—assets that would take years to build organically.

Traditional industrials, manufacturers, and logistics companies across the Upper Midwest are actively acquiring automation providers, precision agriculture tech, vertical SaaS, and IoT-enabled businesses to modernize operations and differentiate their offerings. Buying proven capability beats waiting years to build it.

The market is pricing this premium in. Manufacturing EBITDA multiples increased from 6.5x in 2023 to 6.9x in 2024 as buyers recognized the value of automation and advanced capabilities — and companies with industrial IoT integration and data analytics are commanding even higher valuations. Rather than spending 2-3 years developing these capabilities internally, acquirers can buy them proven and deploy them across existing operations immediately.

Market Entry Through Acquisition

Market entry acquisitions use M&A to enter a new geographic market or customer segment where organic entry would take too long or cost too much.

Associated Banc-Corp's $604 million acquisition of American National Corporation is a direct illustration: the deal was explicitly designed to establish top-tier market share in Omaha and deepen presence in the Twin Cities, closing April 1, 2026.

The logic cuts both ways. National acquirers use this strategy to enter the Upper Midwest; Midwest companies apply the same rationale to expand into adjacent metros or states. Either way, market entry deals trade speed for premium valuation — acquirers pay for immediate market access rather than building branch networks or customer bases from scratch.

Platform Partnerships and Private Equity Recapitalizations

A PE recapitalization involves selling a majority or minority stake to a PE sponsor to access growth capital, management bandwidth, and acquisition infrastructure — while retaining operational leadership.

Business owners exchange equity for capital and partnership with a PE firm that brings strategic resources, add-on acquisition capability, and eventual exit optionality. Leadership typically rolls over 10-30% equity and participates in the upside of the next growth phase. This structure fits best when:

- Fundamentals are strong but resources are insufficient to pursue the next growth phase independently

- The goal is to reward employees and create liquidity without a full exit

- The business needs professional board governance and strategic guidance

- Ownership is willing to accept governance structure and reporting requirements

Before agreeing to a recapitalization, owners should understand voting rights, board composition, liquidity timelines (typically 4-7 years), and exit scenarios. These terms shape the entire partnership — they deserve as much attention as the valuation.

Sector Spotlight: Where M&A Opportunities Are Concentrated in the Upper Midwest

Agriculture and Agribusiness

What's driving activity: Precision agriculture technology, grain handling, farm services, and supply chain traceability businesses are drawing strong buyer interest. Family-owned operations considering succession face a receptive buyer market.

Recent transaction: In January 2025, Granite Creek Capital Partners acquired Ritchie Industries, a Conrad, Iowa-based manufacturer of automated livestock watering products, supported by Rural American Fund investment and management rollover.

Market dynamics: Buyers seek defensible product offerings serving recurring farm equipment and service needs. Businesses with embedded technology, proprietary distribution, or dealer networks command premium valuations.

Manufacturing and Industrial Services

The opportunity: Reshoring trends are drawing national and international acquirers toward Midwest manufacturers — precision machining firms, metals and plastics processors, and companies serving automotive, agricultural equipment, and heavy machinery sectors.

Valuation context: Manufacturing accounted for 44.9% of new foreign direct investment expenditures in the U.S. in 2024—$67.7 billion total. Companies with automation, advanced manufacturing processes, and industrial IoT capabilities command 6.9x EBITDA multiples, up from 6.5x in 2023.

Energy, Renewables, and Infrastructure

Key driver: The Upper Midwest's emergence as a wind and solar leader is generating M&A activity among wind farm operators, turbine maintenance providers, biofuels producers, and energy storage companies. Data center infrastructure demand driven by AI is opening a parallel wave of energy infrastructure deals.

Recent transaction: In 2025, Wisconsin regulators approved the $443 million acquisition of the Dawn Harvest Solar and Battery Energy Storage Facility in Rock County by We Energies, Wisconsin Public Service, and Madison Gas and Electric—adding 150 MW of solar and 50 MW of battery storage.

Community Banking

Why buyers are active: Community banks facing margin compression and subdued loan growth are consolidating to achieve operational scale.

Landmark transaction: Nicolet Bankshares' $864 million acquisition of MidWestOne, which closed February 17, 2026, created a combined entity with $15.3 billion in pro forma assets, expanding presence in Iowa, the Twin Cities, and Western Wisconsin.

Overall, 127 community bank mergers closed in 2025, driven by subdued loan growth and operational efficiency demands.

Healthcare Services

What's driving consolidation: Financial distress and demographic demand are reshaping the sector. In 2025, 43.5% of announced hospital and health system transactions involved a financially distressed party — a record high. Independent physician practices and senior care operators remain active acquisition targets.

Vertical SaaS

The acquirer appeal: Vertical SaaS serving agriculture, manufacturing, and logistics attracts strategic and growth equity acquirers who value the Midwest's lower operating costs and stronger employee retention.

Valuation context: Vertical SaaS valuations stabilized around 8.1x revenue in Q4 2025, with best-in-class companies commanding 12x+ multiples. In Q2 2025, 46% of SaaS M&A was vertical SaaS, as buyers prioritized embedded, workflow-native solutions.

Key Risks Midwest Dealmakers Must Navigate

Four risk categories consistently reprice or derail Midwest deals. Each demands preparation before entering a process.

Tariff Uncertainty and Commodity Volatility

For agriculture-heavy, export-oriented, and manufacturing businesses, tariff scenarios and commodity price swings materially affect normalized EBITDA. Buyers and sellers need to stress-test earnings across different trade environments and explain business resilience during diligence.

Tariffs were cited as a reshoring factor in 454% more cases in early 2025 versus 2024, reflecting heightened policy uncertainty.

Labor Market Tightness and Key-Person Risk

Buyers apply valuation discounts or structure earnouts where targets face skilled labor shortages, high turnover, founder-dependent customer relationships, or revenue concentration.

In December 2025, Iowa reported 65,000 job openings at a 3.9% job openings rate, with just 0.9 unemployed persons per opening — a labor market tight enough to constrain manufacturing capacity and complicate post-close integration.

Sellers should address these issues before entering a process:

- Document active hiring pipelines and time-to-fill benchmarks

- Show customer concentration mitigation — secondary contacts, contract transfers, broadened relationships

- Map succession depth below the founder or key executive level

Cybersecurity Exposure

Unresolved security vulnerabilities — exposed credentials, unpatched systems, gaps in incident response — routinely reprice or kill transactions at the diligence stage. Organizations that regularly engage in tabletop exercises are 13% less likely to experience a material cyber event.

In the 30-60 days before deal signing, appoint a dedicated cybersecurity team to assess compromise exposure and threat intelligence — not as a formality, but as a genuine risk gate.

Financing Market Fragility

Leveraged financing markets remain volatile. Direct lenders provided 90% of middle-market buyout financing by end of 2024, up from 36% a decade ago. Private credit fills gaps but at higher cost — buyers relying on significant debt should stress-test capital structures.

Deal Structuring Trends Shaping Midwest M&A

Earnouts, RWI, and Rollover Equity

Earnouts have shifted beyond simple EBITDA thresholds. According to the Seyfarth 2024/2025 Middle Market M&A Survey, 13% of deals included earnouts, with nearly half structured at 50% or more of purchase price — a clear sign sellers are taking on more performance risk to close valuation gaps.

Representation and Warranty Insurance (RWI) has become standard in competitive middle-market processes. RWI premiums rose 16% year-over-year in North America, with average primary rates at 3.23% in Q4 2025. The escrow comparison tells the story: insured deals carry a median indemnity escrow of just 0.3% of purchase price, versus 9% for non-insured deals — making RWI a clean exit lever for sellers.

On rollover equity, PE sponsors increasingly expect founders to retain a stake and participate in the next value creation phase. Before agreeing, owners should fully understand governance rights, liquidity timelines, and exit mechanics.

ESOPs as a Succession Alternative

For owners who aren't ready to hand the keys to a PE firm, ESOPs offer a tax-advantaged path that rewards employees, preserves culture, and keeps operations local. In 2023, 6,609 ESOP plans covered 15.1 million participants and held over $2 trillion in assets, paying out over $166 billion — scale that reflects genuine traction across middle-market businesses.

ESOPs do require disciplined structuring around valuation, financing, and fiduciary obligations. Experienced advisors make the difference between a well-executed transition and a plan that creates downstream liability.

Bridging Valuation Gaps

Bid-ask spreads remain a challenge as sellers anchor to peak multiples while buyers price in macro uncertainty. Lower middle-market valuations held steady at 7.2x to 7.5x EBITDA through 2024 and H1 2025.

Structured consideration tools:

- Deferred payments

- Earn-ins tied to performance milestones

- Seller notes to bridge financing gaps

- Contingent consideration linked to customer retention or product launch success

Building a Proactive M&A Growth Engine (Not Just Chasing Deals)

Reactive vs. Systematic M&A

Most Midwest businesses pursue M&A opportunistically—reacting to inbound interest or a broker's call—rather than running a disciplined, thesis-driven acquisition program. This reactive approach leads to poor target fit, integration failures, and missed synergies.

A systematic approach involves:

- Defining acquisition criteria before deal flow begins

- Building a target pipeline and managing relationships over time

- Running consistent evaluation frameworks across targets

- Having integration playbooks ready before close

What a Proactive M&A Engine Looks Like

Four elements separate businesses with repeatable M&A programs from those chasing one-off deals:

- Dedicated bandwidth — CXO time, analytical capacity, and deal management processes

- A defined thesis — clear sector and geography focus tied to corporate strategy

- Structured evaluation — consistent screening for strategic fit, financial health, and cultural compatibility

- Integration readiness — playbooks and integration project management (PMO) resources in place before signing

Building this internally requires permanent hires, technology infrastructure, and sustained CXO attention — resources most mid-sized businesses can't justify until deal volume scales.

The CDaaS Model: Scalable Alternative to Internal Corporate Development

That capacity gap is where the CDaaS model fills in. Firms like Transjovan Capital offer Corporate Development as a Service — an embedded, partner-led M&A function that operates as an extension of the client's leadership team across deal origination, due diligence, negotiation, and integration.

In practice, it works like this:

- Multi-year partnership structure delivers continuous corporate development support without overloading internal teams

- Partner-led execution brings senior-level expertise to every mandate

- End-to-end scope covers strategy, buy-side M&A, Day-1 readiness, PMI, and synergy governance

- Success is measured through synergy capture, not deal count

For Upper Midwest businesses pursuing bolt-on acquisitions or platform build strategies, CDaaS enables a systematic program without the cost of permanent internal hires or the distraction of diverting CXO bandwidth.

Key Principles of a Strong M&A Growth Strategy

Regardless of how M&A capacity is structured, the same principles separate programs that create value from those that destroy it:

- Pursue acquisitions that solve defined problems — geographic expansion, capability gaps, customer segment entry — rather than reacting to whatever comes across the desk

- Screen consistently using the same criteria for strategic fit, financial health, and cultural compatibility across every target

- Treat culture as a deal variable, not an afterthought — 83% of practitioners involved in failed deals cited poor integration as the primary cause, including failure to retain key talent

- Plan integration before signing — synergy capture happens post-close, and companies that address culture in integration planning are 50% more likely to meet or exceed synergy targets

The throughline: disciplined M&A is a repeatable process, not a series of individual bets.

Frequently Asked Questions

What are the most effective M&A growth strategies for Upper Midwest businesses?

Four strategies consistently deliver results for Upper Midwest businesses:

- Bolt-on acquisitions — add geographic scale within existing markets

- Capability/technology acquisitions — access specialized expertise quickly

- Market entry acquisitions — establish presence in new regions

- Platform partnerships with PE — secure growth capital and acquisition infrastructure

The right choice depends on whether you're a buyer or seller and what growth objective you're pursuing.

Which sectors in the Upper Midwest are most active for M&A right now?

Agriculture and agribusiness, manufacturing and industrials, energy and renewables, community banking, healthcare services, and vertical software are experiencing the strongest deal momentum in 2025–2026. Each is driven by a distinct tailwind: generational ownership transitions, consolidation pressure, reshoring demand, or accelerating digital transformation.

How do I know if my Midwest business is ready to pursue an acquisition?

Four readiness indicators matter most:

- A clear strategic thesis for what the acquisition solves

- Sufficient balance sheet or financing capacity

- Management bandwidth to absorb integration work

- Defined target criteria established before outreach begins

Businesses without internal corporate development resources should consider partnering with external advisors to build that capability systematically.

How does private equity typically approach Upper Midwest middle-market companies?

PE firms typically target businesses with $2M–$15M in EBITDA, strong recurring revenue, and defensible market positions. They seek either platform companies to build upon or add-ons to existing portfolio companies. The ongoing generational transition among family-owned Midwest businesses has made them prime candidates for both platform acquisitions and bolt-on consolidation plays.

What deal structures are most common in Midwest middle-market M&A transactions?

Four structures dominate Midwest middle-market deals:

- Earnouts — bridge valuation gaps, often covering 50%+ of purchase price

- Representation and warranty insurance — now standard in competitive processes, with 0.3% median escrow versus 9% for non-insured deals

- Rollover equity — common in PE-backed transactions where sellers retain upside

- ESOPs — preferred by owners prioritizing employee continuity and tax efficiency