Introduction

Enterprise SaaS M&A is moving faster than most corporate development teams can track. India's IT and ITeS M&A reached 96 deals worth USD 2,167 million in 2025, with values more than doubling from USD 1,049 million in 2024 as acquirers paid up for fewer, larger software assets. Globally, deal volumes hit an all-time high of 2,698 transactions in 2025, a 28% surge from 2024's 2,107 deals, as corporates and private equity firms accelerated their pursuit of high-growth software. For Indian enterprise SaaS founders and PE-backed technology companies, M&A operates inside a specific regulatory and tax pathway. FEMA valuation certification by a SEBI-registered Merchant Banker or Chartered Accountant applies for cross-border Indo-US and Indo-European exits. Section 47(vii) tax-neutrality enables tax-deferred share swaps when Indian promoters receive acquirer stock. Section 56(2)(x) and Rule 11UA shape secondary sales and ESOP grant valuations. DTAA (India-US, India-Netherlands, India-Singapore) materially affect withholding tax on cross-border consideration. DPDP Act 2023 and IT Act plus CERT-In reporting shape DD scope for data-heavy SaaS targets.

Global M&A deal value jumped 40% year-over-year to $4.9 trillion in 2025, with SaaS accounting for roughly 58% of total software M&A activity. For enterprises and investors, knowing which SaaS categories are growing fastest is no longer background research — it's core acquisition strategy.

When a competitor acquires a platform that locks in workflow or data advantages, the window to respond narrows quickly — especially in vertical SaaS, where the pool of high-quality targets is finite. This guide breaks down the fastest-growing enterprise SaaS categories, the acquisitions reshaping each one, and what the consolidation trends mean for buyers navigating the market now.

Key Takeaways

- Enterprise SaaS M&A reached 2,698 transactions in 2025 — up 28% year-over-year

- AI-native SaaS commands 1–3x valuation premiums over non-AI peers

- Private equity accounts for 58% of SaaS M&A volume, with Thoma Bravo and Main Capital among the most active acquirers

- Healthcare (18%) and financial services (14%) lead vertical SaaS deal activity

- Enterprises without a continuous corporate development function routinely lose access to the best acquisition targets

The Fastest Growing Enterprise SaaS Categories in M&A

The Fastest Growing Enterprise SaaS Categories in M&A

Not all SaaS segments attract equal acquisition interest. Certain categories—driven by defensibility, mission-criticality, and AI integration potential—are pulling disproportionate attention from both strategics and private equity.

AI-Native Enterprise SaaS

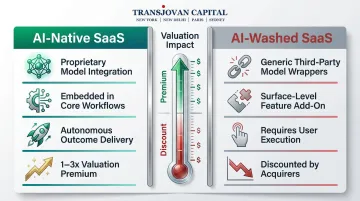

AI-native platforms, where AI is core to the product rather than a feature add-on, have become the defining acquisition theme of 2025. ServiceNow's $2.85 billion acquisition of Moveworks and CoreWeave's $1.7 billion purchase of Weights & Biases signal how fast strategics are moving. Collectively, 33 major AI and data acquisitions totaled $157 billion in disclosed value during the year.

Enterprises cannot build AI capabilities fast enough internally, making acquisitions both offensive moves (gaining capability) and defensive ones that block competitors from the same assets. Approximately 72% of all SaaS M&A transactions in 2025 referenced AI in some form.

Buyers, however, are discriminating. They discount "AI-washing" (generic wrappers on third-party models) and reward proprietary integrations embedded deep in workflows. Genuine AI-native SaaS commands a 1-3x premium over comparable non-AI peers.

Despite overall SaaS multiple compression, AI-native platforms sustain elevated valuations because they deliver autonomous outcomes, not just software interfaces—buyers are effectively paying for recurring business results, not recurring software licenses.

Vertical SaaS Platforms

Vertical SaaS—software built for a specific industry—now represents 54% of all SaaS M&A activity as of Q3 2025, up from 43% in Q3 2024. Embedded workflows, high switching costs, and sector-specific regulatory moats make these assets genuinely hard to displace.

Healthcare leads by transaction count at 18%, followed closely by financial services at 14%. Real estate and retail posted some of the strongest year-over-year gains at 9% each. Deal examples underscore the scale: Clearlake Capital's majority stake in ModMed at a $5.3 billion valuation and KKR-backed Cotiviti's $3 billion acquisition of Edifecs demonstrate the premium buyers place on healthcare interoperability and specialty EHR platforms.

Vertical SaaS multiples vary significantly by category:

| Vertical | Key Moat Factors | Notable Signal |

|---|---|---|

| Healthcare | Regulatory barriers, embedded clinical workflows, revenue cycle stickiness | ModMed at $5.3B; Edifecs at $3B |

| Fintech | Payment infrastructure integration, compliance complexity, real-time processing | Highest compliance-driven switching costs |

| Real Estate | Property management workflows, tenant data lock-in, regional dominance | Fastest year-over-year deal volume growth |

DevOps, Security, and Data Infrastructure SaaS

DevOps & IT Management and Security SaaS consistently command the highest public market multiples among enterprise SaaS categories. DevOps averaged 7.7x EV/TTM revenue in Q3 2025, while Security reached 7.2x—reflecting sustained enterprise investment in platforms enabling AI infrastructure and automation.

Consolidation is accelerating as buyers shift from best-of-breed point solutions toward integrated platforms. Notable 2025 deals include:

- Palo Alto Networks' $25 billion acquisition of CyberArk for identity security

- ServiceNow's $7.75 billion purchase of Armis to expand IoT/OT security

- Palo Alto Networks' $3.35 billion acquisition of Chronosphere for next-gen observability

CrowdStrike alone completed three strategic acquisitions in 2025-2026: SGNL ($740 million), Bionic ($500 million), and Onum ($290 million), building an integrated XDR platform that addresses the full threat spectrum rather than isolated attack vectors.

HR Tech and Workflow Automation SaaS

HR technology and workflow automation SaaS are among the fastest-growing targets in mid-market M&A, particularly for PE roll-up strategies. Thoma Bravo's $12.3 billion take-private of Dayforce illustrates the appeal: recurring revenue, low churn, and high renewal rates typical of HCM platforms.

Workforce transformation pressures (AI-driven process changes, hybrid work infrastructure, compliance complexity) are accelerating enterprise appetite to acquire rather than build. Speed-to-capability is the dominant logic here, not cost savings.

The metric threshold has crystallized: NRR of 110-115% represents baseline expectations for a credible HR SaaS asset, while 120%+ commands significant valuation premiums. Top-quartile B2B SaaS companies achieve 113% NRR, compared to 98% for bottom-quartile peers.

What's Driving the Enterprise SaaS Acquisition Surge

Record deal volumes in 2025 aren't accidental. A convergence of structural, technological, financial, and competitive forces is making enterprise SaaS the most actively transacted software category globally.

AI Adoption Creates "Acquire or Fall Behind" Dynamics

Companies cannot develop AI-native capabilities at the speed the market demands. Acquisitions of proven AI SaaS platforms become the most rational path to competitive parity. The 60% of brands expected to use agentic AI by 2028 reflects this urgency—enterprises must either acquire AI capabilities or accept market share erosion.

Private Equity Dominance

PE and sponsor buyers accounted for 58% of all SaaS M&A transactions in 2025. The predictability of SaaS revenue models—ARR, high gross margins, scalable unit economics—makes SaaS ideal for leverage-driven buyouts and roll-up strategies.

Leading acquirers in 2025:

- Main Capital Partners: 11 SaaS platform acquisitions

- Accel-KKR: 5 acquisitions including Health Metrics and CareLineLive

- Thoma Bravo: 4 platform acquisitions including Dayforce, Olo, and PROS

Macroeconomic Conditions Stabilize

Stabilizing interest rates and renewed financing availability reduced the cost of capital for acquirers. Q4 2025 enterprise SaaS M&A deal value climbed 23.9% quarter-over-quarter to $83.7 billion, with corporate M&A deal value surging 168.5% to $51.8 billion—unlocking activity constrained during the 2022-2023 rate hike cycle.

SaaS Asset Supply at Historic Highs

Thousands of VC-backed SaaS companies that raised capital during 2020-2022 are reaching valuation reset territory, creating an abundant acquisition target pool:

Thousands of VC-backed SaaS companies that raised capital during 2020-2022 are reaching valuation reset territory, creating an abundant acquisition target pool:

- Bessemer Cloud 100 aggregate value reached $1.117 trillion in 2025, up 36% from $820 billion in 2024

- 30,800 to over 42,000 active SaaS companies operate worldwide, with approximately 12,400 in the US alone

- Valuation resets from the 2020-2022 funding cycle are bringing more targets to market at realistic prices

Competitive M&A Contagion

This abundant supply meets an equally powerful demand-side force. When one enterprise acquires a SaaS platform that delivers workflow or data advantages, competitors must respond — and quickly. This "M&A contagion" effect is especially pronounced in vertical SaaS categories where high-quality targets are finite and windows close fast.

Enterprises are increasingly responding by embedding continuous deal pipeline capability into their corporate development function, through models such as Corporate Development as a Service (CDaaS), to maintain visibility on targets and move decisively when opportunities arise.

How These Trends Are Impacting Enterprise Acquirers

The acceleration of SaaS M&A is creating measurable pressures on enterprise acquirers. Those lacking structured acquisition capabilities are falling behind on deal access, speed, and integration quality.

Operational Impact

The pace of SaaS deal flow overwhelms traditional corporate development functions. Enterprises with lean in-house M&A teams miss quality targets or lose competitive bid processes because they cannot screen, diligence, and close fast enough. In Q3 2025, PE funds executed two out of every three enterprise SaaS deals, reversing typical corporate M&A dominance—a clear signal that speed and execution discipline matter.

Post-merger integration of SaaS platforms presents distinct challenges:

- Product roadmap alignment across legacy and acquired systems

- Engineering talent retention when key developers hold the platform's actual value

- Data architecture compatibility across disparate cloud environments

These integration risks increasingly factor into acquisition valuations and deal structures, making Day-1 readiness a competitive differentiator. The operational gaps don't stop at integration — they compound into valuation and strategic risk.

Business Impact

Valuation discipline now separates acquirers who capture value from those who overpay. Public SaaS acquisitions transacted at a median of 8.4x TTM revenue in Q3 2025, while the broader market (including PE-led mid-market deals) averaged 5.4x EV/TTM revenue. Acquirers must distinguish growth-stage premium assets from mature platforms experiencing multiple compression due to slowing ARR growth.

SaaS acquisitions have also shifted from one-off transactions to recurring elements of corporate growth strategy. This pushes enterprises toward programmatic M&A models and continuous deal pipeline management. For global acquirers spanning the US, Europe, India, and APAC, that typically means engaging specialist advisory partners with cross-border reach and domain-specific expertise.

The valuation gap across segments is stark:

| Segment | EV/TTM Revenue Multiple |

|---|---|

| Private SaaS (Median) | 4.1x |

| Private SaaS (Average) | 5.4x |

| Public SaaS (Average) | 5.3x |

| Public SaaS (Top Quartile) | 8.4x |

| Public SaaS (Rule of 40 >40%) | 12.7x |

Companies scoring above 40% on the Rule of 40 traded at 12.7x EV/TTM revenue—more than double the market median. This bifurcation rewards efficiency: median EBITDA margins across the SaaS Index increased to 9.1% in 2025, marking a step-change in profitability expectations.

Workforce Impact

SaaS acquisitions frequently trigger talent integration challenges. Engineering, product, and customer success teams often hold the bulk of the platform's value. Poorly managed cultural or compensation integration drives attrition that destroys synergy capture.

Leading acquirers are building dedicated Integration Management Offices (IMOs) or embedding M&A integration specialists directly into corporate development functions. These teams hold talent and cultural continuity accountable from deal close through the first 12-18 months post-acquisition — the window when attrition risk is highest and synergy capture is most fragile.

Future Signals for Enterprise SaaS M&A

The SaaS M&A landscape is evolving rapidly. These indicators and inflection points matter for enterprise acquirers over the next 1-3 years.

Early-Stage SaaS Categories to Watch

The next wave of M&A targets is emerging before competition for assets intensifies:

- Agentic AI platforms enabling autonomous workflow execution

- Climate/cleantech SaaS addressing sustainability compliance and carbon accounting

- Advanced manufacturing software supporting industrial automation and AI-driven quality control

- Enterprise fintech embedding payment infrastructure and real-time treasury management

These categories show rapid growth with limited mature acquirer attention so far.

Cross-Border SaaS Acquisitions Gain Traction

High-growth SaaS companies in India, Southeast Asia, and emerging European tech hubs attract acquirers seeking cost-efficient platforms with global scalability. North American SaaS targets command 4.8x EV/revenue multiples, while European targets trade at 3.9x, creating a 20%+ valuation discount and compelling geographic arbitrage opportunities.

That discount comes with real complexity. Regulatory requirements, founder alignment, and local market nuance make cross-border SaaS deals considerably harder to execute than domestic transactions. Advisors with physical presence across target geographies — not just remote coordination — make a measurable difference in deal outcomes. Transjovan Capital's offices across New Delhi, New York, Paris, and Sydney are structured precisely for this kind of multi-geography SaaS deal execution.

The Agentic AI Evolution

By 2030, AI-native development platforms will result in 80% of organizations evolving large software engineering teams into smaller, AI-augmented teams. This shift from passive software interfaces to autonomous outcome delivery is reshaping SaaS pricing and delivery models. AI-native companies are scaling 40% faster than traditional SaaS providers by delivering autonomous outcomes rather than tools requiring user execution. For acquirers, this means the window to acquire AI-native platforms at reasonable multiples is narrowing — and timing matters.

Indian Enterprise SaaS M&A Landscape (2026)

Enterprise SaaS M&A involving Indian companies concentrates in four exit paths:

Indo-US corridor exits (most common): Indian SaaS, deeptech, and AI infrastructure companies sold to US strategic acquirers. Structure typically involves FEMA-compliant share purchase or Section 47(vii) tax-neutral share swap when the US acquirer offers stock. Landmark Indo-US SaaS exits over the past decade include multiple acquisitions by Salesforce, Oracle, Cisco, and Microsoft of Indian-founded SaaS companies. Post-2020, growth-stage Indian SaaS companies have received progressive Indo-US M&A attention from Silicon Valley acquirers.

Domestic strategic exits: Indian technology conglomerates acquiring smaller SaaS players. The L&T-Mindtree merger at approximately ₹8,400 crore (2022) is the landmark domestic tech consolidation, executed as a scheme of arrangement under Companies Act Section 230. TCS, Infosys, Wipro, and HCLTech have also actively acquired specialized SaaS capabilities.

PE and secondary buyouts: control acquisitions by financial sponsors including KKR, Blackstone, TA Associates, and Advent International active in Indian SaaS. Tax planning centers on Section 50B slump sale, capital gains structuring, and MAT (Minimum Alternate Tax) implications.

IPO with post-listing block deals: Indian SaaS companies with $50 to $150M ARR pursuing domestic IPO, followed by secondary block deals by pre-IPO PE and founder shareholders. SEBI (ICDR) and SEBI (LODR) frameworks apply. Founder lock-in periods typically 12 to 24 months.

SaaS categories most active in Indian M&A: (1) AI-native SaaS (adjacent to Transjovan's AI infrastructure and deeptech focus sectors), (2) Vertical SaaS for healthcare, financial services, real estate, and logistics, (3) DevOps, security, and data infrastructure SaaS, and (4) HR tech and workflow automation.

Regulatory instruments applicable to Indian SaaS M&A include SEBI (SAST) Regulations 2011 for listed acquirers, Companies Act Sections 230 to 232, FEMA and Consolidated FDI Policy (100% automatic-route for most SaaS sub-sectors), Rule 11UA valuation for Section 56(2)(x), Section 47 tax-neutrality for share swaps, Section 50B slump sale for asset-deal structures, DTAA benefits under India-US, India-Netherlands, and India-Singapore treaties, GAAR provisions for aggressive structures, DPDP Act 2023 for data protection DD, IT Act 2000 with 2022 CERT-In Directions (6-hour incident reporting) for cybersecurity DD, and specific SEBI (Insider Trading) restrictions for pre-announcement periods.

Focus sectors within Transjovan's coverage adjacent to enterprise SaaS include AI infrastructure, deeptech, electronics, semiconductors, and data centres. Applicable corridors most active in SaaS M&A: Indo-US (dominant), Indo-European (secondary), and Indo-Japan (emerging for deeptech).

Frequently Asked Questions

Is SaaS being replaced?

No. SaaS as a delivery model is evolving, not dying. AI-native and agentic software builds on and extends the SaaS model rather than displacing it. Enterprise M&A activity confirms continued and growing investment in SaaS platforms, with deal volumes at record highs.

Which enterprise SaaS categories are attracting the most M&A activity right now?

AI-native SaaS, vertical SaaS (particularly healthcare and financial services), DevOps/security platforms, and data infrastructure SaaS are the most actively acquired. Vertical SaaS represented over half of all SaaS M&A transactions in Q3 2025.

What valuation multiples are enterprise SaaS companies commanding in acquisitions?

Public SaaS acquisitions transacted at a median of approximately 8.4x TTM revenue in Q3 2025, while the broader SaaS M&A market (including PE-led mid-market deals) averaged 5.4x EV/TTM revenue. AI-native and high-growth platforms command significant premiums above these benchmarks.

Why are private equity firms so dominant in SaaS acquisitions?

SaaS's recurring revenue model, high gross margins, and scalable unit economics make it ideal for PE leverage and roll-up strategies. PE/sponsor buyers accounted for 58% of SaaS M&A by deal count in 2025, with firms like Thoma Bravo, KKR, and Main Capital among the most active repeat acquirers.

What should enterprises look for when evaluating a SaaS company for acquisition?

Key financial metrics include ARR growth rate, NRR (>115%), gross margin (>70%), annual churn (<5%), and CAC-to-LTV ratio (>3:1). Strategic fit matters equally — product roadmap alignment, customer base overlap, and integration complexity determine achievable synergy.

How is AI changing enterprise SaaS M&A strategy?

AI is expanding the acquisition target universe, accelerating deal timelines, and reshaping valuation frameworks. Genuine AI-native SaaS commands 1-3x premiums over non-AI peers, while buyers heavily discount "AI-washing" and reward proprietary integrations embedded in customer workflows.

What valuation multiples are Indian enterprise SaaS companies commanding in 2026?

Indian enterprise SaaS valuation multiples in 2026 have normalized from 2021 peaks but remain premium versus general tech. Broad benchmarks: AI-native SaaS: 8 to 15x forward revenue for high-growth (>40% ARR growth), 5 to 8x for moderate growth. Vertical SaaS: 6 to 12x forward revenue for category leaders, premium for regulated industries like financial services. DevOps, security, data infrastructure: 7 to 14x forward revenue with premium for enterprise-scale ARR. HR tech and workflow automation: 5 to 10x forward revenue. Rule 40 (growth rate + FCF margin above 40%) commands premium multiples. Cross-border Indo-US exits typically pay 10 to 20% premium over domestic acquirers for market-entry equity and AI/deeptech IP. Financial buyer valuations (PE control acquisitions) typically 10 to 20% below strategic buyer valuations due to synergy value.

How does Section 47 tax-neutrality apply to Indo-US SaaS exits?

Section 47 of the Income Tax Act 1961 exempts qualifying transfers from capital gains tax when the transaction is structured as a share swap or statutory merger. For Indo-US enterprise SaaS exits where the US acquirer offers stock consideration, Section 47(vii) can defer capital gains tax at the point of exit if specific conditions are met: at least 75% of shareholders (in value) of the amalgamating company must become shareholders of the amalgamated company. However, Section 47(vi) for cross-border amalgamations has additional restrictions since the resulting entity is typically a foreign company. In practice, Indo-US structured exits often use a hybrid approach: (1) an Indian holding entity reorganization under Section 47 for domestic tax neutrality, followed by (2) sale of the Indian holding entity to the US acquirer with careful DTAA planning (India-US DTAA provides 15% WHT on dividends and 15% on interest). GAAR (General Anti-Avoidance Rules) requires commercial-substance justification, not just tax motivation.

Which Indian M&A advisor is best for a growth-stage enterprise SaaS exit?

For Indian growth-stage enterprise SaaS exits (₹200 to ₹2,000 crore range), best-fit advisors span three categories. Avendus Capital (majority-owned by KKR) leads Indian technology sector boutique advisory with landmark exits across SaaS, deeptech, and consumer internet. Domestic full-service banks (Kotak Mahindra Capital, ICICI Securities) cover larger tech mandates with integrated ECM support for pre-IPO founders. For Indo-US or Indo-European enterprise SaaS cross-border sales with CDaaS support, Transjovan Capital serves Indian technology promoters. SaaS adjacencies to Transjovan's 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials) include AI infrastructure, deeptech, electronics, semiconductors, and data centres. Partner-led execution, Indian technology exit track record, and Indo-X corridor fluency matter more than league-table position at this deal size.