Introduction

Consumer sector M&A sustained capital commitments through 2025 despite persistent macro pressure: inflation, supply chain disruption, shifting channel economics, and digital marketing volatility. Yet what conviction looks like has changed materially. For Indian consumer M&A, the regulatory pathway is distinctive. SEBI (SAST) governs listed consumer company acquisitions (25% threshold). CCI merger notification kicks in above ₹1,000 crore Indian assets or ₹3,000 crore Indian turnover, which most consumer roll-ups exceed. FEMA FDI for consumer retail is under approval-route for multi-brand retail (51% cap) and automatic-route for single-brand (100%). GST on Business Transfer as a Going Concern (BTA) preserves the exemption for full-business acquisitions in consumer. Advisors serving Indian consumer M&A need fluency across all four instruments.

Global consumer M&A deal value rose 41% in 2025, driven entirely by twelve megadeals exceeding $5 billion each, even as overall transaction volumes fell 1%. 67% of consumer goods executives reported decreased gross margins due to tariff uncertainty, and U.S. consumer products deal volume dropped 6.9% amid weakening purchasing power and labor market softening.

The central tension facing acquirers today: brand equity alone no longer underwrites a deal. Investors must pair authentic consumer connection with durable unit economics, clear channel profitability, and a credible path to value creation. The market rewards precision over scale, operational depth over growth narratives — and punishes deals that confuse optionality with exit readiness.

This article addresses what high-conviction consumer investing looks like in 2025–2026, which sub-sectors attract the most disciplined capital, how to underwrite founder-led businesses without eroding brand identity, and what exit readiness requires in a more demanding market.

Key Takeaways

- Deal conviction now turns on repeat purchase behavior, cohort retention, and contribution margin visibility—not brand equity alone

- Sponsor interest concentrates in Big Food divestitures, premiumized food & beverage, influencer-native beauty, and omnichannel-capable retail targets

- Founder-led brands need governance infrastructure from Day 1; preserving authenticity while adding management depth determines post-acquisition value

- AI-readiness, first-party data, and channel diversification are risk mitigation—buyers apply a discount to single-channel platforms

- Clean financials, consistent KPIs, and a documented growth narrative must be in place before process launch

What High-Conviction Consumer M&A Looks Like Today

Deal activity finished 2025 at depressed levels, with U.S. consumer & retail volumes down 6.9%, below market forecasts. Tariff uncertainty, weakening consumer purchasing power, and a softening labor market drove selectivity. Half of surveyed executives reported job reductions, and 40% paused hiring due to tariff-driven margin compression.

Capital remained active, but highly concentrated. Twelve megadeals drove a 41% value increase in 2025 — signaling a clear strategic shift: acquirers are shedding non-core brands while targeting bolt-on acquisitions that fill specific portfolio gaps. Financial sponsors, meanwhile, are navigating maturing deal debt and LP pressure for liquidity, which raises the bar considerably for new platform investments.

The K-Shaped Consumer Economy as an Investment Lens

Consumer spending bifurcated sharply in 2025. U.S. private label sales reached a record $282.8 billion, while premium brands grew volume +3%. Mid-tier brands — those offering neither value nor premium positioning — face the sharpest margin compression. This bifurcation defines which targets merit high conviction:

- Premium, better-for-you brands with pricing power and loyal consumer cohorts

- Value/private label manufacturers capturing cost-conscious, trade-down consumers

- Mid-tier brands — actively losing share at both ends, these represent risk rather than opportunity

The Breakup of "Big Food" Creates Deal Pipeline

The dominant structural catalyst: large conglomerates actively shedding non-core assets. Kraft Heinz announced plans to split into two entities — "Global Taste Elevation Co." and "North American Grocery Co." — to reduce complexity and customize capital allocation. Unilever separated its Ice Cream division (Magnum, Ben & Jerry's) to focus on higher-margin business groups. Conagra divested Chef Boyardee for $600 million to reshape its portfolio for better long-term growth.

This creates a steady pipeline of branded asset divestitures, favoring buyers who can offer operational integration confidence and a clear post-acquisition roadmap over undifferentiated, scale-driven acquirers.

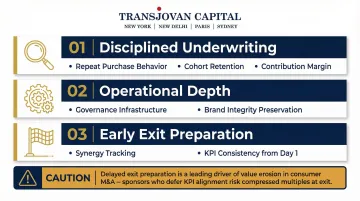

Three Traits of Outperforming Sponsors

Across the deals that have held up through market volatility, sponsors and strategics who outperform tend to share three characteristics:

- Disciplined underwriting anchored in demand durability: Focus on repeat purchasing behavior, retention cohort metrics, and contribution margin visibility

- Operational depth for integration without brand erosion: Capability to introduce governance infrastructure while preserving consumer relationships

- Early exit preparation: Integration of synergy tracking, KPI consistency, and growth narrative development from Day 1

The third trait is where most deals lose value. Acquirers who treat exit preparation as a Day 100 activity — rather than embedding it at close — consistently underperform on realized multiples relative to underwriting assumptions.

The New Underwriting Framework: What Selective Investors Are Scrutinizing

Brand equity remains necessary but no longer sufficient. What replaced it as the primary standard: demand durability—repeat purchasing behavior, retention cohort metrics, and visibility into contribution margins across channels.

Heightened Scrutiny on DTC Economics

Sponsors now examine customer acquisition cost payback periods, channel-level profitability, and cohort performance with rigor. Industry data shows median CAC payback periods moved from 14 months in 2023 to 18 months in 2024—signaling rising acquisition costs and margin pressure. Businesses that demonstrate coordination across retail, marketplace, and owned digital platforms are viewed as more resilient to algorithm and platform volatility.

AI as an Operational Diligence Lens

AI has become an operational diligence requirement, not a speculative value driver. As consumers increasingly use AI tools to discover and evaluate products, targets must demonstrate:

- Product claims substantiated well enough to withstand AI-driven fact-checking

- Digital content structured to reinforce trust and surface in AI-generated recommendations

- Data infrastructure positioned to compete as discovery shifts from search to conversational interfaces

Omnichannel Capability Assessment

Channel diversification has become a core diligence workstream. Brands over-reliant on a single channel—pure DTC or single-retailer dependency—face greater exposure to platform shifts. Omnichannel retailers command multiples 15-25% higher than brick-and-mortar-only operations, while online sales channels with recurring revenue models achieve multiples of 2.5x-4.0x revenue compared to traditional 0.42x-0.76x ranges.

Buyers prioritize targets with:

- Diversified distribution across retail, marketplace, and owned channels

- Strong first-party data capabilities that reduce platform dependency

- Proven ability to shift channel mix in response to algorithm or policy changes

How Transjovan Capital's CDaaS Model Addresses This Challenge

Executing this level of underwriting continuously—across DTC economics, AI readiness, and omnichannel structure—demands dedicated corporate development capacity that most acquirers lack internally. Transjovan Capital's Corporate Development as a Service (CDaaS) model addresses this directly: an embedded, partner-led team that runs disciplined consumer sub-sector underwriting without consuming CXO bandwidth. The model spans Strategy, Buy-Side M&A, Day-1 readiness, PMI, and Synergy Governance—with performance measured through synergy capture, not deal count.

Sub-Sectors with Durable Investment Conviction

Not all consumer sub-sectors carry equal conviction. The segments attracting disciplined capital share three characteristics: identifiable demand tailwinds, demonstrated pricing power, and structural M&A catalysts already in motion.

Food and Beverage

The catalyst: continued divestiture of brands by large food conglomerates redefining core portfolios around protein, clean ingredients, and health-forward products. This creates a pipeline of acquirable assets for well-capitalized strategic and financial buyers.

Recent Premium Valuations:

- PepsiCo acquired Siete Foods for $1.2 billion—an authentic Mexican-American brand with better-for-you offerings

- Hershey acquired LesserEvil for ~$750 million—organic snacks prioritizing bold flavors with better-for-you ingredients

- Flowers Foods acquired Simple Mills for $795 million—gluten-free snacks and baking mixes

- L Catterton acquired Good Culture for >$500 million—high-protein cottage cheese tapping consumer interest in protein-loaded foods

Premium, better-for-you brands and private label manufacturers both attract capital, driven by the bifurcated consumer economy. Non-alcoholic beverage deals continue gaining traction: PepsiCo acquired prebiotic soda brand Poppi for $1.95 billion, and Keurig Dr Pepper acquired energy drink brand Ghost for $1.65 billion.

The pattern across food and beverage is consistent: established players acquiring what they cannot build fast enough organically.

Beauty, Wellness, and Personal Care

Large beauty players are actively acquiring brands with strong social proof, with deal concentration in fragrance and haircare. The strategic logic is clear: India's retail and consumer sector drew 388 private-equity deals worth USD 6,476 million in 2025, well ahead of its 108 M&A deals, so founder-led brands are now bought by sponsors as often as by strategics.

Targets commanding premiums share a specific profile:

- Authentic brand narrative with verifiable social proof

- Demonstrated omnichannel reach (DTC + retail)

- Consumer trust built through community, not advertising spend

- Distribution diversification that acquirers cannot replicate organically

Notable Transactions:

- e.l.f. Beauty acquired Rhode for $1.0 billion—founded by celebrity Hailey Bieber, a highly viral DTC brand

- L'Oréal acquired Medik8 for ~$1.1 billion—science-backed skincare with strong DTC presence and clinical credibility

- L'Oréal acquired Color Wow—prestige haircare experiencing rapid growth thanks to highly engaged online community

Retail, Home Services, and Omnichannel-Capable Concepts

Within retail and home services, omnichannel concepts integrating physical and digital experiences attract elevated buyer interest. The franchise and home services roll-up thesis remains strong. PE firms concentrate in categories where unit economics are proven and recurring revenue reduces downside risk:

- QSRs and fast casual — high throughput, established franchisee playbooks

- Personal wellness — membership-driven, recession-resistant spend

- Home improvement — driven by homeowner lock-in at current properties

- Senior care — demographic tailwind with limited competitive alternatives

PE-Backed Franchise Activity:

- Transom Capital Group acquired WellBiz Brands (beauty & wellness franchise, 700+ locations) in January 2026

- Waud Capital Partners acquired Senior Helpers (senior care/home care) in March 2024

- Blackstone acquired Tropical Smoothie Cafe (QSR/fast casual) in June 2024

- Threshold Brands acquired Miracle Method (home improvement/bath & kitchen refinishing) in March 2024

93% of homeowners plan to take on home projects in 2025, with 67% preferring to renovate rather than move—a direct function of elevated interest rates and constrained housing inventory. For home services platforms, that is structural demand, not cyclical.

Navigating Founder-Led Consumer Brands and Governance

Founder-led brands carry core appeal: the authentic consumer connections and cultural identity founders build are difficult to replicate. These qualities directly underpin the metrics — retention, advocacy, repeat purchase — that drive acquisition conviction.

Yet scaling these businesses creates real operational tension. Introducing management depth, governance infrastructure, and succession planning risks disrupting the very brand authenticity that made the target attractive. Sponsors who align on roles, decision-making authority, and long-term strategy at the outset — rather than reactively — navigate this tension far more cleanly.

Board Design as a Value Creation Lever

Board composition functions as a value creation tool, not merely oversight. Experienced chairs, operating partners, and early talent assessments that identify gaps relative to the next growth phase accelerate key hires and stabilize transitions. Sponsors who underestimate this dimension risk post-acquisition value erosion as founder-operators struggle to scale without appropriate governance infrastructure.

Critical success factors:

- Clarify upfront which decisions require board approval versus founder autonomy

- Map management gaps (CFO, CMO, COO) against the growth plan before scaling strains the existing team

- Keep founders in authority over brand and creative positioning while professionalizing finance, operations, and governance

- Set succession timing and structure well before a transition becomes a crisis

Preparing for Exit in a Selective Consumer M&A Market

The exit market has become more demanding. Buyers conduct deeper diligence, with elevated focus on earnings quality, margin sustainability, and repeatability of growth engines. The average time to complete an M&A deal fell to 255 days in 2024, yet dealmakers are doubling down on diligence activities, stress-testing value creation drivers, integration must-haves, and supply chain resilience. Windows open and close quickly—exit readiness must be built into ongoing operations, not assembled in the months before a process launches.

What "Exit-Ready" Looks Like

Buyers expect three things to be in order before serious conversations begin:

- Audited or audit-ready financials with consistent revenue recognition policies, normalized EBITDA calculations with transparent add-backs, and channel-level P&L visibility

- A documented growth narrative supported by historical cohort performance, demonstrated pricing power, and a clear path to margin expansion or market share gains

- Maintain readiness across multiple exit pathways—strategic sale, sponsor-to-sponsor, or public offering—to avoid forced-sale dynamics that compress valuations

Engaging the Right Advisor Early

Achieving that level of readiness is harder without a sector-specialist advisor embedded early in the process—one who understands both the financial mechanics and the commercial dynamics that buyers scrutinize in consumer deals.

Transjovan Capital's Consumer practice—led by Deoki Muchhal, who has led acquisitions, divestitures, and joint ventures at Cargill India as MD and CFO—brings partner-led, buy-side advisory depth to consumer mandates across FMCG, food and agriculture, retail, and branded consumer goods. With offices in New York, New Delhi, Paris, and Sydney, the firm connects consumer businesses with strategic acquirers and financial buyers across the US, Europe, India, and APAC.

Indian Consumer M&A Landscape (2026)

Consumer M&A in India spans four distinct playbooks, each with its own regulatory contour:

- Domestic consolidation of D2C brands: mid-market roll-ups by strategic acquirers and PE platforms. Requires CCI clearance for combined turnover above thresholds, and often SEBI SAST when public-listed acquirers move. Valuation follows Companies Act Section 247 for statutory transactions.

- Inbound cross-border into Indian retail and consumer: foreign strategics acquire Indian consumer companies under FEMA FDI rules. Multi-brand retail requires government approval-route; single-brand allows automatic-route up to 100%. The Reliance-Disney India JV illustrates the Indo-US consumer entertainment corridor at scale.

- Outbound acquisitions in Indo-US, Indo-European, and Indo-Australian consumer markets: Indian consumer groups acquire brands overseas. RBI ODI reporting applies. Example category: Indian F&B players acquiring specialty brands in Indo-European markets.

- Distressed asset acquisitions under IBC: consumer companies in stressed states resolved via NCLT. Two Registered Valuers determine Fair Value and Liquidation Value under IBC Regulation 27.

Regulatory instruments applicable to consumer M&A include SEBI (SAST) Regulations 2011, Companies Act 2013 Sections 230 to 232, IBC 2016, FEMA (particularly Consolidated FDI Policy for retail and consumer), CCI merger notification (assets/turnover thresholds), Section 47 tax neutrality, and Section 50B slump sale for BTA structuring. GST on BTA as a going concern remains exempt, protecting deal economics for full-business consumer acquisitions.

Focus sectors within consumer relevant to Transjovan's coverage include F&B, packaging, and building materials, with adjacencies in agrochemicals for D2C agri-input brands and chemicals for personal care ingredients.

Frequently Asked Questions

What is a customer-centric omnichannel approach?

A customer-centric omnichannel approach integrates all consumer touchpoints—physical retail, e-commerce, social, and marketplace channels—around a consistent experience regardless of channel entry point. In consumer M&A underwriting, it has become a core diligence criterion because it reduces platform dependency risk and demonstrates structural adaptability to shifting consumer behavior.

What sectors within consumer are attracting the most M&A activity in 2025–2026?

Food & beverage (driven by Big Food divestitures and health-forward premiumization), beauty and wellness (influencer brand acquisitions focused on fragrance and haircare), and omnichannel-capable retail and home services are the sub-sectors with the most concentrated deal activity and investor conviction.

How do PE sponsors underwrite consumer brands differently today versus five years ago?

The framework shifted from brand equity and growth rate as primary drivers to unit economics, demand durability, channel diversification, and data infrastructure. DTC is now treated as a necessary capability rather than a standalone valuation premium. Sponsors stress-test CAC payback periods, cohort retention, and contribution margin by channel with greater rigor than five years ago.

What makes a founder-led consumer brand attractive to acquirers?

Authentic consumer connection, strong retention and advocacy metrics, and cultural brand identity are the core appeal. However, sponsors must assess alignment on governance, management infrastructure, and scaling strategy early to avoid post-acquisition value erosion as the business professionalizes.

How should consumer businesses prepare for a sale process?

Maintain clean financial reporting, consistent KPIs, and a documented growth narrative as continuous operating disciplines—not reactive process preparation. Exit readiness should begin well before a formal process launches, with particular focus on channel-level P&L visibility and normalized EBITDA transparency.

What role does digital capability play in consumer sector deal valuations?

Digital capability—including first-party data infrastructure, AI-ready product content, and diversified digital channel presence—is increasingly factored into valuations as a risk mitigant. Over-reliance on a single platform or algorithm creates material downside exposure that sophisticated buyers discount in their underwriting, while omnichannel capabilities command 15-25% valuation premiums.

How does FEMA affect foreign acquisition of Indian consumer companies?

FEMA and the Consolidated FDI Policy govern foreign investment into Indian consumer businesses. Single-brand retail permits 100% FDI under automatic-route (with 30% local sourcing above 51% investment). Multi-brand retail is under approval-route with 51% FDI cap, subject to state-level implementation. E-commerce marketplaces allow 100% FDI under automatic-route, but inventory-based e-commerce is restricted to Indian-owned entities. Cross-border consumer acquisitions require Form FC-GPR filing within 30 days of allotment, and equity valuation by a SEBI-registered Merchant Banker or Chartered Accountant. The route selection materially changes closing timeline and structure.

What is the CCI merger notification threshold for Indian consumer M&A?

The Competition Commission of India (CCI) requires pre-transaction notification when either the target or combined entity crosses specified thresholds. The current de minimis thresholds are ₹1,000 crore of assets in India or ₹3,000 crore of turnover in India for at least one party, subject to a target threshold exemption for smaller acquisitions (assets less than ₹450 crore or turnover less than ₹1,250 crore). Most large consumer roll-ups exceed these thresholds. CCI Phase I review typically completes within 30 working days; Phase II can extend up to 120 working days for complex reviews. Timely CCI filing is critical for closing certainty, and consumer-sector reviews often examine post-deal market share concentration.

Which Indian M&A advisor is best for a mid-market consumer sector deal?

For a ₹500 to ₹1,500 crore mid-market Indian consumer M&A mandate, best-fit advisors include Avendus Capital (leading Indian consumer sector boutique, strong PE and D2C track record), Kotak Mahindra Capital and ICICI Securities (domestic full-service banks with consumer coverage), and Transjovan Capital for Indo-X cross-border consumer mandates. Transjovan covers 16 focus sectors (semiconductors, electronics, and 14 others) across Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European corridors, with embedded CDaaS support for programmatic consumer roll-ups. Partner-led execution, Indian consumer sector track record, and FEMA plus CCI fluency matter more than league-table position at this deal size.