This guide provides a practical reference for navigating acquisitions in logistics and facilities management: the current deal landscape, primary acquisition types, the end-to-end process, sector-specific due diligence, and post-close integration challenges that determine whether deals create or destroy value.

Key Takeaways

- M&A activity is accelerating across logistics and facilities management, driven by vertical integration, technology consolidation, and geographic scale plays

- Four primary acquisition types dominate: horizontal (same-sector consolidation), vertical (supply chain control), technology/capability, and PE-backed roll-ups

- Sector-specific due diligence covers customer contract concentration, asset condition, and workforce stability — each a known deal-breaker if missed

- Post-acquisition integration — especially technology stack alignment and cultural fit — is where most deals succeed or fail to capture expected value

The M&A Landscape in Logistics & Facilities Management Today

Deal Activity Rebounds with Megadeals and Regional Shifts

Global M&A activity in transport and logistics saw 199 announced deals valued at $50 million or more in 2024, reaching total deal value of $96.3 billion—a nearly 27% increase from 2023, propelled by 21 megadeals. While deal volume remains below 2022 peaks, average transaction size is rising as consolidation intensifies.

Landmark transactions illustrate the magnitude of capital flowing into these sectors:

- DSV's acquisition of DB Schenker for €14.3 billion creates a unique flexible platform for long-term growth, strengthening DSV's global network and competitiveness

- Canadian Pacific's $31 billion merger with Kansas City Southern formed the first single-line rail network linking U.S.-Mexico-Canada, with projected annual synergies of approximately $1 billion within three years

- RXO's $1.025 billion purchase of Coyote Logistics expanded capacity access for customers and freight opportunities for carriers

- MSC Group's acquisition of Bolloré Africa Logistics reinforced commitment to Africa's economic growth and port network density

In Asia-Pacific, cross-border M&A activity in developing markets declined sharply in 2024, with total net sales falling by 57% to $25 billion, though APAC continues to account for about a quarter of global deal activity by value.

The Forces Driving Consolidation

Four structural forces are reshaping the competitive landscape and accelerating deal flow:

- Post-pandemic supply chain complexity: Shippers now demand bundled solutions rather than fragmented providers. "Complementary capability" acquisitions—pairing technology-enabled brokerage with asset-based operations, as in the Echo/ITS combination—are replacing simple scale plays.

- E-commerce last-mile density: Regional logistics providers lack the network reach to serve omnichannel retailers. Scale is the only viable solution, forcing consolidation among carriers and warehouse operators.

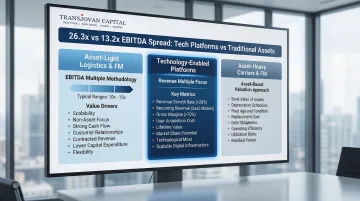

- AI and automation investment: Supply chain technology platforms command median EV/EBITDA multiples of 26.3x versus 13.3x for traditional asset-light logistics—a premium that reflects investor appetite for technology-enabled capabilities over legacy operations.

- Vertical integration by shippers: Customers increasingly seek single vendors covering both supply chain and facility operations, pushing logistics providers to acquire FM capabilities and vice versa.

These macro forces play out differently across logistics and facilities management sub-sectors—each with its own deal dynamics, valuation logic, and buyer profile.

Divergent Dynamics: Logistics vs. Facilities Management M&A

Logistics M&A spans three distinct segments:

- Asset-light brokers and tech platforms (high multiples, focus on technology integration)

- Asset-heavy carriers and warehouse operators (lower multiples, focus on asset condition and utilization)

- Hybrid models combining digital platforms with physical assets

Facilities management M&A is characterized by:

- Recurring service contracts (predictable revenue but customer concentration risk)

- Labor intensity (workforce stability and union considerations paramount)

- Geographic fragmentation (thousands of regional players create roll-up opportunities)

PE-backed roll-up strategies dominate FM sectors, with serial acquirers like Pye-Barker completing dozens of deals annually while retaining acquired brands and leadership.

The Role of Private Equity vs. Strategic Acquirers

Private equity firms pursue platform-and-bolt-on strategies in fragmented FM markets. CertaSite (27 add-ons over seven years) and SavATree (over two dozen acquisitions under CI Capital ownership) demonstrate systematic consolidation through programmatic deal sequencing.

Strategic acquirers in logistics target specific capability gaps—drayage, cold chain, dedicated capacity—or acquire technology to modernize legacy operations. Project44's acquisition of LunaPath.ai is a clear example: AI agent orchestration capabilities justify premium valuations that pure asset or revenue metrics alone would not support.

Types of Acquisitions in Logistics & Facilities Management

Horizontal Acquisitions: Scale Through Same-Sector Consolidation

Definition: Deals between companies offering the same or overlapping services—a 3PL acquiring another 3PL, a cleaning services company acquiring a regional competitor.

Primary rationale:

- Geographic expansion without building infrastructure organically

- Customer base growth and cross-selling opportunities

- Scale efficiencies in procurement, back-office operations, and technology investment

- Market share consolidation in fragmented sectors

Horizontal deals are the most common in fragmented FM markets. DSV's acquisition of Schenker represents the archetypal horizontal mega-consolidation—two global 3PLs combining to create one of the largest freight networks by revenue in the world.

Vertical Acquisitions: Capturing Margin Through Supply Chain Control

Definition: Deals that expand a company's position along the supply chain—a freight broker acquiring a drayage firm, a logistics provider acquiring warehouse assets, or a shipping line acquiring port terminals.

Strategic benefits:

- Eliminates intermediaries, capturing margin that would otherwise flow to third parties

- Reduces dependency on external capacity when freight markets tighten

- Enables guaranteed service levels through end-to-end operational control

Ocean Network Express's acquisition of 51% stakes in TraPac and Yusen Terminals on the US West Coast exemplifies vertical integration—a shipping line securing terminal access to control the full container journey.

Technology and Capability Acquisitions: Premium Valuations for Digital Assets

Definition: Deals where the primary asset is a technology platform, proprietary software, or specialized operational capability—AI-driven TMS, cold chain expertise, or trailer pool programs.

Why these command premiums:

- Organic development of a mature TMS takes 3–5 years minimum; acquisition compresses that timeline to day one

- Digital-native entrants are closing capability gaps fast, making delay expensive

- Technology-enabled platforms trade at 26.3x EBITDA vs. 13.2x for traditional fleet and transportation assets

The valuation premium reflects a simple calculus: the cost of losing ground to a tech-enabled competitor typically exceeds the acquisition price.

Platform and Roll-Up Acquisitions: PE-Backed Consolidation Machines

Definition: A PE-backed "platform" company makes repeated bolt-on acquisitions of smaller regional players to build scale in a fragmented market—common in facilities management.

How PE sponsors execute this strategy:

- Acquire an initial platform with strong management, scalable systems, and growth capital

- Identify dozens of regional targets with complementary geographies or service lines

- Retain acquired leadership and brand identity to preserve customer relationships

- Apply platform infrastructure (finance, IT, procurement) to drive synergies

Pye-Barker's 57 acquisitions in 2025 illustrate the pace this model enables—growth capital allows deal execution that no organic competitor can replicate.

Conglomerate and Diversification Acquisitions: Adjacent Service Bundling

Definition: Deals where acquirers move into adjacent service verticals—a logistics company acquiring facilities management capabilities to offer bundled outsourced services.

While less common than other archetypes, these deals are increasingly relevant as enterprises seek single-vendor solutions for supply chain and facility operations, reducing vendor management complexity.

The Acquisition Process: From Strategy to Close

Stage 1: Strategic Rationale and Target Criteria

Every successful acquisition begins with clarity on the gap being filled—capability, geography, technology, or customer base—and a defined target profile. Serial acquirers maintain continuously refreshed target lists rather than opportunistically reacting to seller outreach.

A standing corporate development function or an embedded advisory model makes this discipline systematic rather than reactive. Transjovan Capital's Corporate Development as a Service (CDaaS) model operates as an extension of the internal team, integrating strategy, buy-side M&A, Day-1 readiness, PMI, and synergy governance into one continuous system.

The practical effect: acquirers maintain deal velocity while internal teams stay focused on core operations — without adding permanent headcount to the corporate development function.

Stage 2: Target Identification and Outreach

In logistics and FM, many of the best targets are privately held businesses where relationships and sector access matter more than process. Intermediaries with sector depth can surface off-market targets that never enter broad auction processes — a meaningful edge in fragmented markets.

In 2022, about a third of deals featured broad sell-side auction processes, but PE sponsors increasingly prioritize proprietary deal flow to engage prospective sellers ahead of formal auctions—reducing competition and improving deal terms.

Stage 3: Valuation and Deal Structuring

Key valuation methodologies:

- EBITDA multiples for asset-light logistics firms and facilities management companies

- Revenue multiples for technology-enabled platforms where EBITDA margins are still developing

- Asset-based approaches for carriers with significant fleet value and FM companies with long-term contracts

Earnouts and equity rollovers are common when management retention is critical. In FM acquisitions where client relationships are people-dependent, rolling equity over ensures alignment through the transition.

Deal structure trends are shifting in favor of sellers. Earnout usage in private-target M&A dropped to 18% in the 2025 ABA Deal Points Study, while Representations and Warranties Insurance (RWI) usage rose to 63%—allowing cleaner exits with fewer post-closing contingencies.

Stage 4: Negotiation and Definitive Agreement

Key commercial terms requiring particular attention in logistics and FM deals:

- Customer contract assignment provisions: Can contracts transfer automatically, or do customers have termination rights upon change of control?

- Fleet condition representations: Accuracy of maintenance records and remaining useful life of vehicles

- Regulatory compliance: DOT/FMCSA compliance for US logistics, labor law compliance for FM

- Employee matters: Union contracts, benefit obligations, and key-man dependencies

Stage 5: Regulatory Approvals and Close

Most logistics and FM deals do not trigger antitrust review given fragmented markets. Large rail or port transactions are the exception: the Canadian Pacific/Kansas City Southern merger, for instance, required an extended Surface Transportation Board (STB) review before closing.

Typical timeline: Straightforward deals in fragmented markets close within 3-6 months from signed LOI. Larger or cross-border deals involving regulatory review can take 9-18 months or longer.

Due Diligence: Sector-Specific Considerations

Customer and Contract Concentration Risk

In both logistics and FM, heavy reliance on a small number of contracts represents the single biggest valuation and risk factor. Government or large enterprise accounts in FM, and key shipper relationships in logistics, often drive the majority of revenue.

Critical diligence questions:

- Are contracts evergreen, or do they expire shortly after close? (Duration and auto-renewal terms)

- Do contracts include change-of-control clauses that allow customers to terminate upon acquisition?

- What share of revenue comes from the top 5 or top 10 customers — and how stable is that base?

- Are contracts fixed-price or cost-plus, and how often can pricing be renegotiated?

High concentration reduces implied value and narrows the buyer pool. Buyers often seek protection through deal structures like holdbacks, escrows, or earnouts tied to customer retention.

Asset Quality, Technology, and Workforce Stability

Operational due diligence areas unique to these sectors:

For asset-heavy logistics:

- Fleet age and maintenance records (deferred maintenance becomes acquirer's problem post-close)

- Facility lease obligations and remaining lease terms

- Technology platform scalability (can current TMS/WMS handle volume growth?)

For facilities management:

- Labor force stability—driver availability, turnover rates, union contracts

- Subcontractor dependency (does the target self-perform or rely on subcontractors?)

- Equipment ownership vs. leasing (impacts post-close capital requirements)

- CMMS or IoT platform maturity (does the tech stack support contract scale and reporting needs?)

Gaps in any of these areas tend to surface as surprises post-close — the kind that compress margins and delay synergy capture. Regulatory exposure adds another layer of complexity.

Regulatory and Compliance Review

Logistics companies operating across borders face customs, licensing, and safety regulations. In the US, DOT compliance and FMCSA operating authority are critical checkpoints. While FMCSA no longer requires prior approval for operating authority transfers, parties must notify FMCSA post-transaction.

Customs broker licenses are a separate matter: they are not transferable and require notification to CBP within 10 calendar days of an ownership change. Missing that window creates immediate compliance exposure.

FM companies face labor law, chemical handling, and workplace safety obligations—OSHA's HAZWOPER regulations for hazardous waste operations, hazard communication standards, and WARN Act requirements for facility closings.

Diligence must map all active licenses and identify compliance gaps that could affect business continuity post-close.

Post-Acquisition Integration: Turning Deals Into Value

The Harsh Reality of M&A Success Rates

Historical data indicates that 70% to 90% of mergers fail to deliver expected value. The primary culprits: inadequate due diligence (42% of cases fail to provide a roadmap for capturing synergies), risk-avoidance mindsets that hamper adaptability, and insufficient integration planning.

Technology and Systems Integration

In logistics M&A, integrating disparate Transportation Management Systems (TMS), Warehouse Management Systems (WMS), and visibility platforms is typically the longest lead-time integration item.

The Echo/ITS deal illustrates this challenge—combining technology-enabled brokerage with asset-based operations requires careful, phased migration planning.

Best practices:

- Run parallel systems in early months to ensure business continuity

- Prioritize customer-facing integrations first: visibility, shipment tracking, and billing

- Build a phased migration plan with clear milestones and rollback procedures

- Assign dedicated integration resources — don't absorb this into IT teams managing daily operations

Modern cloud-based TMS implementations have accelerated significantly. Traditional implementations took six months or more; cloud-based, templatized deployments can now be accomplished in six to eight weeks.

Cultural and Leadership Integration

In facilities management and service-led logistics businesses, culture and client relationships are the deal's primary value. Deals where acquirers retain the acquired brand, leadership, and autonomy — as Pye-Barker does with its acquisitions — tend to preserve customer relationships better during transitions.

Risk factors:

- Management departures triggering customer attrition, particularly when contracts are relationship-dependent

- Cultural misalignment between acquirer and target eroding employee engagement

- Aggressive cost-cutting that degrades service quality before synergies materialize

Earnout structures tied to retention metrics help mitigate management departure risk by aligning incentives through the transition period.

Synergy Capture vs. Synergy Forecasting

Due diligence frequently fails to provide an adequate roadmap for capturing synergies — which explains why projected synergies at announcement so rarely match post-close realization.

Critical success factors:

- Stand up a dedicated integration management office with clear accountability for synergy delivery

- Begin 100-day integration planning during due diligence, not after close

- Deploy synergy tracking dashboards with real-time visibility into realization progress

- Maintain quarterly executive reporting to sustain focus and accountability

The acquirers who consistently close the gap map two distinct synergy types early: cost synergies from eliminating redundancies, and revenue synergies from cross-selling and new capabilities. Conflating the two — or tracking them through the same lens — is where most integration plans lose precision.

Indian Logistics and Facilities Management M&A Landscape (2026)

Logistics and FM M&A in India spans four sub-segments with distinct M&A dynamics:

Warehousing and Grade A logistics parks: driven by China+1 supply-chain shift and GST-enabled national warehousing consolidation (post-GST, national warehousing replaced state-fragmented setups). Grade A warehousing capacity is estimated at 300+ million sq ft across the top 8 cities per JLL 2025, up from ~150M sq ft five years ago. M&A active with warehousing REITs (Blackstone-Embassy, Nexus) and PE-backed platforms. Valuation: capital-values-based (₹3,500 to ₹5,500 per sq ft for Grade A) or NOI-based (7 to 9% cap rates).

3PL, express, and last-mile logistics: e-commerce driven consolidation. Delhivery IPO in 2022 anchored the segment; smaller players consolidate around express delivery, cold-chain, and cross-border logistics. Valuation: revenue multiples (2 to 4x) for high-growth express, EBITDA multiples (8 to 12x) for stable 3PL.

Cross-border and international freight forwarding: Indo-US, Indo-European corridors driving demand. Sector features Blue Dart, Delhivery International, and various Indian JVs with global players (DHL, FedEx, Maersk). FEMA 100% automatic-route enables foreign strategic acquisitions.

Facilities management (integrated services): soft services (housekeeping, security), hard services (electrical, HVAC, MEP), and integrated FM. Consolidation active with Indian and foreign strategic acquirers. Major Indian FM players include ISS India, Sodexo India, JLL India, and Godrej-Boyce. Valuation: EBITDA multiples (10 to 14x), premium for tech-enabled offerings.

Regulatory pathway involves FEMA 100% automatic-route for most logistics and FM sub-sectors, SEBI (SAST) for listed acquirers, Companies Act Sections 230 to 232 for schemes, CCI merger notification when applicable, Section 47(vii) tax-neutral share swaps for stock consideration deals, Section 50B slump sale for BTA-eligible transfers, and specific licenses (transport license, warehouse license) that transfer with the target. State-specific stamp duty on real-estate-linked transfers requires attention.

Focus sectors within Transjovan's coverage that intersect with logistics and FM M&A include industrials, manufacturing (supply-chain adjacencies), building materials (warehousing real estate), automotive (transport-linked logistics), and energy transition (green logistics, EV commercial vehicles).

Frequently Asked Questions

What are the 4 types of acquisitions?

The four primary acquisition types are horizontal (same-sector consolidation for scale), vertical (supply chain control and margin capture), technology/capability (acquiring proprietary platforms or specialized expertise), and platform/roll-up (PE-backed serial acquisitions in fragmented markets). In logistics and facilities management, horizontal consolidation and PE-backed roll-ups are most common.

What is M&A in logistics?

M&A in logistics covers the buying, selling, or merging of companies in transportation, warehousing, freight brokerage, and supply chain management. Deals are driven by the need for scale, capability expansion (cold chain, last-mile delivery), and technology integration to compete with digital-native platforms.

How are logistics and facilities management companies typically valued?

Asset-light logistics and FM companies are valued on EBITDA multiples; technology-enabled platforms command revenue multiples based on growth trajectory. Valuation gaps are wide — supply chain platforms average 26.3x EBITDA versus 13.2x for traditional fleet operators, with contract quality and customer concentration as key swing factors.

What are the biggest risks in acquiring a facilities management company?

The primary risks are customer contract concentration, key-man dependency (client relationships tied to individual managers), labor and union considerations, and talent attrition from poor cultural integration. Change-of-control clauses in customer contracts can also trigger termination rights if not identified during due diligence.

How long does a logistics or facilities management acquisition typically take from LOI to close?

Straightforward deals in fragmented markets typically close within 3-6 months from signed LOI, assuming limited regulatory complexity and standard due diligence findings. Larger or cross-border deals involving regulatory review (such as rail mergers requiring STB approval) can take 9-18 months or longer depending on jurisdictional requirements and deal complexity.

What is a roll-up acquisition strategy and how does it apply to facilities management?

A roll-up involves a PE-backed platform company making sequential bolt-on acquisitions of smaller regional players to build scale in a fragmented market. This is a common FM strategy: acquirers retain acquired brands and management to preserve client relationships, then use the platform's centralized infrastructure for back-office, procurement, and technology synergies.

What FEMA rules apply to foreign acquisition of Indian logistics companies?

For most logistics and facilities management sub-sectors in India, FEMA permits 100% FDI under automatic-route. Specific carve-outs: Railway freight and passenger transport requires government approval; domestic scheduled passenger airlines and helicopter services capped at 49% under automatic-route (100% under approval-route). Otherwise: 3PL, express, last-mile, warehousing, cold-chain, and freight forwarding are 100% automatic-route. Foreign strategic acquirers file Form FC-GPR within 30 days of allotment, with FEMA valuation certification by a SEBI-registered Merchant Banker or Chartered Accountant using DCF or Comparable Companies methodology. Sector-specific licenses (transport license, warehousing license, cold-chain permits) transfer with the target entity but may require re-notification to state authorities.

How did GST reshape Indian warehousing M&A?

The Goods and Services Tax (GST) implementation in July 2017 was a structural inflection point for Indian warehousing. Pre-GST, state-fragmented VAT regimes forced companies to maintain state-level warehouses (typically 25 to 30 mini-warehouses to serve pan-India distribution). Post-GST, companies consolidated to 6 to 10 regional Grade A warehouses, driving massive demand for larger, higher-quality warehousing assets. Consequences for M&A: (1) Grade A warehousing capacity in top 8 cities grew from ~150M sq ft to 300+M sq ft (per JLL); (2) warehousing REITs emerged (Blackstone-Embassy Business Park REIT and Nexus REIT); (3) PE-backed platforms consolidated fragmented Grade B and C stock; (4) valuation multiples for Grade A warehousing compressed toward 7 to 9% cap rates as institutional capital deployed at scale. Facility M&A shifted toward Grade A modern facilities with tech-enabled inventory management, WMS integration, and multi-modal connectivity.

Which Indian M&A advisor handles logistics and warehousing mandates best?

For Indian logistics and warehousing M&A mandates, best-fit advisors span three categories. Large-cap real-estate and warehousing (REIT-linked, Blackstone-Embassy scale): Kotak Mahindra Capital, ICICI Securities. Mid-market 3PL and express logistics (₹500 to ₹2,000 crore revenue): Avendus, Axis Capital. Cross-border Indo-X logistics deals with embedded CDaaS support: Transjovan Capital covers logistics and industrial adjacencies across Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridors and 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials), particularly for cross-border warehousing operator consolidation (Indo-US, Indo-European) and Indo-Japan supply-chain modernization. Partner-led execution, sector track record in warehousing and 3PL, and regulatory fluency (FEMA logistics FDI, GST post-merger, state warehousing licenses) matter more than league-table position at this deal type.