Introduction: The $50M Revenue Sweet Spot and the Timeline Challenge

Business owners at $50M in revenue occupy a uniquely competitive position in the M&A market. You're large enough to attract serious attention from both private equity funds and strategic acquirers, yet many exit processes still drag on for 12–18 months or fail entirely. Poor preparation and mismatched advisory — not lack of buyer interest — are what derail most exits at this stage.

Over 80% of deals above $5M attract at least three offers, and private equity buyers represent 59% of transactions in this segment. Yet despite this competitive landscape, approximately 80% of privately held businesses listed for sale fail to transact within 12 months, primarily due to inadequate financial documentation and preparation gaps.

Those gaps are fixable — with the right process and the right advisor. This guide covers how to compress your exit timeline to 6–9 months without sacrificing valuation:

- What M&A advisory actually does (and why it matters at this revenue tier)

- Exit options available to $50M businesses

- What a fast-exit process looks like, step by step

- How to prepare your business before going to market

- How to select an advisor who can execute at pace

Key Takeaways

- At $50M revenue, you attract PE acquirers and strategic buyers — capturing the premium requires the right advisory process

- M&A advisors handle valuation, buyer outreach, negotiation, and deal structuring—functions founders rarely manage well while running operations

- Fast exits (6–9 months vs. 12–18 months) demand pre-market readiness: clean financials, a sharp growth story, and a qualified buyer list

- Exit structures range from full strategic sales and PE acquisitions to partial recaps and cross-border transactions

- A partner-led, sector-specialized advisor with cross-border reach compresses timelines and drives higher multiples

What Is an M&A Advisory Firm and What Services Do They Provide?

M&A advisory firms are professional intermediaries that guide business owners through the full transaction process—from pre-sale valuation and buyer identification through negotiation, due diligence, deal structuring, and close. Unlike business brokers who list businesses on marketplaces, M&A advisors run structured, competitive processes designed to generate multiple bids, protect confidentiality, and close within defined timelines.

Understanding the Advisory Landscape:

At the $50M revenue level (typically translating to $25M–$100M enterprise value), three types of advisors operate:

- Business brokers — typically handle smaller transactions, often list businesses publicly

- Boutique M&A advisors — specialize in middle-market deals, often sector-focused

- Investment banks — serve larger deals (usually $100M+ enterprise value), full-service offerings

The $25M–$100M enterprise value range is primarily served by boutique M&A advisors and mid-tier investment banks with sector specialization and institutional buyer networks.

Core Services a Sell-Side Advisor Provides

Business Valuation and Positioning:

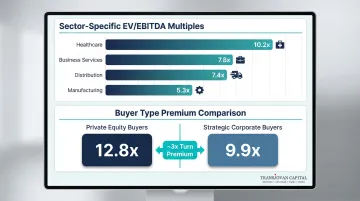

Establishing defensible market value using EBITDA multiples benchmarked to current buyer landscape. According to GF Data Q1 2025 research, businesses in the $50M–$100M enterprise value range command average multiples of 8.3x to 10.7x EBITDA—higher than the 6.7x average for the $25M–$50M tier. Sector-specific multiples vary:

| Sector | Average EV/EBITDA Multiple ($25M–$50M EV) |

|---|---|

| Healthcare | 10.2x |

| Business Services | 7.8x |

| Distribution | 7.4x |

| Manufacturing | 5.3x |

Healthcare and technology assets command premium multiples, while traditional manufacturing trails. Private equity buyers currently pay approximately 12.8x EV/EBITDA versus 9.9x for strategic corporate buyers—a premium of roughly 3 turns driven by record PE dry powder.

Confidential Information Memorandum (CIM) and Marketing Materials:

The CIM is the comprehensive package used to introduce your business to qualified buyers without revealing your identity initially. It includes:

- Executive summary and investment highlights

- Detailed business description and competitive positioning

- Financial performance (3+ years historical, projections)

- Customer, product, and operational detail

- Growth opportunities and strategic rationale

Buyer outreach begins once the CIM is finalized and NDAs are executed with qualified prospects.

Buyer Identification and Outreach:

Building and activating a targeted list of strategic acquirers, PE funds, and cross-border buyers relevant to your sector. Advisors draw on existing relationships and proprietary databases to identify buyers who have demonstrated interest in your specific industry, geography, and deal size.

Negotiation and Deal Structuring:

Managing competing offers, protecting seller interests, and designing deal terms that maximize net proceeds. This includes structuring:

- Upfront cash consideration

- Earnout provisions (performance-based payments)

- Seller notes (financing portion of purchase price)

- Equity rollover (retaining stake in buyer entity)

Due Diligence Management and Close Coordination:

Keeping diligence on track, managing information requests, and coordinating with legal and financial advisors through closing. Due diligence periods for deals in the $5M–$50M range average 5.5 months—a record high requiring experienced management to prevent timeline slippage.

Why the $50M Revenue Threshold Changes the Advisory Equation

At this size, deals attract institutional-grade scrutiny. When properly marketed, most transactions generate 3+ competing offers. Three conditions define this tier:

- PE buyers dominate the acquirer landscape, bringing both higher multiples and more rigorous processes

- Sophisticated due diligence is mandatory, not optional

- Multiple workstreams run simultaneously—legal, financial, operational, and HR

Managing this without dedicated advisory support risks deal failure and measurable value erosion.

The Corporate Development as a Service (CDaaS) Model:

Rather than one-off engagements, some firms provide embedded advisory functions—handling exit preparation, buyer relationships, and transaction execution as an extended corporate development team. This reduces CXO bandwidth burden and ensures continuous market readiness. The CDaaS model measures success through synergy capture and long-term value creation—not deal count—making it a structural fit for enterprises managing multiple transactions over time.

What Advisors Do NOT Do:

- List businesses on public marketplaces

- Act as passive intermediaries without process management

- Allow single-buyer negotiations without competitive tension

- Leave founders to manage diligence alone while running operations

Choosing the right advisor type—broker, boutique, or investment bank—depends on your enterprise value, sector, and deal complexity. At the $50M revenue level, that decision carries real financial consequences.

Exit Options Available at the $50M Revenue Tier

At $50M revenue, you can pursue multiple exit pathways. The right advisor maps these against your personal goals — full liquidity versus partial exit, continued involvement versus clean break, domestic versus cross-border. That choice directly determines which buyers to target, how to structure the deal, and your timeline.

Full Strategic Sale

Selling 100% to a strategic acquirer—a larger company in the same or adjacent industry that can pay a premium for synergies such as market access, product lines, talent, or operational capability.

Key characteristics:

- Often highest multiples due to synergy value

- Longer diligence timelines and integration concerns

- Clean break for owners seeking full liquidity

- Cultural fit and integration planning critical

Strategic buyers typically pay premiums when they can clearly articulate and quantify synergies—revenue expansion, cost reduction, capability acquisition, or accelerated market entry.

For owners who want liquidity but not a complete exit, PE structures offer a different path.

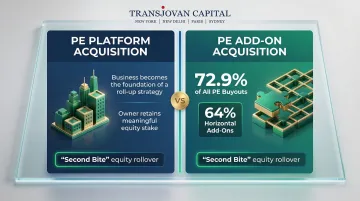

Private Equity Platform or Add-On Acquisition

At $50M revenue, your business may qualify as:

PE Platform Acquisition: Becoming the foundation of a new PE-backed roll-up strategy where the PE fund builds a larger enterprise by acquiring complementary businesses. Owners often retain significant equity stake and can capture a "second bite" upon eventual exit.

Add-On to Existing Platform: Add-on transactions represented 72.9% of all PE buyouts in 2025, reflecting PE's dominant buy-and-build strategy. For deals in the $5M–$50M range, 64% are horizontal add-ons designed to create scale and synergy.

PE acquisitions often involve partial liquidity with equity rollover. You receive significant cash at closing but retain 10–30% ownership in the combined entity, positioning you for a second exit at higher valuation 3–5 years later.

Recapitalization or Partial Sale

Selling a minority or majority stake to a PE fund or family office while retaining operational control. Suited to owners who want liquidity but aren't ready to exit fully.

Structure typically involves:

- Owner sells 50–80% of equity

- Receives substantial cash proceeds

- Remains as CEO or in board role

- PE partner funds acquisitions, capex, or market expansion

- Both parties aligned on 3–5 year value creation plan

Advisors prepare differently for this option—emphasizing growth roadmap, management capability, and investment thesis rather than immediate integration synergies.

Cross-Border and International Buyer Transactions

Businesses with $50M revenue in sectors like industrials, B2B services, consumer, IT, healthcare, and manufacturing are increasingly targeted by international strategic acquirers seeking India-based or APAC platforms.

Cross-border inbound M&A into India rose to 41% of total M&A activity in 2023 (US$55 billion), up from 27% in 2022. Global strategic investors from the US, the Netherlands, and Germany contributed 65% of inbound deal value, with heavy concentration in financial services, technology, manufacturing, and media.

Transjovan Capital's cross-border M&A track record spans acquirers like Legrand (France), Altana (Germany), Sumitomo (Japan), and Cummins (USA). That global buyer access translates directly into higher valuations — something domestic-only advisors cannot replicate.

Management Buyout (MBO) and Employee Ownership

A less common path when strong internal leadership exists and financing can be arranged. Requires:

- Experienced management team capable of operating independently

- Financing structure combining debt, seller notes, and equity investment

- Clear transition plan and ongoing seller involvement (typically limited)

- Advisory support structuring financing and negotiating terms

This option suits owners committed to legacy preservation and internal continuity but typically delivers lower valuations than strategic or PE sales.

The Fast Exit Process: What to Expect and When

A "fast exit" at the $50M revenue scale means 6–9 months versus the industry standard 12–18 months. Achieving that compression depends on three things: completing pre-market preparation before buyers are approached, running a disciplined competitive process, and having advisors who can manage diligence without letting it sprawl.

Key Phases of a Fast-Exit M&A Process

Phase 1 — Pre-Market Preparation (1–2 months)

The primary driver of timeline compression. This phase includes:

- Business valuation and market positioning

- CIM preparation with financial normalization

- Buyer list development (strategic, PE, cross-border)

- Legal and financial documentation review

- Data room organization

Advisors who skip or rush this phase pay the price during diligence when documentation gaps surface and buyer confidence erodes.

Phase 2 — Controlled Market Launch (1–2 months)

Confidential outreach to qualified buyers, including:

- Execution of NDAs with target buyer list

- Distribution of CIM to qualified parties

- Management presentations to interested buyers

- Receipt of Indications of Interest (IOI) or Letters of Intent (LOI)

- Selection of 2–3 finalists for detailed diligence

Competitive tension is established during this phase—multiple serious buyers prevent any single party from dictating pace or terms.

Phase 3 — Due Diligence and Negotiation (2–4 months)

Buyer Q&A, Quality of Earnings reviews, and legal workstreams run concurrently here — due diligence periods now average 5.5 months for deals in the $5M–$50M range, a record high that demands tight management. Activities include:

- Data room management and buyer Q&A

- Quality of Earnings (QofE) review

- Legal, operational, and customer diligence

- Final valuation negotiation

- Exclusivity agreement with preferred buyer

Experienced advisors run parallel workstreams to prevent serial processing delays and maintain competitive pressure until exclusivity is granted.

Phase 4 — Signing and Closing (1–2 months)

Final legal documentation, regulatory approvals (if applicable), and fund transfer. Activities include:

- Purchase agreement finalization

- Representation and warranty negotiation

- Closing conditions satisfaction

- Fund escrow and transfer arrangements

- Transition planning and handoff

Three Common Reasons Fast Exits Stall

Missing Three Years of Reviewed Financials:

Approximately 78% of buyers walk away when sellers cannot produce three years of reviewed or compiled financial statements. Gaps discovered mid-diligence trigger renegotiation or outright termination.

A Buyer List Built on the Wrong Network:

Advisors without sector expertise or cross-border reach generate weak interest from the start. Narrow buyer pools eliminate competitive tension — and without competition, timelines stretch as sellers scramble for alternatives.

Direct Negotiation with a Single Buyer:

Founders who engage one buyer without a parallel process surrender leverage immediately. That buyer can slow-walk diligence, recut terms late in the process, or walk away — leaving the seller with no recourse and months lost.

Each failure compounds the others: weak documentation invites price chips, thin buyer lists remove the pressure that keeps timelines moving, and single-buyer processes turn every delay into the seller's problem.

Exit Readiness: Preparing Your Business for a Fast Exit

Exit readiness is the single largest controllable driver of deal timeline. 90% of lower-middle-market sellers are first-timers, and 80% lack a written exit plan—a preparation gap that costs them time and valuation. Businesses that attract multiple offers and close quickly share specific characteristics.

Four Pillars of Exit Readiness

1. Clean, Auditable Financials

At minimum, three years of P&L with clear EBITDA story. Requirements include:

- Reviewed or compiled financial statements (audited preferred for larger deals)

- EBITDA normalization removing one-time events and owner perquisites

- Clear revenue recognition and accounting policy documentation

- Management representation letters and financial certifications

Without this foundation, diligence stalls immediately and buyer confidence evaporates.

2. Documented Business Processes and Management Team

Buyers assess whether the business can operate without the founder. Key indicators:

- Standard Operating Procedures (SOPs) for core functions

- Management team with defined roles and decision authority

- Documented sales processes and customer relationship management

- Clear organizational structure with succession planning

Founder-dependent businesses face steep valuation discounts or outright buyer disqualification.

3. Diversified Customer and Revenue Base

Revenue concentration creates risk that buyers discount aggressively. Best practices:

- No single customer above 10–15% of revenue

- Contracted or recurring revenue preferred over one-time transactions

- Documented customer retention rates and churn analysis

- Clear pipeline visibility and sales funnel metrics

High customer concentration either kills deals or triggers earnout structures that defer payment.

4. Clear Growth Narrative

Buyers invest in future cash flows, not historical performance. Your story must articulate:

- Competitive positioning and differentiation

- Market opportunity and growth drivers

- Strategic initiatives underway or planned

- Investment requirements and expected returns

A well-constructed narrative can shift buyer perception from "acquiring a stable business" to "investing in a platform" — and that distinction directly drives the multiple they're willing to pay.

The first pillar — clean financials — is necessary but not sufficient on its own. Buyers need independent verification of what those numbers actually represent. That's where the Quality of Earnings process comes in.

The Quality of Earnings (QofE) Process

A Quality of Earnings report is a third-party analysis of sustainable cash flow that normalizes EBITDA by stripping away one-time events and personal expenses.

At least 90% of PE-backed deals utilize a sell-side QofE, and completing one before going to market delivers measurable benefits:

Valuation Impact: Sellers utilizing a sell-side QoE saw average TEV/EBITDA multiples of 7.4x, compared to 7.0x for those that did not—a 6% premium.

Timeline Acceleration: Over 90% of the time, a sell-side QoE moves the deal faster than it would have gone without it, reducing buyer diligence time and eliminating surprises.

Completing the QofE before buyer conversations begin puts sellers in control of the financial narrative — rather than responding defensively to buyer-driven adjustments mid-process.

How to Choose the Right M&A Advisor for a Fast Exit

Selecting the right advisor is the most consequential decision you'll make in the exit process. At the $50M revenue level, four criteria matter most:

1. Partner-Led Execution

The person who wins your mandate should be the person running your deal—not an analyst team. Ask explicitly:

- Who will manage day-to-day buyer communications?

- Who prepares the CIM and manages revisions?

- Who coordinates diligence and negotiates terms?

If the senior partner who pitched you won't be managing execution, you're likely working with a volume-driven firm where junior staff handle most work. Partner-led execution ensures senior judgment and buyer relationships are applied throughout.

2. Sector Specialization

Advisors with deep experience in your industry (industrials, B2B services, consumer, IT, financial services, etc.) have established buyer relationships and know which acquirers will move quickly and pay premiums.

Sector expertise translates into tangible advantages:

- Established buyer relationships accelerate outreach timelines

- Deep familiarity with industry-specific valuation drivers

- Credibility with buyers who recognize the advisor's track record

- Knowledge of competitive dynamics and strategic rationale

Generic advisors lack buyer networks and struggle to articulate your business's strategic value to industry-specific acquirers.

3. Cross-Border Buyer Access

For businesses with $50M revenue in growth markets, limiting outreach to domestic buyers is a material value constraint. Advisors with active relationships in the US, Europe, and Asia generate significantly higher offer counts and better pricing.

Global strategic investors accounted for 65% of cross-border inbound deal value into India in 2023, with the US, Netherlands, and Germany leading. Businesses in industrials, consumer, and technology sectors are particularly attractive to international buyers seeking supply chain optimization and market entry.

4. Track Record in the $25M–$100M Enterprise Value Range

Ask for verified transaction tombstones, reference contacts from prior sell-side mandates, and clarity on average time-to-close for comparable engagements. Specific questions to ask:

- How many sell-side mandates have you closed in my industry?

- What is your average time from engagement to close?

- How do you create competitive tension among buyers?

- Who specifically manages due diligence on your team?

- What does your buyer list typically look like for a business like mine?

- Can you provide client references for similar deals?

Advisors without a demonstrated track record in your deal size range are effectively learning on your transaction — and you'll absorb the cost of that education in both time and valuation.

Understanding Fee Structures

Retainer-Plus-Success-Fee: 81% of middle-market advisors in North America charge an upfront engagement fee or retainer, with 56% deducting collected fees from the final success fee. Retainers signal commitment from both parties and filter for serious sellers.

Success-Fee-Only: Advisors working on pure success fees face dangerous incentives—having invested months of unpaid work, they may pressure sellers to accept suboptimal offers just to collect fees. Retainer-backed advisors can afford to remain objective and hold out for premium valuations.

Typical Success Fee Ranges:

| Deal Size Tier | Typical Success Fee Percentage |

|---|---|

| $5M – $10M | 4% – 6% |

| $20M – $50M | 2% – 4% |

| $100M – $150M | 1% – 2% |

Success fees scale inversely with deal size, reflecting the baseline effort required to execute institutional-grade transactions. At the $50M revenue level (typically $25M–$75M enterprise value), expect fees in the 2.5%–4% range plus monthly retainer.

Indian ₹400 Crore Mid-Market Exit Landscape (2026)

Fast exits for Indian ₹200 to ₹1,000 crore revenue businesses cluster in three exit paths:

PE and strategic sell-side exit (most common): timeline 12 to 18 months from decision to closing. Typical valuation range: 8 to 15x EBITDA for stable industrials and consumer; 4 to 8x revenue for high-growth technology and deeptech; 20 to 30x EBITDA for high-quality specialty chemicals and consumer brands. PE dry powder available in India (~$50 billion per Bain-IVCA 2025) provides consistent competitive tension. Advisors serving this segment: Avendus Capital (consumer, tech, healthcare mandates), Kotak Mahindra Capital and ICICI Securities (large-cap and mid-market with integrated ECM), Axis Capital and JM Financial (mid-market execution), and Transjovan Capital for Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian corridor deals.

Strategic Indo-X cross-border exit: timeline 12 to 24 months. Foreign strategic acquirers pay premium multiples for market entry, brand equity, or IP acquisition. Structure typically involves FEMA-compliant share purchase or Section 47(vii) tax-neutral share swap if acquirer offers stock. Cross-border DD adds regulatory tail (US CFIUS for tech targets, EU merger control for large deals, Japanese FEFTA for foreign investment).

IPO with post-listing block sale: timeline 18 to 30 months (longer given SEBI ICDR requirements). Suitable for larger ₹800 crore+ revenue businesses. Founders retain equity through IPO, then exit via post-IPO block sales subject to SEBI (LODR) and SEBI (Insider Trading) restrictions.

Pre-exit corporate development readiness is where Indian mid-market promoters often lose value. Key checklist: (1) Companies Act cap-table clean-up: Section 62 preferential allotments, ESOP compliance, Section 179 share transfer restrictions in AoA; (2) Section 56(2)(x) exposure remediation: past ESOP grants and secondary sales below Rule 11UA fair value trigger deemed-gift tax; (3) FEMA compliance for prior foreign investment: Form FC-GPR, Form FC-TRS filings; (4) Financial statements: converted to Ind AS if not already, with related-party transactions disclosed and cleaned up; (5) Tax compliance: TDS on past transfers, GST compliance, transfer-pricing documentation.

Focus sectors within Transjovan's coverage most active in ₹400 crore mid-market exits include industrials, manufacturing, engineering, automotive, chemicals, packaging, F&B, agrochemicals, and building materials for Indo-Japan and Indo-German corridors; AI infrastructure, deeptech, and electronics for Indo-US corridor; specialty chemicals for Indo-European corridors.

Frequently Asked Questions

What is an M&A advisory firm and what services do they provide?

M&A advisory firms are professional intermediaries who guide business owners through mergers, acquisitions, and sales—covering valuation, buyer outreach, negotiation, due diligence management, deal structuring, and close coordination. Full-service advisors (versus brokers) provide strategic guidance throughout the entire transaction, not just buyer introductions.

What exit options do M&A advisory firms provide for companies at $50M revenue?

Primary options at this revenue level include:

- Full strategic sale (100% to a corporate buyer)

- PE platform or add-on acquisition, often with equity rollover

- Partial recapitalization — minority or majority stake sale while retaining control

- Cross-border transaction with an international acquirer

- Management buyout

The right structure depends on your liquidity goals, desired continued involvement, and timeline.

How long does a fast exit typically take for a $50M revenue business?

A well-prepared, advisor-led process can close in 6–9 months versus the industry average of 12–18 months. Speed depends primarily on pre-market preparation (clean financials, ready data room, clear growth story) and running a structured competitive process with multiple qualified buyers simultaneously.

What valuation multiple can a $50M revenue business expect in today's M&A market?

Valuation multiples are applied to EBITDA (not revenue) and vary significantly by sector and growth profile. Businesses in the $50M–$100M enterprise value range average 8.3x to 10.7x EBITDA, with healthcare commanding 10.2x and manufacturing at 5.3x. Businesses with above-average financial performance, low customer concentration, and clear growth drivers command premium multiples. PE buyers currently pay approximately 12.8x versus 9.9x for strategic corporate buyers.

How do I know if my business is ready for a fast exit?

Key readiness signals include:

- Three or more years of clean, reviewed financial statements

- A management team that operates independently of the founder

- No single customer above 10–15% of revenue

- Documented business processes and SOPs

- A clear EBITDA story with normalized earnings

An experienced M&A advisor can assess readiness and identify gaps before you go to market, avoiding costly delays during diligence.

What is the typical valuation range for a ₹400 crore revenue Indian mid-market company in 2026?

Valuation ranges vary widely by sector, growth rate, and profitability profile. Broad 2026 benchmarks for ₹400 crore revenue Indian mid-market: stable industrials, engineering, automotive components: 8 to 12x EBITDA. Specialty chemicals and agrochemicals: 12 to 18x EBITDA (premium for regulated products with formulation IP). F&B and consumer brands: 15 to 25x EBITDA with premium for D2C brand equity. Technology and SaaS: 4 to 8x forward revenue for growing companies, 10 to 15x for high-quality AI infrastructure and deeptech. Financial services: 2 to 4x P/BV for NBFCs, 15 to 25x P/E for high-growth insurance and payments. Energy transition (renewable IPPs, EV components): project-IRR-based for asset-heavy, 8 to 15x EBITDA for operating businesses. Cross-border Indo-X exits typically pay a 10 to 20% premium over domestic strategic buyers for market-entry equity.

What Section 47 tax structuring options exist for a fast Indian mid-market exit?

Section 47 of the Income Tax Act provides tax-neutrality for qualifying share swaps and mergers, which is materially valuable for Indian promoters preferring stock over cash consideration. Applicable sub-sections: Section 47(vii) exempts allotment of shares to shareholders of the amalgamating company in consideration of an amalgamation (statutory merger under Companies Act Sections 230 to 232 requiring NCLT approval, with the resulting company being an Indian company); Section 47(vic) covers demergers; Section 47(vi) covers cross-border share swaps with restrictions. For a fast mid-market exit where the acquirer is an Indian listed entity offering stock consideration, Section 47(vii) enables the Indian promoter to defer capital gains tax at the point of exit, receiving listed shares that can be sold post-lock-in. Alternative structures: Section 50B slump sale for a lump-sum consideration transfer treated as capital gains based on net worth methodology; Section 47(via) for cross-border reorganizations (subject to specific conditions). GAAR (General Anti-Avoidance Rules) requires commercial-substance justification.

Which Indian M&A advisor is best for a ₹400 crore mid-market fast exit?

For Indian ₹200 to ₹1,000 crore mid-market fast exits, best-fit advisors vary by sector and corridor. Consumer, D2C, technology, and healthcare exits: Avendus Capital leads with landmark PE and VC exit track record. Industrial, chemicals, semiconductors, and manufacturing Indo-X exits: Transjovan Capital serves mid-market Indian promoters with CDaaS support across Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridors and 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials). Large mid-market Indian domestic sell-side with integrated ECM: Kotak Mahindra Capital, ICICI Securities, Axis Capital. Structured deals with debt-linked exits: JM Financial. Partner-led execution, sector track record with the acquirer universe, and regulatory fluency (Section 47 planning, Rule 11UA valuation, FEMA compliance) matter more than league-table position at this deal size.