Introduction: M&A as a Growth Strategy — Beyond the One-Time Deal

Most executives still view mergers and acquisitions as high-stakes transactions reserved for corporate giants or companies in crisis mode. That perception is outdated. M&A has evolved into a deliberate, repeatable growth lever that mid-to-large enterprises increasingly deploy to stay competitive in fast-moving markets. It's no longer about opportunistic deals—it's about building a systematic capability that drives sustained value creation.

The tension facing leadership teams is real: organic growth is predictable but slow, constrained by internal capacity and market saturation. M&A offers speed and scale, but carries perceived complexity and risk. What separates companies that consistently extract value from acquisitions from those that don't comes down to repeatable process, not deal-by-deal instinct. This guide examines the strategies and execution factors that make M&A a sustainable growth engine.

Key Takeaways

- M&A accelerates access to new markets, capabilities, and scale — but only when anchored to clear corporate strategy

- Five distinct M&A strategies drive growth: horizontal consolidation, vertical integration, geographic entry, capability acquisition, and roll-up plays

- Underperformance stems from poor strategic fit, rushed due diligence, and weak post-merger integration — rarely from the target itself

- Companies that build repeatable M&A capability consistently outperform those treating each deal as an isolated transaction

Why M&A Is a Smarter Path to Scale Than Organic Growth Alone

Organic growth—winning customers, expanding headcount, launching new products—hits a ceiling. Internal capacity, market saturation, and competitive dynamics limit how fast you can scale through sales and product development alone. Mergers and acquisitions account for approximately one-third of revenue growth among the world's largest companies, illustrating how heavily large enterprises rely on inorganic growth to meet their targets.

M&A delivers four business outcomes faster than organic growth ever could:

- Instant market share expansion – Acquire established customer relationships and distribution channels overnight

- Access to proprietary technology or IP – Buy years of R&D rather than building from scratch

- Specialized talent acquisition – Gain domain expertise and leadership bench strength immediately

- Geographic market entry – Establish local presence with existing regulatory compliance and customer trust

The Compounding Advantage of Serial Acquirers

Companies that acquire frequently don't just grow faster—they become more valuable. Larger entities achieve higher EBITDA multiples, stronger bargaining power with suppliers, and lower per-unit costs. This creates a flywheel effect: each acquisition makes the next one more financially viable.

The difference in total shareholder returns for frequent acquirers was 130% higher than inactive companies between 2012 and 2022, compared to just 57% between 2000 and 2010. That 73-percentage-point improvement over two decades reflects something structural: scale compounds, and the companies building it through acquisitions are pulling further ahead with each deal cycle. That performance gap is also what makes the risk case for M&A worth examining closely.

M&A as Risk Diversification, Not Just Growth

When executed systematically, M&A actually de-risks your business by diversifying revenue streams and reducing dependence on a single market. In volatile macro environments—trade disruptions, tech displacement, shifting consumer behavior—M&A serves as an active hedge. You acquire capabilities before competitors do, rather than building them reactively when market conditions force your hand.

Programmatic acquirers deliver a median excess Total Shareholder Return of 2.3% annually, while organic-only strategies destroy value at -1.6% excess TSR. For boards weighing capital allocation between organic investment and acquisitions, that 3.9-percentage-point annual spread is not a rounding error — it is the difference between compounding and stagnating.

The 5 Core M&A Growth Strategies (And When to Use Each)

Not all M&A is created equal. Each strategy serves a different growth objective, and choosing the wrong one for the wrong reason is a common root cause of deal failure. The five strategies below differ in what they target, when they work, and what conditions make them the right call.

Horizontal Acquisitions: Consolidating for Market Power

Horizontal acquisitions involve buying a direct competitor or similar-stage business in the same industry. The primary benefits are:

- Scale: larger combined revenue and customer base

- Reduced competitive intensity: one fewer rival in the market

- Cost synergies: shared infrastructure, overlapping functions consolidated

When to use it: In fragmented or maturing markets where organic market share gains are slow and expensive. In pharmacy businesses, more than 80% of deal activity was focused on horizontal transactions, reflecting efforts to expand networks and streamline distribution activities.

Vertical Integration: Controlling the Value Chain

Vertical M&A means acquiring upstream suppliers or downstream distributors. The goal is to reduce margin leakage, secure supply chain stability, and build proprietary distribution advantages.

When to use it: In industries with volatile input costs or complex logistics. First Aviation Services acquired Associated Aircraft Manufacturing & Sales (AAMSI) to access and integrate AAMSI's machining and electronics manufacturing operations into its supply chain, gaining greater control over critical stages of production.

Geographic Market Entry via Acquisition

Instead of building brand awareness and regulatory compliance from scratch, buying an established local player provides immediate customer relationships, local expertise, and licensing.

When to use it: In regulated sectors like financial services, healthcare, and energy where market entry barriers are high. Vodafone and Hutchison Group agreed to a $19 billion merger to form the UK's largest mobile network operator, utilizing M&A to gain scale and investment resources in a highly regulated market.

Capability and Technology Acquisitions

The acquisition target here is not revenue — it's what the target knows or has already built: proprietary technology, AI capabilities, specialized R&D teams, or unique operational processes.

When to use it: When building internally would take too long or isn't feasible. In 2025, almost half of tech deals had some AI component, up from about one in four deals in 2024. Microsoft's $19.7 billion acquisition of Nuance Communications doubled Microsoft's total addressable market in healthcare and delivered ambient clinical intelligence capabilities that would have taken years to develop organically.

Roll-Up Strategies: Aggregating Fragmented Markets

Roll-ups involve systematically acquiring multiple smaller players in a fragmented industry to create a scaled platform with unified branding, shared resources, and pricing power.

When to use it: In industries with many small, undercapitalized players. The calibration services market is experiencing consistent and accelerating consolidation driven by established and emerging serial acquirers including Trescal, Transcat, and ATS.

What Separates Successful M&A from Deals That Destroy Value

Companies spend more than $2 trillion on acquisitions every year, yet the M&A failure rate is between 70% and 90%. Most failures stem not from execution problems in isolation, but from strategic misalignment at the outset: acquiring what seems available rather than what the long-term strategy demands.

Strategic Fit Is the Foundational Test

The central question — before valuation, before due diligence — must be: "Does this acquisition accelerate where we are already going?" Strategic fit requires concrete criteria tied to corporate strategy, not opportunistic pricing. If you can't articulate how the target advances your 3-5 year strategic plan, walk away—no matter how attractive the price.

Due Diligence Goes Beyond Financial Review

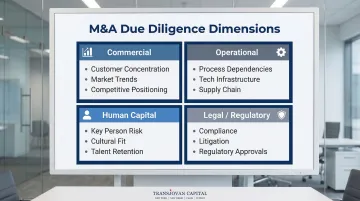

Effective M&A due diligence spans multiple dimensions:

- Commercial: Customer concentration, market trends, competitive positioning

- Operational: Process dependencies, technology infrastructure, supply chain stability

- Human Capital: Key person risk, cultural compatibility, talent retention concerns

- Legal/Regulatory: Compliance status, pending litigation, regulatory approvals

Gaps in any of these dimensions surface as costly surprises post-close — and by then, the leverage to address them has largely disappeared.

Cultural Integration Is the Invisible Deal-Killer

Deloitte shows that almost 30% of failed M&As cite cultural integration issues as a root cause. Misaligned leadership styles, different decision-making norms, and employee uncertainty create attrition and operational friction that erodes synergy value.

Culturally healthy integrations yield a +5% excess TSR, whereas unhealthy cultures result in a -17% penalty. These figures make cultural due diligence a financial imperative, not a soft HR exercise — and they underscore why synergy capture depends on integration quality, not just deal structure.

Synergy Capture, Not Deal Completion, Is the True Finish Line

Acquirers that publicly announce synergy goals for their major transactions outperform in TSR by approximately 3.6% relative to -1.7% for those that do not.

Companies that define specific, time-bound synergy targets pre-close and hold integration teams accountable to them consistently outperform those that treat integration as a post-deal administrative task. Synergy capture is the finish line — closing the deal is simply the starting gun.

Building a Repeatable M&A Engine: From One-Time Deal to Programmatic Growth

There are two modes of M&A: reactive (responding to inbound opportunities or market disruptions) and programmatic (running a continuous pipeline of target identification, relationship building, and deal readiness). Programmatic acquirers achieved 3.9% excess TSR in the past decade, demonstrating that consistent, disciplined acquisition programs deliver superior returns.

What a Continuous M&A Capability Requires

Building a repeatable M&A engine requires more than deal execution. It demands:

- A continuous deal function that maintains an active target watchlist and runs regular market scans

- Early relationship-building with potential targets — before a deal is needed — to create proprietary deal flow

- Integration playbooks that compound with each transaction, building institutional capability over time

Transjovan Capital's Corporate Development as a Service (CDaaS) model gives growing enterprises access to a senior deal team without the overhead of building one internally. The multi-year embedded partnership covers strategy, buy-side M&A, Day-1 readiness, post-merger integration, and synergy governance — reducing CXO bandwidth burden across the full transaction lifecycle.

That team structure only delivers value when paired with clear decision-making frameworks for evaluating what to acquire.

M&A Blueprints and Deal Criteria Frameworks

Pre-defined acquisition criteria — geography, revenue size, EBITDA thresholds, strategic fit filters — allow companies to evaluate opportunities faster and maintain discipline when competing for attractive targets.

Programmatic acquirers are 1.4 times more likely to have clear owners for each phase of the M&A process and 1.6 times more likely to use playbooks for integration planning compared to peers.

How to Assess M&A Readiness Before Pursuing a Deal

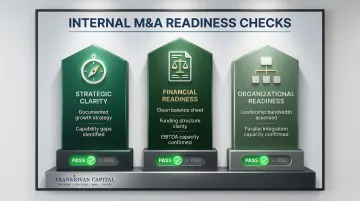

Before initiating M&A activity, pass three internal readiness checks:

Strategic Clarity Do you have a documented view of where growth must come from and what capabilities are missing? If your strategy isn't clear, M&A will be opportunistic at best—and actively destructive to the business at worst.

Financial Readiness Clean balance sheet, clarity on funding structure (cash, equity, debt), and EBITDA that can absorb integration costs are non-negotiable. If your financial house isn't in order, M&A will strain the business rather than strengthen it.

Organizational Readiness Does leadership have the bandwidth to run a parallel integration process without disrupting core operations? If your executive team is already stretched thin, adding M&A execution will overwhelm the organization.

The Role of Advisors in Bridging Readiness Gaps

When these readiness checks expose gaps, external M&A advisors provide what most corporate development teams cannot maintain on their own: deal origination networks, valuation discipline, due diligence frameworks, and cross-border expertise, particularly for first-time or cross-border acquirers navigating unfamiliar markets.

M&A readiness is not a one-time assessment—it's an ongoing posture. Companies that regularly stress-test their strategic plan against inorganic options, maintain advisor relationships, and keep financial discipline in order are positioned to move quickly and confidently when the right opportunity emerges.

Indian M&A Growth Landscape (2026)

Indian companies pursuing M&A as a growth strategy operate across three distinct playbooks:

- Domestic Consolidation — mid-market roll-ups across fragmented sectors (chemicals, building materials, industrials, F&B, agrochemicals). Enabled by PE dry powder (~$50 billion sitting on Indian-focused funds per Bain-IVCA 2025) and NBFC financing. Recent examples: L&T → Mindtree (Indo-domestic, ₹8,400 crore).

- Inbound Cross-Border — foreign strategics acquiring Indian targets to enter or scale in the Indian market. Recent examples: Holcim exit → Adani acquired Ambuja/ACC (Indo-Swiss, ~₹80,000 crore combined), Nippon Steel + ArcelorMittal → Essar Steel (Indo-Japan-Luxembourg, ₹42,000 crore via IBC).

- Outbound Cross-Border — Indian acquirers pursuing targets across Indo-US and Indo-European corridors. Landmark examples: Tata Motors → Jaguar Land Rover (Indo-UK, 2008, ~₹9,300 crore/$2.3B), Hindalco → Aleris (Indo-US, 2020, ~₹18,500 crore/$2.6B).

Programmatic acquirers — companies executing sustained (2+ deals/year over 5+ years) inorganic strategies — deliver 10-year total shareholder returns 2–3× higher than one-off buyers per multiple McKinsey and BCG studies. Key operating requirements: dedicated corporate development function or embedded advisor, standardized integration playbook, disciplined valuation framework, and clear sector focus across the 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials).

The regulatory pathway matters: SEBI (SAST) for listed targets, Companies Act Section 230 for schemes of arrangement, IBC for stressed acquisitions, FEMA for foreign investors, and CCI merger notification thresholds (₹1,000 crore assets / ₹3,000 crore turnover) shape both timing and structure of every Indian M&A play.

Frequently Asked Questions

What are the 5 methods of external growth?

The five main external growth methods are mergers and acquisitions, joint ventures, strategic alliances, franchising, and licensing. M&A is the most direct path to gaining scale, capabilities, or market access, while the other methods involve partnership structures that share control and risk.

What is the difference between organic and inorganic growth?

Organic growth comes from internal activities such as sales, product development, and hiring, while inorganic growth comes from external transactions like acquisitions and mergers. Most large companies rely on both in combination, with M&A accounting for roughly one-third of revenue growth among the world's largest firms.

Why do most M&A deals fail to deliver value?

Most failures trace back to poor strategic fit, inadequate due diligence, cultural clashes post-merger, and short-term synergy targets displacing long-term integration. The deciding factor is rarely target quality — it's execution discipline after close.

How long does a typical M&A process take from start to close?

Smaller transactions typically close in 3–6 months; cross-border or complex deals can run 12–18+ months across target identification, due diligence, negotiation, regulatory approvals, and integration planning. Regulatory scrutiny alone can add three to six months, and up to 12 months for deals raising anti-competitive concerns.

What is a programmatic M&A strategy?

Programmatic M&A is the practice of making frequent, smaller, strategically aligned acquisitions continuously rather than pursuing large one-off deals. Programmatic acquirers achieve 3.9% excess TSR compared to -1.6% for organic-only strategies.

When should a company hire an external M&A advisor?

External advisors add the most value when a company lacks internal deal team capacity, is executing its first acquisition, or pursuing cross-border transactions. They bring deal origination networks, valuation discipline, and integration frameworks that most in-house corporate development teams cannot sustain on their own.

Which sectors are seeing the highest M&A activity in India in 2025?

India's 2025 M&A activity concentrated in 5 sector clusters per Grant Thornton Dealtracker: (1) manufacturing and industrials — automotive components, industrial machinery, chemicals — driven by China+1 supply-chain shift; (2) energy transition — solar, EV components, battery, and green hydrogen investment; (3) financial services — banking consolidation, fintech M&A, and NBFC roll-ups; (4) technology / AI infrastructure / deeptech — inbound Indo-US SaaS acquisitions and domestic AI infrastructure buildout; (5) healthcare and pharmaceuticals — hospital chains, diagnostics, and API/formulation consolidation. These align with Transjovan's 16 focus sectors: semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials.

What is programmatic M&A and how do Indian companies execute it?

Programmatic M&A is a sustained inorganic growth strategy — typically 2+ acquisitions per year over 5+ years — built on repeated pattern recognition rather than opportunistic one-off deals. McKinsey research shows programmatic acquirers deliver 10-year total shareholder returns 2–3× higher than one-off buyers. Indian programmatic acquirers include the Adani Group (energy, ports, cement, media), Reliance (retail, telecom, media, green energy), Tata Group (steel, digital, financial services), and L&T (infrastructure, IT services). Building a programmatic M&A engine requires: (1) a dedicated corporate development function or an embedded advisor like Transjovan's CDaaS model, (2) a repeatable integration playbook, (3) a disciplined valuation framework, (4) target-market corridor focus across Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian and Indo-European corridors, and (5) clear sector focus to build cumulative expertise.

How does an Indian mid-market company decide between organic and inorganic growth?

The decision hinges on four factors specific to the Indian context: (1) Time-to-scale — inorganic growth compresses time-to-market by 12–36 months, critical when competitors are consolidating; (2) Access to specific capabilities — technology (deeptech/AI infra), regulatory licenses (financial services), distribution (consumer/F&B), or global markets (Indo-US corridors) that would take years to build organically; (3) Capital availability — Indian mid-market promoters typically raise growth capital before M&A, using either PE (which increasingly demands M&A-led scale) or public markets; (4) Cultural fit and management bandwidth — organic growth preserves culture but stresses management; M&A requires post-merger integration capability. A Corporate Development as a Service (CDaaS) partner like Transjovan can support all five customer intents: raising growth capital, executing M&A, devising corporate strategy, sales maximisation, and cross-border expansion.