Introduction

Cross-border M&A deals rarely collapse because of flawed strategy. They collapse because acquirers underestimate legal complexity. Indian M&A reached roughly ₹5 lakh crore (USD 60.2 billion) across 963 deals in 2025, with value up 36% year-over-year. Globally, cross-border transactions accounted for approximately 34% of global deal numbers in 2025, representing roughly $950 billion in value, yet more of those deals are hitting regulatory walls than ever before. Cross-border M&A legal complexity for Indian companies runs across two regulatory geographies simultaneously. Indian side: SEBI SAST for listed targets, Companies Act 2013 Sections 230 to 232, IBC for stressed assets, FEMA and Consolidated FDI Policy, CCI merger notification, and Income Tax Sections 47 and 50B. Target-market side: US CFIUS review for tech and critical infrastructure, EU merger control for large transactions, UK CMA for competition, Japanese FEFTA for foreign investment, Australian FIRB, and DTAA optimization for withholding tax. Managing this dual-jurisdiction stack is where cross-border deals succeed or stall.

Antitrust authorities now levy record fines for pre-closing coordination violations. Foreign direct investment (FDI) screening has expanded to capture sensitive personal data. OECD Pillar Two has fundamentally rewritten deal modeling assumptions. Divergent governance norms and multi-jurisdictional tax traps compound the exposure at every stage.

This article gives corporate development leaders and C-suite executives a practical framework for navigating that complexity—covering regulatory strategy, jurisdiction-specific due diligence, deal structuring choices, and integration sequencing that holds up across multiple legal systems.

Key Takeaways

- Cross-border M&A legal complexity cuts across regulatory approvals, FDI/national security reviews, antitrust filings, tax structuring, IP, and multi-jurisdiction governance — simultaneously

- Map your regulatory strategy by jurisdiction before signing — it is the single most decisive success factor in cross-border deals

- Domestic due diligence standards fail in cross-border deals; FCPA compliance, sanctions screening, and local labor law each require jurisdiction-specific investigation protocols

- Transaction structure choices (asset vs. share acquisition, holding entity jurisdiction, consideration type) create cascading legal and tax consequences

- Governance and cultural differences are consistently underestimated legal risks — board consent processes, fiduciary duties, and shareholder thresholds vary sharply across markets

What Makes Cross-Border M&A Legally Complex

Cross-border M&A occurs when a company in one country acquires, merges with, or invests in a company in another country. Despite geopolitical tensions, cross-border transactions remained resilient in 2025, accounting for 36% of global M&A value.

Core Layers of Legal Complexity

Cross-border deals face fundamentally different legal challenges than domestic transactions:

- Multi-jurisdictional regulatory regimes: Antitrust authorities, FDI screening bodies, and sector-specific regulators operate with conflicting thresholds, timelines, and approval standards across the acquiror's home jurisdiction, the target's jurisdiction, and any third-country holding structure.

- Corporate governance mismatches: Fiduciary duty standards, works council consultation obligations, mandatory bid thresholds, and shareholder approval processes vary dramatically — what's routine in one jurisdiction may be prohibited in another.

- Tax and FDI structure risk: Withholding taxes, capital gains treatment, transfer pricing, bilateral tax treaties, and anti-inversion rules all require careful modeling before signing. A misstep here directly erodes post-merger returns.

- Extraterritorial compliance exposure: The FCPA applies to US-listed acquirors and their subsidiaries worldwide. OFAC sanctions require supply chain screening. GDPR and similar privacy regimes govern how personal data moves across borders during due diligence and integration.

Build Your Multi-Jurisdictional Regulatory Strategy Early

Regulatory planning must begin at deal origination, not after a term sheet is signed. Political, antitrust, and foreign investment screening risks need mapping against the target's industry, geography, and ownership structure well before public announcement.

Understand Which Regulatory Bodies Have Jurisdiction

Cross-border deals trigger multiple concurrent approval processes with different thresholds and waiting periods:

- HSR Act (US) — 2026 transaction threshold: $133.9 million. Initial waiting period: 30 days (15 for cash tender offers); a Second Request adds 30 days after compliance.

- EU Merger Regulation — Triggered when combined worldwide turnover exceeds €5 billion and EU-wide turnover for at least two firms exceeds €250 million. Phase I: 25 working days; Phase II: up to 90 working days.

- Competition Commission of India (CCI) — Deal Value Threshold of ₹2,000 crore applies when the target has "substantial business operations in India." Overall review spans 150 days, with a 30-day prima facie opinion period.

Deal Structuring Tip: Identify the "long pole in the tent" early — often a CFIUS investigation or EUMR Phase II review — and align drop-dead dates in the purchase agreement accordingly. Sequence filings to manage risk, not just satisfy compliance order.

Prioritize FDI Screening and National Security Reviews

Antitrust clearance is only part of the approval picture. FDI and national security screening has intensified across major jurisdictions — in 2024, CFIUS reviewed 116 declarations and 209 formal notices, launching investigations into 116 of those notices. The Committee concluded with mitigation agreements for 16 notices; two transactions were blocked via Presidential decision.

Three regimes demand close attention:

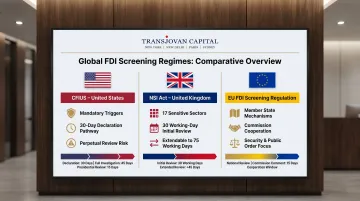

- CFIUS (US) — Mandatory notifications now apply to investments in critical technology, infrastructure, sensitive personal data, or by foreign government-linked entities. Deals that don't file remain subject to CFIUS review in perpetuity. Abbreviated declaration processes offer a 30-day assessment pathway to reduce uncertainty.

- UK National Security and Investment Act 2021 — Mandatory pre-completion notification in 17 sensitive sectors, including AI, defense, and data infrastructure. Initial review: 30 working days, extendable to 75.

- EU FDI Screening (Regulation 2019/452) — Requires Member States to operate national screening mechanisms and cooperate with the Commission on investments affecting security or public order.

Key Takeaway: Run a CFIUS/FDI risk assessment at the outset of any deal with a US or EU nexus. Allocate regulatory risk contractually — reverse break fees tied to non-approval are standard practice — and engage agencies proactively, potentially before public announcement.

Conduct Jurisdiction-Specific Due Diligence

Wholesale application of the acquiror's domestic due diligence checklist to a foreign target is one of the most common and costly mistakes in cross-border M&A. It causes friction, wastes time, misses local risks, and can cost the acquiror credibility in competitive processes.

Adapt Diligence Standards to Target Jurisdiction Norms

Due diligence scope and methodology must be calibrated to the target's legal regime and market norms. What constitutes reasonable inquiry, how data rooms are structured, what information can be legally shared before signing, and what requests are considered intrusive vary by jurisdiction.

Jurisdiction-specific priorities often underfocused in domestic deals include:

- Employee transfer obligations and works council consultation (Europe): Directive 2009/38/EC requires information and consultation of European Works Councils in transnational M&A. When structure changes significantly, existing EWCs must be adapted or renegotiated.

- Government concession or license terms (regulated industries in emerging markets): Sensitive sectors often have foreign ownership restrictions or require regulatory consent for control changes.

- Foreign ownership restrictions (sensitive sectors): Many countries limit foreign participation in telecommunications, defense, media, and financial services.

Firms like Transjovan Capital, with partner-led advisory teams and on-the-ground presence across the US, Europe, India, and APAC, bring jurisdiction-specific intelligence to due diligence—ensuring local legal risks are identified through advisors who understand both the letter and practice of law in each target market.

Focus on Anti-Bribery, Sanctions, and Data Privacy Compliance

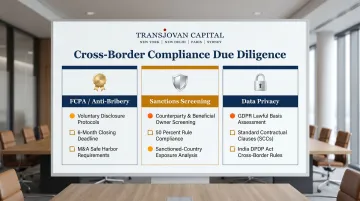

Foreign Corrupt Practices Act (FCPA): The FCPA applies extraterritorially to US-listed acquirors and their subsidiaries worldwide. Anti-corruption due diligence on targets with operations in high-risk jurisdictions is not optional. The DOJ's 2023 Corporate Enforcement Policy creates a presumption of declination for companies that voluntarily self-disclose misconduct, fully cooperate, and timely remediate.

The M&A Safe Harbor requires disclosure within six months of closing and remediation within one year to avoid successor liability.

Sanctions compliance: OFAC expects rigorous sanctions-related due diligence during M&A, particularly for non-US targets. Screening must cover:

- Counterparties, intermediaries, and beneficial owners (applying OFAC's 50 Percent Rule)

- Supply chains and jurisdictions of operation

- Targets with Russia, Belarus, Iran, or other sanctioned-country exposure

Data privacy: Sharing EU personal data in a virtual data room requires a lawful basis under GDPR Article 6, such as "legitimate interests." International transfers require adequacy decisions or Standard Contractual Clauses. India's Digital Personal Data Protection Act 2023 permits cross-border transfer except to countries restricted by government notification.

Data privacy has also become a CFIUS trigger. CFIUS ordered Beijing Kunlun to divest Grindr over national security concerns regarding foreign access to sensitive personal data of US citizens — a precedent that acquirors in any data-intensive sector should factor into their diligence framework.

Structure the Transaction for Legal and Tax Efficiency

Transaction structure in cross-border M&A is not a back-office decision. The choice of acquisition vehicle, form of consideration, governing law, and holding entity jurisdiction all have cascading legal, tax, and regulatory consequences that must be modeled before signing.

Choose the Right Acquisition Vehicle and Legal Form

The choice of legal form carries materially different risk profiles across jurisdictions:

- Asset acquisitions provide cleaner liability separation but may trigger consent obligations under local law

- Share acquisitions are simpler to execute but inherit contingent and hidden liabilities

- Mergers/schemes of arrangement offer court-approved deal certainty — particularly in the UK, Ireland, and certain Commonwealth jurisdictions

Acquirors should select jurisdiction and corporate form based on tax treaty access, FDI regulatory requirements, and practical ability to enforce contractual remedies in the target's country. That same jurisdictional choice then determines the tax exposure the deal inherits — which must be modeled before term sheets are signed.

Model Cross-Border Tax Exposure Before Signing

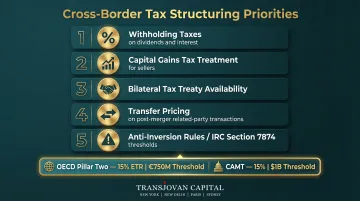

Cross-border tax structuring priorities include:

- Withholding taxes on dividends and interest

- Capital gains tax treatment for sellers

- Bilateral tax treaty availability (OECD Model Tax Convention Articles 10 and 11 govern withholding tax mitigation)

- Transfer pricing implications of post-merger related-party transactions

- Anti-inversion rules: IRC Section 7874 imposes penalties if US target shareholders hold 60–80%+ of the combined entity post-transaction. At 80%+ continuing ownership, the new foreign parent is treated as a domestic US corporation for all tax purposes, nullifying the inversion.

Two global minimum tax regimes add further complexity for large multinationals. OECD Pillar Two imposes a 15% global minimum Effective Tax Rate (ETR) for entities with €750 million+ consolidated global revenue. The US Corporate Alternative Minimum Tax (CAMT) applies a 15% minimum tax on Adjusted Financial Statement Income (AFSI) for corporations averaging $1 billion+ annually.

These "book income" overlays can inflate effective tax rates on acquisition financing structures that appeared efficient pre-Pillar Two — making holding company jurisdiction decisions far more consequential than they were five years ago.

Model multiple transaction structures — including holding company jurisdiction alternatives — against post-deal effective tax rate before signing. Engage tax counsel from both the target and acquiror jurisdictions simultaneously, not sequentially.

Manage Corporate Governance Differences and Plan Integration

Corporate governance norms differ substantially across jurisdictions—board composition, fiduciary duty standards, works council roles, mandatory bid thresholds, and shareholder approval requirements. Failing to understand these differences causes deal delays, litigation risk, and post-merger friction.

Navigate Governance Differences Proactively

United Kingdom: Rule 2.7/2.8 (PUSU) "put up or shut up" rules dictate firm intention announcements within strict timelines. Rule 21 passivity rules restrict target boards from taking frustrating actions (e.g., asset disposals) without shareholder approval.

India: Acquiring 25% or more of shares/voting rights triggers a mandatory open offer to public shareholders under SEBI regulations.

Ireland: A 42-day PUSU period is placed on bidders to make intentions publicly known.

Practical best practices:

- Research the target board's decision-making obligations under local law before approaching

- Plan communications to all stakeholder groups—employees, unions, regulators, communities—before public announcement

- Engage local public relations advisors early in politically sensitive transactions

Manage Integration as a Legal Risk

Post-merger integration carries its own set of legal compliance obligations — three in particular require structured attention from day one.

Gun-jumping is among the most costly risks. Premature integration before regulatory clearance exposes parties to antitrust liability. In January 2025, the FTC imposed a record $5.6 million civil penalty on XCL Resources, Verdun Oil, and EP Energy for unlawfully coordinating on pricing during the HSR waiting period. The European Commission fined Illumina €432 million for closing its GRAIL acquisition while an in-depth EC investigation was still ongoing.

Labor law obligations govern when and how headcount changes can occur across borders. Works council consultation requirements, employee transfer protections, and notice periods vary significantly by jurisdiction.

IP transfer and licensing arrangements require legal formalization in each jurisdiction to ensure enforceability and avoid tax exposure.

These compliance obligations directly influence whether integration delivers value. Recent 2024 research by Bain & Company shows nearly 70% of mergers now succeed in creating value — a marked improvement over the oft-cited 70% failure rate from earlier studies. Yet a 2023 Bain analysis found that 83% of practitioners in failed deals pointed to poor integration as the primary cause, specifically cultural misalignment and failure to retain key talent.

Transjovan Capital's CDaaS model embeds an experienced corporate development team directly into the client's organization, managing integration compliance obligations across jurisdictions on a continuous basis. This reduces the burden on CXO teams while keeping PMI governance and synergy tracking on track through each phase of the deal.

Indian Cross-Border M&A Legal Landscape (2026)

Cross-border M&A involving Indian buyers or sellers navigates a dual-jurisdiction regulatory stack:

Indian regulatory instruments: (1) SEBI (SAST) Regulations 2011 for listed-target acquisitions, (2) Companies Act 2013 Sections 230 to 232 for schemes of arrangement, (3) IBC 2016 for stressed-asset resolutions, (4) FEMA and Consolidated FDI Policy for cross-border share and asset transfers, (5) CCI merger notification (assets over ₹1,000 crore or turnover over ₹3,000 crore in India), (6) Income Tax Sections 47(vi), 47(vii), and 47(vic) for tax-neutral share swaps and demergers, (7) Section 50B for slump sale, (8) Section 56(2)(x) and Rule 11UA valuation for tax purposes, and (9) GAAR (General Anti-Avoidance Rules) for aggressive tax-motivated structures.

Target-market regulatory instruments for major corridors:

- Indo-US corridor: CFIUS (Committee on Foreign Investment in the US) review for critical technology, US state privacy laws, HSR Act pre-merger notification, and SEC filings for public-target acquisitions.

- Indo-European corridor (French, German, Italian, and broader European): EU merger regulation (EUMR) for combined turnover thresholds, national FDI screening (French SREN, German FDI Screening Act, Italian FDI regime), GDPR compliance, and EU AI Act for AI-target acquisitions.

- Indo-Japan corridor: FEFTA (Foreign Exchange and Foreign Trade Act) foreign-investment approval for designated business categories, Japanese Antimonopoly Act (JFTC) merger notification, and specific technology-transfer restrictions.

- Indo-Australian corridor: FIRB (Foreign Investment Review Board) approval thresholds, Australian Competition and Consumer Commission (ACCC) merger review, and critical-technology screening.

DTAA (Double Taxation Avoidance Agreement) considerations: India-US, India-UK, India-Netherlands, India-Mauritius, and India-Singapore treaties materially affect withholding tax on dividends, interest, royalty, and capital gains. Structuring choices (holding entity jurisdiction, hybrid instruments) leverage DTAA benefits within GAAR-safe boundaries.

Landmark 2019 to 2025 Indo-X deals like the ArcelorMittal-Nippon acquisition of Essar Steel, Hindalco acquisition of Aleris, and Adani acquisition of Ambuja and ACC all navigated this dual stack, typically requiring 6 to 18 months of parallel-processed regulatory approvals across both jurisdictions.

Frequently Asked Questions

What is cross-border M&A?

Cross-border M&A occurs when a company in one country acquires, merges with, or makes a significant investment in a company in another country. It requires simultaneous navigation of multiple legal systems, regulatory regimes, and governance frameworks.

What is cross-border structuring?

Cross-border structuring is the process of designing a transaction framework to optimise legal compliance, regulatory clearance likelihood, and tax efficiency across all relevant jurisdictions. This includes decisions on acquisition vehicle, deal form (asset vs. share, merger vs. tender offer), holding entity jurisdiction, and consideration type.

What is cross-border tax structuring?

Cross-border tax structuring involves designing a transaction to minimise aggregate tax exposure across all jurisdictions. Key considerations include withholding taxes, capital gains treatment, treaty access, anti-inversion rules, global minimum tax regimes, and the long-term tax profile of the combined entity.

What are the 4 types of M&A?

The four main types are horizontal (same industry, competing companies), vertical (buyer-supplier or supply chain relationships), conglomerate (unrelated industries), and market extension/product extension mergers. Each carries different antitrust risk profiles in cross-border contexts.

How do you manage regulatory risk in cross-border M&A?

Effective regulatory risk management starts with early identification of all applicable approvals — antitrust, FDI/CFIUS, and sector-specific regulators — followed by proactive agency engagement before or shortly after announcement. Contractual protections such as reverse break fees allocate risk between parties, while advisors with jurisdiction-specific knowledge keep the process on track.

Why is jurisdiction-specific due diligence critical in cross-border deals?

Domestic due diligence checklists miss jurisdiction-specific risks that can become material liabilities post-closing or derail regulatory approvals. These include local anti-bribery standards, works council requirements, government concession terms, sanctions exposure, and data privacy obligations.

How do Indian and US regulatory regimes intersect in Indo-US M&A?

For Indo-US cross-border M&A, both regimes apply concurrently. Indian side: FEMA reporting (Form FC-TRS for share transfers between residents and non-residents, Form ODI for outbound), Rule 11UA and Merchant Banker valuation certification, SEBI SAST for listed Indian targets, and Section 47 tax-neutrality planning. US side: CFIUS review is critical for acquisitions of US critical-technology, critical-infrastructure, or sensitive personal-data companies (mandatory declaration for TID US Businesses); HSR Act pre-merger notification if the transaction value exceeds thresholds (~$120M current, adjusted annually); SEC filings if the US target is public; and state-level privacy laws (CCPA, VCDPA, CTPA) affecting technology target DD. Sequencing typically runs Indian FEMA and CCI in parallel with US CFIUS and HSR, adding 90 to 180 days combined.

What role does DTAA play in cross-border M&A structuring for Indian companies?

Double Taxation Avoidance Agreements (DTAAs) between India and target-market jurisdictions materially affect withholding tax (WHT) on cross-border dividend, interest, royalty, and capital-gains flows. Key DTAAs relevant to Indo-X M&A: India-Mauritius (revised 2016) provides reduced WHT on qualifying investments and treaty benefits subject to Principal Purpose Test and Limitation on Benefits; India-Netherlands offers favorable WHT on dividend flows for holding-entity structures; India-Singapore provides low WHT on royalties and technical services fees; India-US DTAA provides 15% WHT on dividends and 15% on interest with careful GAAR compliance. Structuring choices (holding-entity jurisdiction, hybrid instruments, and equity vs debt-linked funding) leverage DTAA benefits, but GAAR (General Anti-Avoidance Rules) requires commercial-substance justification, not just tax motivation. Advisors serving Indo-X deals typically model 3 to 5 alternative structures for DTAA benefit optimization.

Which Indian M&A advisor handles cross-border legal complexity best?

For cross-border M&A with dual-jurisdiction legal complexity, best-fit advisors span three categories. Global bulge-brackets (Goldman Sachs, Morgan Stanley) handle mega-cap Indo-US and Indo-European deals requiring global distribution. Domestic full-service banks (Kotak Mahindra Capital, ICICI Securities, Axis Capital) partner with global bulge-brackets on such mandates. For Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridor deals with embedded CDaaS support across 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials), Transjovan Capital serves as the corridor-fluent advisor, coordinating dual-regime sequencing (Indian SEBI, FEMA, CCI plus target-market CFIUS, EU merger control, FEFTA, or FIRB). Partner-led execution, corridor track record, and cross-jurisdiction sequencing depth matter more than league-table position at this deal type.