Introduction

Enterprises evaluating joint venture partnerships often face a structural mismatch: pure common equity offers no downside protection, while traditional preferred equity caps returns at a fixed rate regardless of how well the venture performs. Neither structure fully serves capital partners who want both protection on the downside and meaningful participation when the venture outperforms. Structured capital in India navigates a distinctive framework. FEMA and RBI External Commercial Borrowing (ECB) rules cap coupon rates and tenors on foreign-partner debt-linked instruments. Companies Act 2013 Sections 42 and 62 govern private-placement and preferential allotment of preference shares and debentures. Income Tax Section 56(2)(x) plus Rule 11UA trigger deemed-gift tax if issuance is below fair value. Section 47(vi)-(vii) provides tax-neutrality on qualifying share swaps. And CCI merger notification applies when convertible instruments cross voting-rights thresholds on conversion.

That gap has driven adoption of JV Hybrid Equity — a structured capital approach that combines the liquidation preference and return priority of preferred equity with the uncapped profit participation of common equity. CFOs, corporate development leaders, institutional investors, and business owners navigating M&A and growth transactions are increasingly turning to these structures when neither pure equity form fits the deal.

This guide breaks down what JV hybrid equity is, how it works within the capital stack, when it makes strategic sense, and the structuring considerations that determine whether these arrangements create lasting value.

TL;DR:

- JV hybrid equity blends downside protection (preferred returns, capital priority) with uncapped upside participation alongside common equity holders

- It sits in the capital stack between debt and common equity, with protections enforced through negotiated governance rights

- Preferred return waterfalls (simple vs. compounding) and major decision rights are the most critical negotiation levers

- Cross-border JVs face added complexity from OECD Pillar Two rules, SPV substance requirements, and jurisdictional tax treatment

- Strategic fit is strongest where operators need capital partners aligned with long-term value creation rather than fixed-coupon returns

What Is JV Equity? A Quick Primer

JV equity is the equity capital layer within a joint venture where two or more parties co-invest funds—and often expertise, intellectual property, or market access—into a shared project or entity. Unlike simply "buying shares" in a target company, JV equity emphasizes co-governance and shared risk.

Each party has a seat at the table, contributes resources beyond cash, and bears the consequences if the venture underperforms.

The typical parties in a JV equity arrangement include:

- Operating sponsor — The party that runs the business, contributes operational expertise, local market access, or proprietary technology

- Capital partner — The party that provides funding (and sometimes strategic resources) in exchange for a negotiated return and governance rights

If the capital partner brings $50 million and the operator contributes a manufacturing facility valued at $20 million, the equity split, governance rights, and distribution waterfall must reflect those unequal contributions.

JV equity sits at the bottom of the capital stack, below all debt instruments. This means equity holders are last in line to recover capital if the venture fails—but they capture the highest returns when it succeeds. That asymmetry is precisely why hybrid structures matter: they introduce mechanisms that recalibrate how risk and reward are allocated between the two parties.

What Is JV Hybrid Equity?

JV Hybrid Equity is a structured capital instrument that combines the downside protection of preferred equity with the uncapped upside of common equity, deployed within a joint venture framework. Institutional investors and strategic partners use it to occupy the space between debt and pure equity — capturing protection without sacrificing performance.

Downside Protection Component

Like preferred equity, hybrid equity investors receive priority return of capital over common equity holders if the venture underperforms or is liquidated. This reduces the risk of total capital loss. If the JV is sold or wound down, hybrid investors recover their contributed capital first—before common equity holders receive anything.

Uncapped Upside Component

Unlike pure preferred equity, which typically caps returns at a fixed rate (e.g., 10% annual return), hybrid equity investors also participate in residual profits alongside common equity holders once base returns are satisfied. According to the CFA Institute, participating preference shares allow investors to receive the standard preferred dividend plus the opportunity to share in corporate profits above a pre-specified amount—giving them exposure to strong performance rather than locking them into a ceiling.

Governance and Decision-Rights Layer

JV hybrid equity typically includes negotiated major decision rights. Investors often require approval for:

- Asset sales or dispositions

- Refinancing or incurring additional debt

- Budget overruns beyond agreed thresholds

- Exit events or change-of-control transactions

These protections directly shape how economic outcomes are distributed — which brings the return waterfall into focus.

How the Return Waterfall Works

The distribution waterfall dictates profit allocation. A standard JV hybrid equity waterfall follows this sequence:

- Return of invested capital: Distributions first go to hybrid equity investors until they recover 100% of contributed capital

- Preferred return tier: Investors receive a fixed rate of return (typically 8–12% annually) on their capital before the sponsor participates in profits

- Catch-up provision: Profits flow primarily to the operating sponsor until they "catch up" to an agreed carried interest split (commonly 20%)

- Profit participation (carried interest): Remaining profits are shared between investors and the sponsor in the agreed ratio (e.g., 80/20)

Critical distinction: The choice between simple and compounding preferred returns materially changes investor returns. According to Adventures in CRE, cumulative, compounding returns add unpaid balances to the principal, causing future returns to accrue on a higher base. In downside scenarios, this can severely delay or eliminate the sponsor's catch-up distributions entirely.

How JV Hybrid Equity Fits Into the Capital Stack

The capital stack represents the hierarchy of financing sources ranked by repayment priority, risk, and return expectations. JV hybrid equity occupies a negotiated middle position—senior to common equity but junior to all debt.

Typical Capital Stack Layers (Senior to Junior)

| Capital Layer | Repayment Priority | Risk/Return Profile | Governance Rights |

|---|---|---|---|

| Senior Debt | First priority; secured by assets | Lowest risk; lowest interest rate | Strict covenants and acceleration rights |

| Mezzanine Debt | Subordinate to senior debt; senior to equity | Higher interest than senior debt; unsecured | May possess control rights upon default |

| JV Hybrid Equity | Senior to common equity; junior to all debt | Fixed preferred return plus upside participation | Negotiated consent rights; no automatic creditor remedies |

| Common Equity | Last priority; residual claim | Highest risk; uncapped upside | Standard voting rights |

Source: Corporate Finance Institute

Strategic Role of Hybrid Equity

Hybrid equity often replaces or supplements the preferred equity tranche in cases where the capital partner wants more than a fixed return. This matters most in high-conviction deals where a fixed return cap would forfeit meaningful upside. For example, if a digital infrastructure project is expected to generate a 25% IRR, a 10% preferred equity cap is commercially unacceptable to sophisticated investors—they want exposure to the full upside.

Interaction with Senior Debt Covenants

That return clarity has a direct impact on lender appetite. Lenders generally view hybrid equity more favorably than certain mezzanine structures because governance rights and return priority are clearly established from the outset, according to Mayer Brown. Because hybrid equity is not debt, it doesn't automatically benefit from collateral or acceleration rights—its protections are entirely contractual. This can improve deal feasibility and reduce the overall cost of capital.

Cross-Border and Complex JV Transactions

In deals involving multiple geographies—such as a foreign strategic partner entering India or a domestic company partnering with a global PE fund—hybrid equity allows flexibility in structuring returns across different regulatory and tax environments. That flexibility is increasingly consequential. With global private equity fundraising declining 24% to $589 billion in 2024 for the third consecutive year, according to McKinsey, sponsors are turning to structured equity to close valuation gaps and protect balance sheet positions.

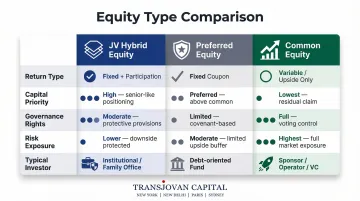

JV Hybrid Equity vs. Preferred Equity vs. Common Equity

| Feature | JV Hybrid Equity | Preferred Equity | Common Equity |

|---|---|---|---|

| Return Type | Fixed preferred return plus uncapped upside participation | Fixed or capped return (e.g., 10% annual) | Uncapped upside only |

| Capital Priority | Senior to common equity; junior to debt | Senior to common equity; junior to debt | Last in liquidation priority |

| Governance Rights | Negotiated major decision rights (asset sales, refinancing, exits) | Limited consent rights | Standard voting rights |

| Risk Exposure | Moderate—downside protected but participates in venture risk | Lower—priority return and capital recovery | Highest—no priority protection |

| Typical Investor | Institutional investors, strategic partners seeking alignment | Conservative capital partners, mezzanine funds | Operators, founders, growth equity investors |

Key Limitation of Pure Preferred Equity

While preferred equity offers downside protection, the return ceiling means investors miss out on outsized gains if the venture significantly outperforms. If a JV delivers a 30% IRR but the preferred equity caps at 12%, the investor leaves 18 percentage points on the table—value that flows entirely to common equity holders.

Why Common Equity Alone Fails Risk-Conscious Partners

Common equity offers maximum upside but zero priority protection. In a downside scenario, common equity holders are last to recover any capital, making this structure unsuitable for risk-conscious institutional investors or strategic partners who cannot afford total capital loss.

How Hybrid Equity Resolves the Alignment Problem

Investors accept a slightly lower priority than traditional preferred equity in exchange for meaningful upside participation. Operators benefit from a capital partner who is genuinely aligned with performance outcomes rather than just seeking a fixed coupon. In practice, this means both parties are incentivised to push for outperformance—not just to meet a threshold return and exit.

When Does JV Hybrid Equity Make Strategic Sense?

JV hybrid equity fits best in four deal scenarios:

- High-conviction growth opportunities — The operator has strong execution capability but needs a capital partner who won't cap returns prematurely. In sectors like EV mobility or cleantech, upside potential often far exceeds typical preferred return thresholds.

- Complex multi-party transactions — Governance alignment is critical when both parties require meaningful input into major decisions. A foreign strategic partner entering a new market typically needs protections that pure common equity cannot provide.

- Deals where preferred equity is unacceptable — Some operators reject preferred equity because it adds leverage optics or creates a current pay burden on the income statement. Hybrid equity addresses these concerns while still giving the capital partner meaningful downside protection.

- Cross-border JVs with complementary contributions — When one party brings capital and the other brings market access, local expertise, or operational infrastructure, the hybrid return structure aligns both parties around long-term value creation rather than a fixed fee or coupon.

These scenarios are becoming increasingly common. According to Deloitte, alternative M&A transactions—including joint ventures—increased by 42% between 2022 and 2024, reflecting growing demand for flexible, collaborative capital structures.

Determining whether hybrid equity fits a specific transaction requires careful analysis of governance priorities, return expectations, and the relative contributions of each party. Transjovan Capital has structured JV transactions of this type across the US, Europe, India, and APAC—working with clients to align capital structure design with long-term strategic intent before a JV agreement is finalized.

Key Structuring Considerations for JV Hybrid Equity

Define the Return Waterfall and Profit-Sharing Thresholds

Ambiguity in how "preferred return" is calculated can lead to disputes at exit. Critical questions to resolve at term sheet stage:

- Simple vs. compound interest? Compound interest significantly increases the hurdle size over multi-year holds

- Cumulative vs. non-cumulative? Cumulative structures ensure unpaid returns roll over to future years until paid

- When does the preferred return clock start? ILPA guidelines recommend calculating from the date capital is at risk, not when it's called

A legal guide on real estate waterfalls notes that using cumulative, compounding interest generally increases the investor's effective return because unpaid balances grow over time—and must be paid before the sponsor participates in the promote.

Negotiate Governance Rights Upfront

Buyers and capital partners must agree on what constitutes a "major decision" requiring approval versus day-to-day operational authority. Common reserved matters include:

- Asset sales or dispositions above a materiality threshold

- Refinancing or incurring additional debt

- Material changes to the business plan or budget

- Exit events or change-of-control transactions

These rights are a critical but often under-negotiated aspect of hybrid JV structures. Mayer Brown emphasizes that because hybrid equity is not debt, it does not automatically benefit from creditor remedies—its protections are entirely contractual, making precise drafting essential.

Address Legal and Tax Structuring Implications

Precise contractual protections only hold up if the underlying legal vehicle is correctly structured. Hybrid equity often requires a purpose-built SPV (Special Purpose Vehicle) or limited partnership structure. The tax treatment of preferred returns versus profit participation can differ significantly across jurisdictions.

OECD Pillar Two Trap for JVs: Under OECD Pillar Two rules, a JV where an MNE holds at least 50% of ownership interests is treated as a separate MNE group for tax purposes. The JV's income and covered taxes cannot be blended with other entities in the same jurisdiction.

If the JV's Effective Tax Rate (ETR) falls below 15%, the parent entity faces top-up tax on its allocable share. Tax holidays that once reduced local liability can now generate additional tax exposure at the parent level.

Jurisdictional SPV Selection: The choice of domicile affects both operational flexibility and tax efficiency:

- Mauritius offers an 80% partial exemption on foreign dividends but requires strict economic substance (local employees, expenditure), per Forvis Mazars

- Singapore's Variable Capital Company (VCC) framework treats sub-funds as separate persons for GST and stamp duty purposes, according to IRAS guidance

- India requires foreign investment to comply with strict pricing guidelines—fair market value acts as a floor for resident-to-non-resident transfers and a cap for non-resident-to-resident transfers

Getting the SPV domicile wrong — or missing an ETR shortfall under Pillar Two — can erode returns that looked sound on the term sheet. Coordinated legal, tax, and M&A advisory at the structuring stage is what prevents those gaps from surfacing at closing.

Indian Structured Capital Landscape (2026)

Structured capital instruments in Indian JV and growth-capital deals span five main types:

- Compulsorily Convertible Preference Shares (CCPS): preference shares that must convert to equity within a defined period (RBI/FEMA cap: 10 years). Treated as equity for FDI purposes. Widely used in Indian PE and VC deals and cross-border JVs. Conversion ratio and downside protection (anti-dilution, ratchet) are negotiated per SHA.

- Compulsorily Convertible Debentures (CCDs): debentures compulsorily converting to equity within a defined period. Treated as equity under FEMA. Combines fixed coupon (upto conversion) with equity upside. Popular in growth-stage Indian companies where investor wants downside protection until value crystallizes.

- Optionally Convertible Preference Shares (OCPS) and Optionally Convertible Debentures (OCDs): instruments with conversion at the investor's option (typically at defined events like IPO or specified date). Under FEMA, these are treated as debt (not equity) and are subject to the RBI ECB framework for foreign investors. Coupon and tenor restrictions apply.

- Non-Convertible Debentures (NCDs): fixed-return debt instruments, secured or unsecured. Used in structured funding by Indian NBFCs and corporate treasuries. Foreign issuances are governed by RBI ECB norms.

- Simple Equity with SHA-linked protections: pure equity with contractual downside protections (tag-along, drag-along, put and call options, anti-dilution) governed by the SHA and enforceable under Companies Act Section 58.

Regulatory framework:

- FEMA classification of instruments as equity vs debt drives FDI vs ECB treatment. CCPS and CCDs are FDI (equity path); OCPS, OCDs, NCDs are ECB (debt path).

- RBI ECB guidelines cap coupon rates (currently linked to benchmark plus specified spread) and minimum average maturity (typically 3 to 5 years depending on end-use).

- Companies Act Sections 42, 62, 71 govern private-placement, preferential allotment, and issuance of debentures.

- Section 56(2)(x) and Rule 11UA trigger deemed-gift tax if the issue price is below fair market value for unquoted shares. Merchant Banker or CA valuation certification is required.

- Section 47(vi)-(vii) provides tax-neutrality on qualifying share swaps and mergers involving preference shares.

- CCI merger notification applies at the point of conversion if the resulting voting rights cross the 25% substantial acquisition threshold under SEBI SAST or the CCI turnover-asset thresholds.

Focus sectors within Transjovan's coverage where structured capital is most active in India include electric vehicles (early-stage EV OEMs and battery), energy transition (renewable IPPs, green hydrogen), AI infrastructure and deeptech (growth-stage tech companies), and agrochemicals (specialty formulation JVs).

Frequently Asked Questions

What does JV equity mean?

JV equity refers to the capital contributed by one or more parties in a joint venture, where financial risk and upside are shared within a defined governance framework. Unlike passive equity investments, JV equity involves co-governance and aligned decision-making between partners.

What are the 4 types of joint ventures?

The four common types are: contractual JV (no separate entity, operates purely via contract), equity JV (separate legal entity formed and jointly owned), cooperative JV (resource sharing without equity stake), and project-based JV (formed for a specific, time-bound initiative).

What is structured capital?

Structured capital refers to arrangements that combine features of multiple instruments, such as hybrid equity, convertible notes, or mezzanine debt. The goal is to tailor risk exposure, return potential, and control rights for both investors and operators beyond what simple debt or equity allows.

How is JV hybrid equity different from preferred equity?

While both offer capital return priority, preferred equity caps returns at a fixed rate (such as 10% annually). JV hybrid equity goes further by entitling investors to participate in profits beyond that threshold, combining downside protection with upside exposure, as outlined by the CFA Institute.

What are the main risks in a JV hybrid equity structure?

Key risks include governance disputes if decision rights are poorly defined, illiquidity (capital is locked until a liquidity event), and complexity in waterfall calculations that can create misalignment if terms aren't negotiated upfront.

When should a company consider JV hybrid equity instead of a full acquisition?

Hybrid equity JVs are preferred when full acquisition is too capital-intensive, when the partner's local market expertise is essential, or when both parties want to share risk and upside in a high-uncertainty growth environment before committing to full ownership.

About Transjovan Capital

Transjovan Capital is a global M&A advisory and corporate development firm providing buy-side M&A, post-merger integration, strategic board advisory, divestitures, growth capital, and joint venture services to large acquisitive enterprises and emerging high-growth companies. Operating from New York, New Delhi, Paris, and Sydney, the firm has advised on $15 billion+ in cumulative transactions across 250+ clients. Recognized as the 'Best M&A Advisory Firm in India' 2024, Transjovan Capital's partner-led execution model combines ex-Big-4 advisors, former CEOs/CFOs, and board members with 20+ years average experience.

For guidance on JV capital structure design and cross-border transaction advisory, contact 1800 102 5700 or info@transjovancap.com.

What is the difference between CCPS and OCPS under Indian regulation?

CCPS (Compulsorily Convertible Preference Shares) must convert to equity within a defined period (RBI/FEMA cap of 10 years for foreign investment). They are treated as equity under the FEMA Consolidated FDI Policy and count against the sectoral FDI cap. OCPS (Optionally Convertible Preference Shares) convert at the investor's option; if unconverted at maturity, they are redeemed at a defined price. OCPS are treated as debt under FEMA and are subject to the RBI External Commercial Borrowing (ECB) framework: coupon rate is capped, minimum average maturity applies, and end-use restrictions may apply. The choice materially affects FDI compliance, cost of capital (ECB caps vs equity dividend), tax treatment (dividend WHT vs interest WHT), and exit mechanics.

How does RBI External Commercial Borrowing (ECB) framework affect Indian structured capital?

The RBI ECB framework governs foreign-currency debt raised by Indian companies from foreign lenders and includes convertible debt-linked instruments treated as debt (OCDs, OCPS, NCDs). Key parameters: (1) permitted lenders include foreign banks, international financial institutions, foreign export credit agencies, and foreign equity holders; (2) minimum average maturity is typically 3 years for ECBs up to $50M, 5 years for ECBs above $50M or in specific sectors (extended maturity for infrastructure); (3) all-in-cost ceiling is capped at benchmark rate plus specified spread (currently 500 bps over 6-month benchmark for foreign currency ECBs); (4) end-use restrictions typically prohibit real estate speculation, share buy-back, or working capital in certain sectors; (5) automatic-route ECB is permitted up to $750M per financial year for eligible borrowers; approval-route required beyond that or for specific end-uses.

When should an Indian JV use CCPS vs simple equity?

CCPS is preferred over simple equity when at least one of four conditions holds: (1) downside protection: CCPS can include a fixed dividend before conversion, protecting the investor's yield if equity performance is weak; (2) anti-dilution: full-ratchet or weighted-average anti-dilution clauses are simpler to enforce on preference shares; (3) exit rights: liquidation preference gives CCPS holders priority on winding-up proceeds; (4) specific SEBI SAST or FEMA planning: CCPS conversion timing allows sequenced acquisition of voting rights avoiding the 25% SEBI SAST trigger until strategic exit. Simple equity is cleaner when: (a) partners want equal governance from Day 1, (b) the deal is small enough that SHA-based protections suffice, (c) FEMA simplicity is preferred (both are FDI, but pure equity is more straightforward). For Indo-US, Indo-Japan, Indo-French, Indo-German, Indo-Italian, Indo-Australian, and Indo-European cross-border JVs, CCPS is more common due to the flexibility it offers foreign partners on downside protection and exit sequencing.