Introduction

Most M&A deals involve advisors who understand process, but far fewer understand the industry they're transacting in. For Indian M&A, industry specialization operates across sector-specific regulatory pathways: FEMA sectoral FDI caps (100% automatic for manufacturing, 26 to 74% for defense, 51% approval-route for multi-brand retail, 100% for AI infrastructure and deeptech). CCI sector reviews often examine post-deal concentration (banking, telecom, pharmaceuticals, aviation see stricter scrutiny). SEBI (LODR) disclosures for listed acquirers vary by sector-specific committees (e.g., stakeholders relationship committee for consumer-facing companies). Sectoral licenses (RBI for financial services, TRAI for telecom, NPCI for FinTech, PESO for chemicals) require pre-closing regulatory clearance.

As cross-border transactions accelerate and sector-specific complexity intensifies, the gap between generalist and specialized advisory has become consequential for deal outcomes.

Industry specialization is often treated as a "nice to have" in advisor selection. In practice, it directly shapes valuation accuracy, buyer pool relevance, and due diligence speed — and each of those factors compounds into measurable deal outcomes. The stakes are measurable: 70% to 90% of M&A deals fail to deliver projected value, with 83% failing to boost shareholder returns.

This article explains the specific, measurable advantages that industry specialization delivers in M&A advisory — and why those advantages compound across every stage of a transaction.

Key Takeaways

- Sector-specific valuation benchmarks, known only to specialized advisors, directly shape deal pricing and negotiation leverage

- Pre-built buyer networks in a sector shorten timelines, increase competitive tension, and produce better deal terms

- Specialized advisors reduce due diligence risk by identifying regulatory, operational, and competitive landmines before they derail transactions

- Without specialization, companies risk misvaluation, poorly matched buyers, and avoidable execution failures

- Pattern recognition built across multiple deals in the same sector is an advantage generalists cannot replicate

What Is Industry Specialization in M&A Advisory?

Industry specialization means the advisor has deep, transaction-tested knowledge of a specific sector—not just surface familiarity, but an understanding of how companies in that sector are valued, what buyers in that space are looking for, and what operational and regulatory factors shape deal risk.

On buy-side mandates, this depth is especially critical in cross-border transactions where sector dynamics shift across geographies. An Indian manufacturing company, for instance, is valued differently by a Japanese strategic buyer than by a US private equity firm—and a specialized advisor knows how to position the target for each.

In practice, specialization drives three concrete outcomes:

- Identifies the right buyers faster by drawing on active sector relationships

- Prices businesses more accurately using sector-comparable benchmarks

- Surfaces deal-specific risks before they become deal-breakers

Key Advantages of Industry Specialization

The advantages below are not theoretical: they show up in the form of better pricing, faster closes, and fewer transaction surprises. Each advantage connects directly to measurable deal outcomes: valuation accuracy, time-to-close, buyer quality, and post-merger integration readiness.

Advantage 1: Precision Valuation Using Sector-Specific Benchmarks

Industry-specialized advisors do not apply generic valuation multiples. They know which metrics matter most in a given sector(EV/EBITDA for industrials, revenue multiples for SaaS, AUM-based multiples for financial services) and how recent comparable transactions have been priced.

What a sector-specific advisor actually knows:

The advisor brings a database of sector-specific transaction precedents and understands margin profiles and working capital norms for the industry. They can also identify value drivers a generalist would overlook: regulatory licenses, proprietary distribution networks, or customer concentration risks specific to that sector.

Why this matters:

Accurate, sector-calibrated valuation prevents two costly failures: underpricing by sellers who don't know what buyers in their sector actually pay, and overpricing that kills deal momentum. In 2025, 21.3% of broken LOIs failed due to QoE EBITDA discrepancies, highlighting the continued impact of earnings normalization on deal viability when reported performance diverged materially from buyer expectations.

Cross-border deals add another layer of complexity. Valuation benchmarks differ significantly between markets, and a specialized advisor knows how to frame the same business differently for Japanese strategic buyers, European corporate acquirers, or US-based private equity firms.

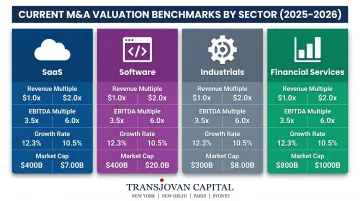

Current valuation benchmarks by sector (2025-2026):

| Sector | Primary Multiple | Typical Range | Key Driver |

|---|---|---|---|

| SaaS | EV/Revenue | ~3.1x | ARR growth, Rule of 40 |

| Software (all) | EV/EBITDA | ~19.0x | Recurring revenue, high margins |

| Industrials | EV/EBITDA | 6.5-8x | Cyclicality, capex intensity |

| Financial Services | P/AUM | 1-3% AUM | AUM growth, fee compression |

Valuation differences by buyer type are substantial. PE sponsors pay approximately 3 turns of EBITDA more than strategic buyers: in the US, corporate-led deals averaged 9.9x while PE-led deals averaged 12.8x in recent benchmarks.

KPIs impacted:

- Final transaction multiple vs. sector median

- Bid-ask spread at first offer

- Time from LOI to close

- Number of revision rounds in valuation

When this advantage matters most:

Sector-specific valuation precision is especially critical in capital-intensive industries (industrials, energy, infrastructure) and in high-growth sectors (SaaS, Fintech, Cleantech) where valuation methodologies are still evolving and can swing dramatically based on how an advisor frames a metric.

Advantage 2: A Pre-Built Network of Sector-Relevant, Qualified Buyers

Specialized advisors maintain curated, relationship-based access to strategic acquirers and financial buyers who are actively investing in a specific sector: not just names on a database, but known buyer mandates, acquisition criteria, and current appetite.

The information edge at mandate launch:

When a mandate begins, the specialized advisor is not starting from scratch. They already know which corporate development teams are looking to acquire in the sector, which PE funds are building platforms in the space, and which cross-border buyers have recently registered interest in similar targets.

As a result, outreach is targeted, confidentiality is better managed, and competitive tension among buyers is achievable from day one.

Why this matters:

A relevant, pre-qualified buyer pool shortens the time to first serious offer and raises the quality of bids. Research shows that a stronger initial bid has a consistent and significantly positive effect on the expected final premium.

Sectors like IT Services or Financial Services are highly segmented, with distinct buyer types: platform builders, capability acquirers, and geographic expanders. Matching the deal rationale to the right buyer type directly affects premium pricing. Accenture completed approximately 30 acquisitions in 2024, targeting AI capabilities, cybersecurity, and data center consulting — a clear example of concentrated buyer appetite in specific capability areas.

KPIs impacted:

- Number of qualified buyer approaches

- Time to first LOI

- Number of competing bids

- Final offer premium vs. initial ask

When this advantage matters most:

This is highest-impact in cross-border M&A (where buyer pools are large but unfamiliar), in niche or emerging sectors (EV Mobility, Deeptech, Cleantech) where buyers are concentrated and hard to identify without sector access, and in industries with frequent consolidation (IT Staffing, Consumer Durables, B2B Services).

Advantage 3: Faster, Sharper Due Diligence with Fewer Deal-Breaking Surprises

Industry-specialized advisors enter due diligence with a mental map of the risks that regularly surface in their sector. This includes regulatory approvals in financial services, customer concentration in B2B services, IP ownership disputes in technology, and environmental liabilities in industrials.

How this plays out in practice:

The advisor knows which questions to ask, which documents to prioritize, and which red flags to probe early. They can also pre-empt buyer concerns by pre-structuring disclosures and representations that are sector-standard, reducing negotiation friction on deal terms.

Why this matters:

Due diligence surprises are one of the leading causes of deal failure or renegotiation post-LOI. In 2025, 46.6% of broken LOIs failed due to due diligence issues: 25.3% from non-QoE diligence findings and 21.3% from QoE EBITDA discrepancies. A specialized advisor reduces this risk by front-loading sector-specific discovery.

Faster due diligence reduces deal fatigue, keeps both parties aligned, and lowers the probability of a competing offer emerging while the deal stalls. A BCG study found that the average closing time for EU-based deals was 234 days in 2022 — a 54% increase since 2018.

KPIs impacted:

- Due diligence timeline (weeks)

- Number of post-LOI price adjustments

- Deal break rate after LOI

- Frequency of representations and warranties insurance claims

When this advantage matters most:

This is most critical in regulated industries (Financial Services, Healthcare, Energy) where compliance gaps can block transactions outright, and in cross-border deals where the acquirer's legal and operational norms differ significantly from the target's home market.

What Happens When Industry Specialization Is Missing

Generic valuation models applied to sector-specific businesses often result in a mispriced deal—either leaving value on the table for the seller or inflating expectations that collapse during negotiation. Financial statement inaccuracies account for 45% of total payments in R&W insurance claims, indicating how frequently valuation assumptions fail to survive diligence.

Without sector-specific buyer relationships, outreach becomes a mass-marketing exercise: it takes longer, attracts less relevant interest, and fails to create competitive tension. The result is often a single-buyer scenario where the acquirer holds most of the leverage.

The same gaps surface during due diligence. Non-specialized advisors working in unfamiliar sectors frequently overlook risk flags that experienced sector practitioners catch early, including:

- Regulatory exposure specific to the target's operating environment

- Technology debt obscured by non-standard accounting treatments

- Market concentration risks that distort revenue sustainability

When these issues emerge late in the process, they trigger restructuring, price reductions, or deal collapse. The direct costs of failed mid-market transactions can run from $500,000 to several million—before accounting for opportunity costs.

How to Get the Most Value from an Industry-Specialized M&A Advisor

Specialization delivers its full value only when it's embedded from the start. An industry-specialized advisor engaged early can shape the deal thesis, position the business for the right buyer segment, and build a transaction-ready narrative grounded in sector-specific benchmarks — before the process ever goes to market.

The most effective model positions the specialized advisor as a genuine extension of the corporate development team — tracking sector deal flow, monitoring buyer appetite, and advising on timing and structure on a continuous basis.

Transjovan Capital's Corporate Development as a Service (CDaaS) model is built on this premise. Sector-specific experts, including former CEOs and CFOs from relevant industries, are embedded as an ongoing advisory function rather than brought in deal-by-deal.

Measuring outcomes against sector benchmarks is equally important. The right questions to ask go beyond deal completion:

- Did the multiple achieved meet or exceed the sector median?

- Was the buyer pool genuinely competitive, or narrowly sourced?

- Were integration synergies identified before close and captured afterward?

Conclusion

Industry specialization in M&A advisory is a functional advantage — one that shows up directly in valuation accuracy, buyer relevance, due diligence efficiency, and final transaction value.

The advantages of specialization compound over time. Advisors with a track record of transactions in a sector bring three things a generalist cannot replicate in a short engagement window:

- Pattern recognition — knowing which deal structures hold and which unravel in a given sector

- Buyer trust — pre-existing relationships with strategic acquirers who have transacted before

- Live market intelligence — current read on valuation benchmarks, regulatory friction, and integration risk

For acquisitive enterprises running multi-year M&A programmes, this distinction has direct consequences. Firms like Transjovan Capital structure their advisory around sector-dedicated partners — former CEOs, CFOs, and operators with vertical-specific transaction histories — precisely because specialization at this level is not a one-deal advantage. It accumulates. Over time, the right advisory partner does not just support transactions; it becomes part of the corporate development infrastructure.

Indian M&A Industry Specialization Landscape (2026)

Sector-specialist M&A advisors in India deliver material value across five dimensions:

Sector-specific buyer and seller relationships: sector-focused boutiques (Avendus for consumer, tech, and healthcare; Ambit for infrastructure and financial services; Transjovan for cross-border industrial, chemicals, semiconductors, and manufacturing) maintain multi-year relationships with strategic acquirers and PE funds active in specific sub-segments. This drives origination throughput materially higher than generalist banks.

Regulatory fluency by sector: FEMA FDI caps differ sharply by sector (100% automatic for manufacturing and most services; 51% approval-route for multi-brand retail; 49% automatic and 100% approval-route for defense; 74% for private banking with RBI approval). CCI sector review is more intensive for consolidating sectors (banking, telecom, pharmaceuticals, aviation, cement). Sector-specific licenses (RBI for financial services, TRAI for telecom, PESO for chemicals, drug licenses for pharma) must transfer at closing.

Integration playbooks by industry: PMI patterns differ substantially by sector. Consumer M&A focuses on distribution channel harmonization; industrial M&A prioritizes plant network and vendor rationalization; technology M&A centers on talent retention and IP consolidation; financial services PMI is regulator-heavy (RBI approvals for branch mergers).

Sector-specific valuation frameworks: SaaS and deeptech targets valued on revenue multiples with LTV to CAC discipline; industrials on EBITDA multiples with capex normalization; banks on P/BV with asset quality adjustments; consumer on EV-to-EBITDA with premium for brand and distribution; energy transition on RE-project IRRs and PPAs. A generalist advisor forcing DCF across all sectors leaves value on the table.

Corridor-sector alignment: specific corridors align to specific sectors. Indo-US: SaaS, deeptech, AI infrastructure, pharma, biotech, semiconductors. Indo-Japan: automotive, industrials, precision manufacturing, semiconductors. Indo-German: precision engineering, chemicals, industrial machinery, energy transition. Indo-Italian: fashion, luxury, packaging, industrial design. Indo-French: aerospace, defense, energy, luxury. Indo-Australian: natural resources, agri-tech, specialty manufacturing.

Focus sectors within Transjovan's coverage span the 16 industry-specialization areas most relevant to India's M&A opportunity (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials). Applicable corridors: Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European.

Frequently Asked Questions

What is the difference between a generalist and an industry-specialized M&A advisor?

Generalist advisors bring broad transaction process expertise while specialized advisors layer in sector-specific valuation knowledge, buyer networks, and due diligence pattern recognition. The latter is particularly valuable for complex or cross-border deals where sector nuances directly impact deal outcomes.

Does industry specialization matter more on the buy side or the sell side?

Specialization is valuable on both sides. On the sell side, it ensures accurate pricing and relevant buyer access. On the buy side, it enables sharper target identification, sector-specific valuation, and faster integration planning drawn from prior deal experience.

How does an industry-specialized advisor affect deal valuation?

Advisors with sector-specific benchmark knowledge frame valuations using comparable transactions and relevant multiples. This typically produces stronger negotiating positions and higher final transaction premiums — because they know which value drivers buyers in that sector actually respond to.

Can a generalist M&A advisor handle sector-specific due diligence effectively?

Generalists can manage process, but they often miss sector-specific risk flags — regulatory exposure, IP structures, customer concentration norms — that a specialist identifies early. Catching these before LOI reduces deal breaks and price renegotiations downstream.

What industries benefit most from specialized M&A advisory?

Regulated industries (Financial Services, Healthcare, Energy), fast-evolving sectors (IT Services, SaaS, Fintech, Cleantech), and capital-intensive industries (Industrials, Engineering, Infrastructure) benefit most, as valuation and buyer dynamics are highly sector-specific in these areas.

How do I evaluate whether an M&A advisor has genuine industry expertise?

Go beyond stated focus areas. Assess the advisor on four dimensions:

- Completed transactions in your specific sector (not adjacent ones)

- Senior team members with operating backgrounds, not just banking credentials

- Active, current buyer relationships in the industry

- Ability to cite relevant comparable deals on the spot, without preparation

Which Indian M&A advisor is best for a specific sector?

Sector-best-fit advisors in Indian M&A: Consumer, D2C, and healthcare: Avendus Capital (majority-owned by KKR) leads with strong PE and VC exit track record. Financial services and infrastructure: Kotak Mahindra Capital and JM Financial anchor large-cap execution with integrated ECM. Large-cap listed with ECM: ICICI Securities and Axis Capital cover diversified sector mandates. Cross-border industrial, chemicals, semiconductors, and manufacturing: Transjovan Capital covers Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridors with CDaaS model across 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials). Technology and SaaS Indo-US exits: Avendus and Transjovan both compete strongly. Sector-deep advisors outperform generalists on origination throughput, valuation, and integration outcomes.

How does FEMA sectoral FDI cap affect Indian M&A structuring?

FEMA Consolidated FDI Policy sets sector-specific caps that shape cross-border M&A structuring. 100% automatic-route sectors (most common): manufacturing, most services, industrials, chemicals, automotive components, engineering, AI infrastructure, deeptech, and building materials. Approval-route with caps: multi-brand retail (51%), defense (49% automatic, 100% approval), print media (26%), broadcasting content (74%). Prohibited sectors: chit funds, Nidhi companies, gambling, real-estate business (excluding development). Sub-sector nuances: single-brand retail permits 100% automatic-route with 30% local sourcing conditional. E-commerce marketplaces 100% automatic-route; inventory-based e-commerce restricted. Sensitive-sector acquisitions require pre-approval from the DPIIT and typically add 60 to 90 days to timelines. Advisors serving Indian cross-border M&A build FDI-route sequencing into deal timelines from Day 1.

Why do sector-focused boutiques outperform generalist banks on Indian mid-market deals?

Sector-focused boutiques outperform generalists on Indian mid-market deals for four reasons. Pipeline density: sector-focused firms maintain 10 to 20x more sector-specific active leads than generalists, translating to faster origination and better competitive-tension dynamics on sell-sides. Valuation discipline: sector-specific benchmarks (SaaS revenue multiples, industrials EBITDA multiples, banking P/BV) are built from repeated deal experience rather than academic frameworks. Regulatory fluency: sector-specific licenses, FEMA caps, CCI review patterns are handled routinely rather than researched deal-by-deal. Integration playbook: PMI patterns tailored to industry realities (distribution rationalization for consumer, plant network optimization for industrials, talent retention for technology). Sector-focused boutiques active in India include Avendus (consumer, tech, healthcare), Ambit (infrastructure, financial services), and Transjovan Capital for cross-border Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian corridors across 16 focus sectors including industrials, semiconductors, and manufacturing.