Yet here's the costly truth — most technology leadership teams think about exits far too late. A well-executed M&A exit strategy, planned years in advance, can mean the difference between accepting a reasonable outcome and securing a transformative one. When founders wait until investor pressure mounts or cash reserves dwindle, they surrender negotiating leverage and leave millions on the table.

This guide covers what growth-stage technology companies need to know: how to select the right exit route, what makes a tech company attractive to acquirers, the preparation steps that maximize valuation, how M&A pricing actually works, and how to avoid the most common and costly mistakes that kill deals or erode value.

TL;DR:

- M&A accounts for the vast majority of VC-backed tech exits, with strategic and PE buyers paying premiums for capabilities they can't build quickly

- Exit preparation should begin 12–24 months before engagement, focusing on financial cleanup, IP verification, revenue quality, and management depth

- SaaS companies meeting Rule of 40 command 121% valuation premiums over peers

- Deal structure matters as much as headline price — earn-outs, escrows, and reps & warranties significantly affect what founders actually receive

- Running a competitive buyer process is critical; single-buyer negotiations routinely result in 20–30% lower effective valuations

Why M&A Dominates Technology Company Exits

M&A has become the primary exit mechanism for growth-stage technology companies because it delivers speed, certainty, and full liquidity in ways that IPOs cannot. Going public requires massive regulatory infrastructure, quarterly earnings pressure, and ongoing compliance costs that distract leadership teams from running the business. IPO windows are cyclical and timing risk is real — market volatility can close exit opportunities for years.

By contrast, strategic acquisitions and PE buyouts offer relative speed and certainty. In 2025, global technology deal values rose 50%, with technology representing 84% of deal volumes and 76% of deal values. Trade sales typically close within 6–12 months and provide founders with full liquidity at signing (minus any earn-out or escrow provisions). PE buyouts can offer partial liquidity while accelerating growth with leverage and operational support.

The current macro environment strongly favors tech M&A activity. Global private equity dry powder reached $2.59 trillion in 2023, with more than 40% of capital from 2022–23 vintages still awaiting deployment.

Strategic acquirers — especially US, European, and Japanese corporates — are using acquisitions to secure AI capabilities, digital transformation infrastructure, and geographic market access they cannot build fast enough in-house.

That demand for geographic market access is precisely why cross-border M&A exits have accelerated for Indian and emerging-market tech companies. Recent transactions illustrate the trend:

- TCS acquired Coastal Cloud for approximately $700 million to deepen Salesforce implementation capabilities in North America

- Coforge acquired Encora for roughly $2.4 billion, expanding its digital engineering footprint across the US and Latin America

These deals reflect a structural shift: global acquirers are no longer just buying revenue — they are buying teams, capabilities, and market positions. For growth tech companies planning an exit, that dynamic makes cross-border M&A access and multi-geography deal expertise a material factor in maximizing outcome.

Technology M&A Exit Routes: Trade Sale, PE Buyout, or IPO?

Founders should understand all three primary exit paths early and avoid committing to one route prematurely. Market conditions, business maturity, revenue quality, and acquirer appetite will ultimately determine which route is viable when the exit window opens. Flexibility requires preparation across multiple scenarios.

Strategic Acquisition (Trade Sale)

A strategic sale works like this: a competitor, adjacent player, or large corporate acquires your technology company for its intellectual property, customer base, talent pool, or technology capabilities. This is the most common exit route for growth tech companies and typically delivers the fastest path to full liquidity.

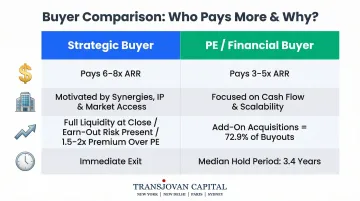

Strategic buyers pay for synergies. If your technology fills a critical capability gap, eliminates a competitor, or accelerates their entry into a new market, they will pay above-market multiples. On comparable SaaS deals, the difference is material:

- Strategic buyers: 6–8x ARR (typically 1.5–2.0x more than financial buyers)

- PE buyers: 3–5x ARR, focused on cash flow predictability over synergy value

Many strategic acquirers structure deals with deferred consideration tied to post-close milestones. Earn-out clauses mean founders must often remain actively involved for 1–3 years to realize the full deal value. Earn-outs can inflate headline valuations, but they expose founders to real risks:

- Integration disruption and management changes post-close

- Shifting corporate priorities that render milestones unachievable

- Headline valuation that overstates guaranteed cash proceeds

Evaluate earn-out terms with the same scrutiny as headline price. They are contingent, not certain.

Private Equity Buyout or Secondary Sale

A PE buyout involves a financial sponsor acquiring a majority or significant stake, often providing founders with partial liquidity while using leverage to accelerate growth for a subsequent exit. PE firms focus on predictable cash flows, scalable business models, and operational efficiency. Strategic synergies are secondary to financial engineering and margin expansion.

Add-on acquisitions now dominate PE activity — in 2025, they represented 72.9% of all buyouts, holding steady with the five-year average. PE firms acquire platform companies and bolt on complementary businesses to build revenue scale, expand capabilities, and reduce concentration risk. If your tech company fits the add-on profile for an existing PE portfolio company, expect multiple bidders and a competitive process.

A secondary sale occurs when one PE investor sells to another PE firm. This route makes strategic sense when a company has matured under PE ownership but needs additional capital and operational support to reach the next growth stage. India recorded 1,506 private-equity deals worth USD 37 billion in 2025 alongside its M&A activity, widening the secondary and sponsor-to-sponsor exit routes available to founders.

IPO

The IPO route offers access to public capital markets, public market visibility, and liquid currency for future acquisitions. The trade-offs are significant, though. Going public introduces:

- Quarterly earnings pressure and continuous analyst scrutiny

- Regulatory compliance burden and ongoing public reporting costs

- Governance requirements — independent board composition, audit committee oversight, and financial reporting rigor that most growth-stage companies are not yet equipped to meet

IPO windows are also cyclical. Market downturns can close public markets for extended periods, leaving late-stage companies without a liquidity path. Timing risk is real and often underestimated by founders focused on valuation upside.

For most mid-market technology companies generating $50M–$200M in revenue, M&A exits deliver better risk-adjusted outcomes than pursuing an IPO.

What Makes a Technology Company an Attractive Acquisition Target

The most successful exits happen when founders map their likely buyer universe early and build the business around what those specific acquirers value most. The priorities diverge sharply depending on whether you are targeting strategic buyers or financial buyers.

Strategic buyers want:

- Proprietary IP and defensible technology

- Access to new customer segments or geographies

- Talent and technical expertise

- Product adjacency that complements their existing portfolio

Financial buyers (PE firms) want:

- Predictable, recurring cash flows

- Scalable business models with operational efficiency

- Revenue growth potential with manageable risk

- Strong management teams that can execute post-acquisition

Proprietary Technology and Defensible IP

Proprietary technology and defensible IP directly increase acquisition valuations. Acquirers assess "build vs. buy" decisions rigorously — if replicating your capability would take 3–5 years and substantial capital, they will pay a premium to acquire it instead.

Ensure all IP is cleanly assigned to the company entity. Broken chains of title (where ownership rights are incomplete or disputed — a founder inventor who never formally assigned rights, or a university partner who retains unexpected claims) can surface as post-acquisition liabilities.

Unresolved IP disputes or unclear ownership structures routinely reduce EBITDA multiples by 20–30%. This is one of the most common and most preventable valuation leaks in tech transactions.

Revenue Quality Signals

Acquirers scrutinize revenue quality through specific metrics:

- Consistent ARR/MRR growth above 30% year-over-year signals genuine market demand

- NRR above 120% commands a 63% valuation premium over the median — expansion revenue is valued higher than new logo growth

- No single customer should exceed 10–15% of revenue; high concentration triggers escrows, earnouts, and valuation haircuts

- Long cohort lifetimes and low churn validate product-market fit in ways that top-line growth alone cannot

SaaS and subscription-based models command higher multiples due to revenue predictability. In 2024, SaaS firms were valued 21% higher than their non-SaaS peers, with median revenue multiples for private SaaS firms at 4.1x compared to 2.6x for all software deals.

Management Team Depth

Acquirers discount valuations heavily when key-person risk is concentrated. If the founder holds all critical client relationships, owns all technical knowledge, or is the sole driver of sales, the business is not institutionalized. Buyers fear that value walks out the door if the founder leaves.

Build a second tier of management at least 2–3 years before exit:

- A VP of Sales who owns customer relationships independently

- A CTO who manages technical architecture without founder input

- A CFO who runs financial operations and can field buyer due diligence directly

A business that runs without founder dependency closes faster and at better terms — buyers price execution risk into every deal structure.

Scalable Operations and Clean Data Infrastructure

Buyers pay less to integrate companies that have already built operational infrastructure. Tech companies with ERP, CRM, and financial reporting systems in place reduce integration cost and timeline — which translates directly into deal terms.

Clean data infrastructure means:

- Automated revenue recognition processes

- Real-time financial dashboards with KPI tracking

- CRM with documented customer history and pipeline

- Documented processes and playbooks across sales, marketing, and customer success

In competitive processes, buyers routinely offer 0.5–1.0x higher revenue multiples for targets that can demonstrate Day 1 integration readiness — the operational work done pre-exit pays for itself.

Preparing for a Tech M&A Exit: 12–24 Months Before Market

Exit preparation should begin at least 12–24 months before engaging with potential buyers. The goal is to eliminate discovery risk — anything a buyer finds during due diligence that they did not expect will erode value or kill the deal. Adopt a "diligence readiness" mindset across finance, legal, and operations.

Financial Preparation

Financial preparation is the most scrutinised element of due diligence. Buyers judge the quality of the finance function as a proxy for the quality of the business overall.

Requirements:

- Three years of clean, audited (or audit-ready) financial statements

- Documented revenue recognition policy consistent with ASC 606 or IFRS 15

- Up-to-date management accounts with monthly close processes

- KPI dashboard tracking ARR, MRR, churn, NRR, CAC, LTV, and gross margins

- Detailed financial model with realistic projections (3-year forward)

Avoid aggressive revenue recognition, deferred revenue misclassification, or expense capitalisation that inflates profitability. Buyers will normalise financials during diligence, and any discrepancies destroy trust and compress valuations.

Legal and Governance Readiness

Legal surprises rarely kill deals outright. More often, they surface mid-process, stall negotiations, and generate legal costs that erode proceeds for both sides. Address these items 12+ months before engaging buyers:

- IP assignments verified — ensure all founders, employees, and contractors have signed IP assignment agreements

- Customer and supplier contracts reviewed — identify change-of-control clauses that require consent or trigger renegotiation

- Data privacy compliance — document GDPR compliance (for European customers), India's DPDP Act compliance (phased implementation through May 2027), or equivalent regulations

- Board minutes current — ensure all board resolutions, equity grants, and major decisions are properly documented

- Cap table clean — verify all option grants are properly recorded, vesting schedules are accurate, and there are no outstanding disputes

India's Digital Personal Data Protection Act (DPDP Act) requires companies to document cross-border data transfers and carries penalties of up to ₹250 crore for non-compliance. Ensure your data processing and transfer policies are documented and compliant before due diligence begins.

The Virtual Data Room

Maintain a live, organised virtual data room at all times rather than assembling one reactively under deal pressure. A well-organised data room signals operational maturity and can cut several weeks off the due diligence timeline.

Data room structure should include:

- Corporate documents (articles, bylaws, cap table, board minutes)

- Financial statements (3 years audited, management accounts, projections)

- Contracts (customer agreements, supplier contracts, partnership agreements)

- IP documentation (patents, trademarks, assignment agreements)

- HR and employment (org chart, key employee contracts, equity plans)

- Compliance (privacy policies, security certifications, regulatory filings)

Working with an M&A Advisor

Bring in a dedicated M&A advisor 12–24 months before taking your company to market. Advisors with deep sector expertise can help position your exit narrative, identify the right buyer universe, and run a competitive process that maximises valuation.

Transjovan Capital — with specialised expertise in IT Services, Enterprise SaaS, and Deeptech, and access to strategic acquirers across the US, Europe, India, and APAC — supports growth tech companies through structured exit preparation. Its Corporate Development as a Service (CDaaS) model embeds exit readiness directly into the business, so companies reach the market prepared rather than reactive.

Valuation Drivers in Technology M&A: What Acquirers Actually Pay For

Understanding how acquirers price technology companies is essential for setting realistic exit expectations and negotiating effectively. Valuation frameworks differ by business model, growth stage, and buyer type.

Primary Valuation Frameworks

For SaaS businesses:

- EV/ARR multiples — the most common metric for SaaS valuations. Between 2015 and 2026, the median SaaS company was valued at 4.5x EV/Revenue, with top quartile companies achieving 8.1x or higher.

- Rule of 40 — calculated as Revenue Growth Rate (%) + EBITDA Margin (%). Companies meeting Rule of 40 get a 121% valuation premium over those that don't. Acquirers use this metric to assess whether a SaaS business warrants premium pricing.

For IT Services companies:

- EV/EBITDA multiples — over the past decade, median transaction multiples for IT services companies have averaged 1.4x Revenue and 11.0x EBITDA.

For high-growth, pre-profitability tech:

- Blended growth-adjusted multiples — acquirers weight revenue growth more heavily than profitability, typically applying a 2x weighting to growth versus margin contribution.

Before entering negotiations, benchmark your company against current comparable multiples in your specific sub-sector — vertical SaaS, IT services, and fintech each trade at materially different ranges.

Strategic Premium

When a tech company fills a critical gap for an acquirer — entering a new geography, eliminating a competitor, or delivering a capability that would take years to build — buyers pay above-market multiples. This is called strategic premium. Strategic acquirers pay an average premium of 46.4% above recent trading value in competitive auctions, compared to 36.5% when financial buyers win.

Capturing that premium requires identifying and cultivating "motivated acquirers" well before a formal process begins. Motivated acquirers typically share one or more of these characteristics:

- Publicly committed to investing in your technology category

- Recently acquired a direct competitor, signalling active consolidation intent

- Facing an existential competitive threat that your capability would neutralise

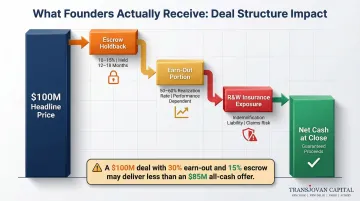

Deal Structure's Impact on Effective Valuation

Headline price is not what founders receive. Deal structure directly affects what founders actually receive:

- Escrows — typically 10–15% of purchase price held for 12–18 months to cover indemnification claims

- Earn-outs — deferred consideration tied to post-close revenue or EBITDA milestones; only 50–60% of earn-outs are fully realized

- Representations and warranties — founders remain liable for breaches; uncapped R&W exposure can create unlimited downside

- Locked-box vs. completion accounts — locked-box mechanisms fix valuation at a historical date; completion accounts adjust for working capital changes between signing and closing

Founders who focus only on headline price often leave money behind. A $100M deal with 30% earn-out, 15% escrow, and broad R&W exposure may deliver less cash at close than an $85M all-cash offer with capped indemnities. Negotiating structure is as important as negotiating price.

Common Pitfalls in Tech M&A Exits — and How to Avoid Them

Pitfall 1: Starting Too Late and Triggering a Distressed Sale

Founders who only begin exit preparation when they face a cash crisis or investor pressure operate under compressed timelines, limited buyer competition, and reduced valuations. Distressed sellers accept the first reasonable offer because they have no time to wait for better ones.

Build exit readiness as a continuous business discipline — not a one-time sprint before a sale. Maintain clean financials, organized legal documentation, and operational metrics year-round. When market conditions turn favorable, you can engage buyers from a position of strength rather than necessity.

Pitfall 2: Negotiating with a Single Buyer Without Running a Competitive Process

Exclusivity with one potential acquirer eliminates negotiating leverage and routinely results in lost deal value. Single-buyer processes may close faster, but they consistently yield lower valuations than competitive auctions — speed rarely compensates for the premium left on the table.

Run a structured process with multiple qualified buyers simultaneously. Even if you have a preferred acquirer, bringing additional parties to the table:

- Creates genuine urgency that prevents lowball offers

- Validates your valuation through independent buyer interest

- Gives you negotiating leverage on both price and terms

Pitfall 3: Overfocusing on Headline Valuation While Ignoring Deal Structure

Earn-out risk, escrow holdbacks, representations and warranties exposure, and post-close restrictive covenants can reduce the effective value of a deal significantly below the announced price.

The announced price is rarely what founders actually receive. Evaluate total deal economics by modelling these scenarios before signing:

- What do you receive at close (net of escrows)?

- What conditions must be met to receive earn-out payments?

- What is your exposure under R&W provisions?

- What non-compete and employment restrictions apply post-close?

Negotiate aggressively on terms — escrow size, earn-out structure, indemnity caps, and survival periods — not just headline price.

Indian Technology M&A Exit Landscape (2026)

Technology exits in India span four distinct exit paths:

- Indo-US corridor sales to strategic acquirers: Indian SaaS, deeptech, and AI infrastructure companies sold to US strategic buyers. Requires FEMA valuation certification, DTAA benefit optimization (India-US, India-Netherlands, or India-Mauritius routes), and Section 47 planning if consideration includes acquirer stock.

- Domestic strategic exits: Indian technology companies acquired by larger Indian tech or diversified groups. The L&T-Mindtree merger at ~₹8,400 crore is the landmark domestic tech consolidation example, executed as a scheme of arrangement under Companies Act Section 230.

- PE and secondary buyouts: control acquisitions by financial sponsors, with tax planning around Section 50B slump sale, capital gains, and MAT (Minimum Alternate Tax) implications.

- IPO plus block deals: partial exit via public listing, followed by secondary block deals by pre-IPO PE and founder shareholders. SEBI (ICDR) and SEBI (LODR) frameworks apply.

Regulatory instruments include SEBI (SAST) Regulations 2011, Companies Act Sections 230 to 232, FEMA (for cross-border sales and DTAA optimization), Rule 11UA valuation for Section 56(2)(x), Section 50B (slump sale), Section 47(vii) (tax-neutral share swaps in schemes), Section 5 of the Income Tax Act (residence-based taxation for founders), GAAR provisions (for aggressive structures), and specific SEBI (Insider Trading) considerations for pre-announcement periods.

Focus sectors within Transjovan's coverage particularly relevant to technology exits include AI infrastructure, deeptech, electronics, and semiconductors. Cross-border corridors most active in tech exits include Indo-US (SaaS, deeptech), Indo-European (industrial tech, deeptech), and Indo-Japan (deeptech and semiconductors).

Frequently Asked Questions

What is the best exit strategy for a technology company?

The "best" strategy depends on your company's growth stage, revenue quality, founder objectives, and market conditions. M&A (trade sale or PE buyout) is the most common route, delivering speed and certainty. IPO is reserved for highly scaled, governance-ready companies with sustained profitability and public market appetite.

When should a tech founder start planning their M&A exit strategy?

Exit planning should begin from the company's earliest stages — ideally at first fundraise when you select investors and structure the cap table. The detailed preparation phase (financial cleanup, legal readiness, management team development) should begin at least 12–24 months before engaging buyers to maximize valuation and reduce execution risk.

What valuation multiples apply to technology companies in M&A?

SaaS businesses are typically valued on EV/ARR multiples (3–8x depending on growth rate and NRR), while IT services companies use EV/EBITDA (averaging 11.0x). The Rule of 40 is a widely used benchmark — companies meeting this threshold command significant valuation premiums.

What is the difference between a strategic buyer and a financial buyer in tech M&A?

Strategic buyers (corporates, competitors) pay for synergies and often pay premiums to eliminate competition, acquire capabilities, or enter new markets. Financial buyers (PE firms) focus on cash flow potential and scalability, typically using leverage and planning for a subsequent exit within 3–7 years.

What are the most common reasons tech M&A deals fail or fall through?

The top causes include due diligence discoveries (legal, financial, or IP surprises), valuation misalignment, key-person dependency concerns, and cultural or integration incompatibility. Even technically sound deals fail at execution — post-merger value erosion is most often a people and culture problem, not a financial one.

How long does a typical tech M&A exit process take from start to close?

A well-run technology M&A process typically takes 6–12 months from initial buyer outreach to close, with due diligence and legal documentation accounting for the largest share of time. Companies in a state of diligence readiness can compress this timeline; unprepared sellers face extended timelines and higher deal failure risk.

How does Section 47 tax neutrality apply to Indian technology M&A exits?

Section 47 of the Income Tax Act 1961 exempts qualifying transfers from capital gains tax when the transaction is structured as a share swap or statutory merger. Sub-sections most relevant to Indian technology exits include Section 47(vii), which exempts allotment of shares to shareholders of the amalgamating company in consideration of the merger, and Section 47(vic) for demergers. This enables tax-deferred exits when Indian technology founders receive stock of the acquiring company (particularly common in Indo-US strategic sales where the US acquirer offers stock consideration). Restrictions include: at least 75% of shareholders (in value) of the amalgamating company must become shareholders of the amalgamated company; the resulting entity must be an Indian company for Section 47(vi). Cross-border Indo-US share swaps often use qualifying structures under Sections 47 read with Section 5 of the Income Tax Act.

What FEMA rules apply to Indian technology company sales to foreign buyers?

When a non-resident acquires shares of an Indian technology company (partial or full acquisition), FEMA requires: (1) valuation certification by a SEBI-registered Merchant Banker or Chartered Accountant using internationally accepted methodology (typically DCF or Comparable Companies for tech), (2) Form FC-TRS filing within 60 days for share transfers between residents and non-residents, and (3) compliance with FDI sectoral cap (100% automatic-route for most technology sub-sectors, subject to specific carve-outs). For outbound Indian technology sales where an Indian founder sells to a foreign acquirer, additional considerations include RBI reporting for the founder receiving foreign consideration and potential FEMA implications for keeping proceeds abroad under the Liberalised Remittance Scheme (LRS) or Overseas Direct Investment (ODI) frameworks.

Which Indian M&A advisor is best for a technology exit in the ₹500 to ₹2,000 crore range?

For Indian technology exits in the ₹500 to ₹2,000 crore range, best-fit advisors span three categories. Avendus Capital (majority-owned by KKR) leads the Indian technology sector boutique category with landmark exits across SaaS, deeptech, healthcare tech, and consumer tech. Domestic full-service banks Kotak Mahindra Capital and ICICI Securities cover larger tech mandates with integrated ECM support for pre-IPO founders. For Indo-US or Indo-European technology cross-border sales with CDaaS support, Transjovan Capital serves Indian technology promoters across 16 focus sectors including AI infrastructure and deeptech (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials). Partner-led execution, Indian tech exit track record, and Indo-X corridor fluency matter more than league-table position at this deal size.