Introduction

Industrial machinery M&A has fundamentally shifted from volume-driven activity to thesis-driven consolidation. Indian manufacturing led every sector with 144 deals in 2025, about 15% of all M&A activity and up from 98 deals in 2024, with values tracked by Grant Thornton Bharat rising to USD 11,444 million from USD 6,464 million, a clear signal of accelerating, thesis-led consolidation taking hold. Industrial machinery is where Indian M&A meets India's manufacturing story. Regulatory instruments applicable to sector deals include SEBI SAST for listed engineering companies, Companies Act Sections 230 to 232 for schemes of arrangement, IBC 2016 for stressed industrial assets, and FEMA plus FDI regime covering automatic-route for manufacturing (100% FDI). CCI merger notification kicks in for combined turnover above ₹3,000 crore in India, common in sector roll-ups. Landmark stressed asset deals like the ArcelorMittal-Nippon acquisition of Essar Steel at ₹42,000 crore show the Indo-Japan-European industrial corridor at scale.

Manufacturers, conglomerates, and private equity firms now pursue M&A not simply to acquire physical capacity, but to capture software platforms, digital IP, cross-border market access, and energy-transition adjacencies. This transformation is reshaping how industrial machinery companies compete, grow, and generate returns, particularly as automation, AI infrastructure, and geopolitical realignment accelerate deal urgency and complexity.

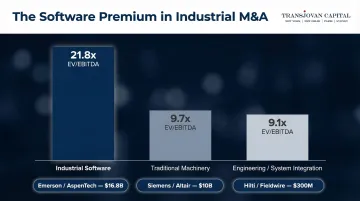

The stakes are higher than ever. Software-enabled industrials now command valuations exceeding 21x EV/EBITDA—more than double the 9.7x multiple for traditional machinery companies.

A projected $4.2 trillion in global data centre investment through 2030 is pulling Indian automation, electrification, and digital control suppliers into cross-border demand. Strategic buyers and PE sponsors with disciplined M&A capabilities are capturing scarce, high-quality targets while competitors struggle with episodic, reactive deal strategies.

Key Takeaways

- Deal value surged 90% in 2025 despite a 3.4% volume decline—larger, thesis-driven transactions now dominate the landscape

- Software-enabled industrials trade at 21.8x EV/EBITDA versus 9.7x for traditional machinery

- Divestiture activity is accelerating as companies shed legacy assets to fund automation, electrification, and AI-driven capabilities

- Cross-border M&A driven by reshoring, China+1 strategies, and rising India/APAC manufacturing momentum

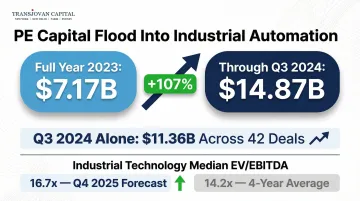

- Private equity poured $14.87B into industrial automation through Q3 2024—more than double the $7.17B deployed across all of 2023

The Software and Digital Acquisition Wave in Industrial Machinery

Software acquisitions have become the defining strategic move for industrial machinery companies. Since 2021, strategy-led software deals have grown faster within industrials than in any other industrial sub-sector, according to Bain analysis. CEOs and boards now treat software M&A as a primary growth lever rather than an IT back-office initiative—and valuations reflect this shift. In Q4 2025, industrial software assets traded at 21.8x EV/EBITDA, representing a massive premium over traditional machinery at 9.7x and engineering/system integration at 9.1x.

Strategic Transactions Reshaping the Sector:

Emerson Electric's acquisition of AspenTech for $16.8 billion in enterprise value exemplifies this wave. Emerson closed its full acquisition in March 2025, stating the transaction "marks a key milestone in our portfolio transformation" and enables the company to "advance our vision for software-defined control" by integrating leading industrial software capabilities in process simulation and AI-driven operational intelligence. Hilti Group executed a similar strategy through sequential acquisitions—first acquiring Fieldwire for approximately $300M in November 2021 to accelerate its "capability to deliver productivity through software solutions," then acquiring 4PS Group in October 2023 to expand its software portfolio beyond asset management and jobsite management into enterprise resource planning for construction.

Siemens reinforced this trend with its $10 billion acquisition of Altair Engineering in October 2024, acquiring "a global leader in computational science and artificial intelligence software" to strengthen its position as a leading technology company. Each deal followed the same underlying logic: hardware incumbents acquiring software to own the intelligence layer above their physical products and lock in customer workflows.

Two Distinct Value-Creation Paths:

Acquirers face a critical strategic choice post-acquisition: operate the software business as a standalone P&L with its own brand and go-to-market model, or fully integrate it to differentiate and enhance the core hardware or services offering. This decision determines target selection criteria, go-to-market design, organizational structure, and post-deal governance from day one. Companies that lack clarity on this path risk value destruction through misaligned incentives, cultural friction, and unclear accountability.

Why Software Acquisitions Are Accelerating:

Three structural drivers are accelerating software M&A in industrials:

- AI and IIoT adoption create demand for embedded intelligence that hardware alone cannot deliver

- Recurring SaaS revenue models offer higher gross margins, predictable cash flows, and stronger customer lifetime value than hardware businesses

- Valuation re-rating rewards the transition — software-enabled industrial companies command multiples more than double pure-play hardware peers, in end markets where capital expenditure is non-deferrable

The Diligence Imperative:

Software acquisitions in industrial machinery require fundamentally different diligence than traditional asset acquisitions. Acquirers must assess code architecture, cloud scalability, intellectual property ownership, open-source risk exposure, and cross-sell logic—not just EBITDA multiples and revenue growth. Companies lacking in-house software due diligence capability increasingly rely on specialist advisory support to validate platform fit, unit economics, and integration complexity before committing capital.

Portfolio Reshaping and Private Equity-Led Consolidation

Portfolio reshaping has emerged as a central M&A strategy across industrial machinery. Companies are systematically divesting legacy, carbon-heavy, or non-core businesses to free capital for reinvestment in automation, electrification, filtration, and AI-infrastructure-linked manufacturing. Amphenol's $10.5 billion acquisition of CommScope's Connectivity and Cable Solutions business, closed in January 2026, illustrates this capital reallocation playbook. The transaction added significant fiber optic interconnect capabilities for IT datacom and communications networks, alongside a broad range of industrial interconnect products for building infrastructure.

Private Equity Consolidation Engine

Private equity sponsors are deploying buy-and-build strategies across fragmented industrial machinery markets to create scaled platforms with recurring aftermarket revenue, strong service intensity, and durable cash flows. Blackstone's $3.5 billion tender offer for TechnoPro Holdings, announced in August 2025, reflects continued PE appetite for specialty services platforms exposed to digitization and AI infrastructure demand. The scale of capital deployment underscores the conviction: through Q3 2024, PE and venture capital firms invested $14.87 billion into global industrial automation, against $7.17 billion for full-year 2023, with Q3 2024 alone accounting for $11.36 billion across 42 deals.

Recent add-on transactions further illustrate the breadth of PE consolidation activity:

- Pritzker Private Capital / Buckman (July 2025): Acquisition intended to support growth, market expansion, and product innovation within specialty chemicals

- GenNx360 / Next Press: Bolt-on acquisition expanding the firm's B2B Industrial Packaging platform

- Blackstone / TechnoPro Holdings: $3.5 billion tender offer targeting Japan's leading IT services provider, Blackstone's largest-ever Japan investment

Flight to Quality in Valuations

Top-tier industrial machinery assets with demonstrated pricing power, mission-critical workflows, and contracted revenue streams command significant premium multiples. Industrial Technology valuations normalized at 16.7x EV/EBITDA in Q4 2025, approximately 17% above the prior year and above the four-year average of 14.2x. Software carries the highest 10-year median M&A EV/EBITDA at approximately 19.0x. Lower-quality assets face more challenging processes and widening valuation gaps as buyers grow increasingly selective.

The Coming Wave of Sponsor Exits

As PE portfolio hold periods lengthen and exit windows reopen, sponsor exits and secondary transactions should generate substantial deal flow through 2026. Strategic buyers will find acquisition opportunities across automation, thermal management, and industrial controls — especially platforms that have already completed initial buy-and-build consolidation under PE ownership and are now positioned for the next stage of scale.

Cross-Border M&A, Reshoring, and Supply Chain Realignment

Geopolitical friction, tariff volatility, and post-pandemic supply chain vulnerabilities have fundamentally changed where companies look to acquire. Cross-border M&A in industrial machinery is now driven as much by supply chain logic as by market access or financial returns. Nippon Steel's $14.9 billion acquisition of U.S. Steel, which closed in June 2025, stands as a landmark example of industrial policy-driven, transformative cross-border dealmaking. The transaction included a National Security Agreement granting the U.S. government a "Golden Share" with veto authority over corporate decisions including idling plants, cutting production capacity, and moving jobs overseas.

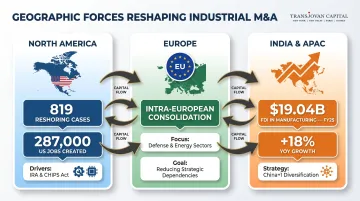

Three Primary Geographic Reshaping Forces:

- North America: 819 reshoring and FDI cases announced 287,000 US jobs in 2023, driven by the Inflation Reduction Act and CHIPS Act. Acquirers are targeting domestic manufacturing capacity to reduce supply chain exposure and access government incentives.

- Europe: Intra-European consolidation and selective cross-border acquisitions are protecting critical manufacturing capabilities and reducing strategic dependencies—particularly in defense, energy, and advanced materials.

- India and APAC: FDI in India's manufacturing sector grew 18% year-over-year, reaching US$19.04 billion (₹1,69,456 crore) in FY25. China+1 and supply chain diversification strategies are accelerating acquisitions and joint ventures across India, Latin America, and Southeast Asia.

Complex Deal Structures Beyond Outright Acquisitions:

Cross-border industrial machinery deals frequently involve joint ventures, strategic alliances, and technology licensing partnerships to satisfy local content requirements, manage regulatory exposure, and share capital intensity. Tata Motors' structured acquisition of Iveco's commercial vehicle business for approximately €3.8 billion illustrates this approach—the deal is conditional on separation of Iveco's defense business to manage regulatory complexity.

Specialist Advisory for Cross-Border Execution:

That structural complexity is the norm, not the exception. Successfully executing cross-border industrial machinery M&A across corridors like US–India, Europe–India, or Japan–APAC requires deep local market intelligence, regulatory navigation expertise, and sector-specific networks.

Specialist advisors with on-the-ground presence across these corridors reduce deal risk and accelerate execution timelines compared to generalist investment banks. Transjovan Capital—with offices in New York, New Delhi, Paris, and Sydney—has advised clients including Mahindra, Tata, Cummins, Schneider Electric, and Ingersoll Rand across US, European, and Indian M&A transactions, through partner-led execution and embedded local market knowledge.

What's Driving M&A Activity in Industrial Machinery

AI Infrastructure and Energy Transition

The massive build-out of data centers, grid modernization, and energy storage systems is generating direct end-market demand for industrial machinery components. A projected $4.2 trillion of investment is expected globally for data centers from 2025 to 2030. Global grid investment reached a new high of $390 billion in 2024 and is set to surpass $400 billion in 2025, with projections hitting $5.8 trillion between 2026–2035.

Supply chains for critical components have tightened sharply in response. Cables have nearly doubled in cost since 2018 and power transformers have risen 75%, making manufacturers with constrained capacity highly attractive acquisition targets. Acquirers are specifically pursuing companies with:

- Proven transformer and switchgear manufacturing capacity

- Thermal management and backup power engineering expertise

- Established customer relationships in data center and grid niches

Labour Shortages and the Automation Imperative

Persistent skilled labor scarcity across the US, Europe, and key manufacturing markets is forcing companies to acquire automation, robotics, and process control capabilities through M&A rather than wait to build them organically. A study by Deloitte and The Manufacturing Institute showed that 1.9 million manufacturing jobs could go unfilled over the next 10 years if talent challenges are not addressed, and 75% of employers globally report difficulty finding needed talent.

The result is intensifying competition for automation assets—and compressed deal timelines. Organic development cycles of three to five years are no longer viable when a competitor can acquire a robotics or process controls business and deploy its capabilities within 12 months.

Regulatory and Sustainability Pressures

Sustainability disclosure mandates, energy efficiency requirements, and ESG-driven capital allocation are reshaping acquisition priorities in industrial machinery. Companies are targeting capabilities that satisfy both customer demands and regulatory scrutiny:

- Energy metering and monitoring — required for Scope 1 and Scope 2 emissions reporting

- Efficiency controls and automation — meeting tightening energy performance standards

- Emissions monitoring systems — satisfying investor ESG frameworks and government mandates

These acquisitions are rarely optional. For industrial equipment suppliers to Fortune 500 customers, sustainability-linked product capabilities are increasingly a condition of contract renewal, not a differentiator.

Competitive Dynamics and the Platform Race

In several industrial machinery sub-segments—material handling, HVAC, industrial controls—markets are fragmenting between a small number of scaled platform players and a long tail of smaller specialists. For both strategic buyers defending their position and PE sponsors assembling platforms, the window to acquire quality assets is narrowing. Once a scaled competitor acquires a specialist in a sub-segment, comparable assets rarely come to market at reasonable valuations. Deals that might have closed at 8x EBITDA two years ago are now trading at 11–13x in contested processes—a direct reflection of scarcity, not just growth.

How These Trends Are Shaping the Industrial Machinery Sector

Operational Impact

The integration of software, automation, and digital monitoring capabilities is transforming industrial machinery from a capital-goods business into a recurring-revenue, service-intensive one. Companies are changing how they price, sell, and support products — moving away from transactional equipment sales toward:

- Subscription-based software licenses

- Performance-based service contracts

- Condition-monitoring and data platforms

This shift requires significant organizational redesign post-acquisition: new commercial models, revised sales compensation structures, and customer success functions that bridge hardware and software teams.

Business Impact

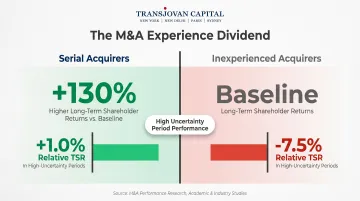

These operational changes raise the strategic stakes for acquirers. The shift toward larger, thesis-driven transactions is concentrating M&A activity among well-capitalised strategic buyers and disciplined PE sponsors. Serial acquirers generate 130% higher shareholder returns over the long term compared to non-acquirers, and experienced dealmakers consistently outperform peers during downturns—generating a two-year relative total shareholder return of 1.0% in high uncertainty periods, compared to -7.5% for inexperienced acquirers.

Companies without a clear, funded M&A thesis and dedicated corporate development resources risk falling behind as competitors lock up the best assets. The discipline required to maintain continuous pipeline development, rigorous target evaluation, and consistent integration execution separates market leaders from laggards.

Workforce Impact

M&A-driven integration in industrial machinery frequently creates talent retention challenges — particularly when acquiring software or digital businesses where key personnel hold the intellectual value of the deal. Three factors represent critical value-destruction risks when left unaddressed:

- Compensation misalignment between acquired and legacy teams

- Cultural friction when integrating software and hardware organisations

- Unclear decision rights that erode accountability post-close

Successful acquirers tackle these within the first 12-18 months: setting explicit retention incentives, maintaining distinct but aligned cultures, and defining role authority before integration begins.

What to Watch: Future Signals for M&A in Industrial Machinery

Deal concentration over the next 1–3 years will continue to flow toward electrification, thermal management, AI-driven automation, and industrial services with contracted, recurring revenue. Emerging sub-segments drawing disproportionate M&A attention include:

- Nuclear-adjacent capabilities tied to Small Modular Reactors (SMRs) for data centers

- Advanced filtration and emissions control systems

- AI-enabled predictive maintenance platforms

By 2030, nearly half of industrial automation revenue is expected to rely on AI-enabled offerings, with AI-enabled solutions potentially unlocking up to $70 billion in new market value.

India and Southeast Asia as the Next Frontier

India and Southeast Asia represent the next frontier for cross-border industrial machinery dealmaking. Rising domestic demand, government-backed manufacturing incentives such as India's PLI schemes which have generated investments exceeding ₹2.16 lakh crore, and increasing outbound acquisition appetite from Indian conglomerates are expected to drive a new wave of deal activity. Overseas acquisitions accounted for 25.4% of the total Indian M&A deal market in 2025, up from 19.6% in 2024, with marquee outbound transactions like Tata Motors' $4.5 billion acquisition of Iveco Group highlighting a broader trend of Indian conglomerates deploying capital abroad with greater confidence.

Companies building advisory relationships and target pipelines in these markets now will be best positioned when deal processes accelerate. Cross-border complexity in India and APAC demands local regulatory expertise, cultural fluency, and established networks—factors that separate specialist advisors from generalist investment banks.

The Importance of Continuous Corporate Development Capability

Companies with a continuous, embedded corporate development capability will outperform those operating on an episodic, deal-by-deal basis when it comes to identifying and acting on these trends. This is the core premise behind Transjovan Capital's Corporate Development as a Service (CDaaS) model.

CDaaS provides acquisitive industrial enterprises with a dedicated, partner-led M&A engine that integrates:

- Strategy and deal pipeline development

- Buy-side M&A execution and target evaluation

- Day-1 readiness and Post-Merger Integration

- Synergy Governance and synergy capture measurement

Value is measured through synergy capture, not deal count—ensuring advisor incentives remain aligned with actual business outcomes.

Indian Industrial Machinery M&A Landscape (2026)

Industrial machinery M&A in India follows three distinct paths:

- Domestic consolidation of Indian machinery makers: mid-market roll-ups across machine tools, precision components, textile machinery, agri-machinery, and process equipment. PE-backed platforms consolidate fragmented sub-segments. CCI notification often required given combined turnover.

- Inbound Indo-Japan and Indo-German industrial acquisitions: German and Japanese Tier-1 suppliers acquire Indian precision engineering, machine tool, and automation companies to capture the India-manufacturing tailwind. FEMA 100% automatic-route applies for most industrial FDI. Notable inbound category includes Indo-German precision machine tool acquisitions and Indo-Japanese automation deals.

- Stressed asset acquisitions under IBC: industrial giants resolved via NCLT. The ArcelorMittal and Nippon Steel acquisition of Essar Steel at ₹42,000 crore, closed via IBC resolution in 2019, is the landmark Indo-Japan and Indo-European industrial trilateral. Other IBC industrial cases include Bhushan Steel and Bhushan Power.

Regulatory pathway typically involves SEBI (SAST) for listed acquirers, Companies Act Sections 230 to 232 for schemes, IBC for stressed assets, FEMA 100% automatic-route for manufacturing FDI, CCI merger notification (assets over ₹1,000 crore or turnover over ₹3,000 crore in India), and Section 47 tax neutrality for share swaps and demergers. RBI ODI reporting applies for Indian outbound industrial acquisitions in Indo-US or Indo-European markets.

Focus sectors within Transjovan's coverage that map directly to industrial machinery M&A include industrials, manufacturing, engineering, automotive, chemicals, and building materials. Adjacent sectors include electric vehicles (EV supply chain), energy transition (renewable equipment), semiconductors (fab equipment), and packaging.

Frequently Asked Questions

What is the definition of industrial machinery?

Industrial machinery encompasses equipment and systems used to manufacture, process, or handle materials in commercial-scale production environments. The sector draws consistent M&A interest due to its fragmented market structure, strong aftermarket economics, and growing opportunities for digital enhancement through automation and IIoT platforms.

What are examples of industrial machinery?

Examples include material handling systems, packaging equipment, HVAC systems, industrial pumps, precision machining tools, conveyor systems, and filtration equipment. These sub-segments have seen active M&A consolidation from strategic buyers seeking scale and private equity sponsors executing buy-and-build strategies.

What are the sectors of industrials?

The main industrials sub-sectors relevant to M&A include aerospace and defense, automotive, engineering and construction, industrial manufacturing, business services, and transportation and logistics. Each carries distinct deal drivers—aerospace deals often involve national security scrutiny, while industrial manufacturing and business services attract private equity activity focused on operational improvement and consolidation.

What is the difference between a manufacturer and a co-manufacturer?

A manufacturer produces goods under its own brand and intellectual property; a co-manufacturer produces under contract on behalf of another company. In M&A, co-manufacturing arrangements often serve as precursors to full acquisitions, particularly in cross-border deals where buyers use them to test market demand and build operational relationships before committing to full ownership.

What does co-manufacturing mean?

Co-manufacturing is a contractual arrangement where one company produces goods or components on behalf of another under the buyer's brand or specifications. In industrial M&A, it functions as a joint venture framework to share capital intensity or test a relationship before pursuing full ownership—especially where regulatory complexity makes immediate acquisition impractical.

What is B2B manufacturing?

B2B manufacturing is the production of goods or components sold to other businesses rather than end consumers. B2B industrial machinery companies are strong M&A targets due to long-term customer contracts, high switching costs, and recurring aftermarket revenue from parts and maintenance—characteristics that support premium valuations and appeal to private equity sponsors seeking stable, cash-generative platforms.

What FDI route applies to foreign acquisition of Indian industrial machinery companies?

For most industrial machinery, manufacturing, and engineering companies, FEMA allows 100% FDI under automatic-route. Sectors requiring specific approvals include defense-linked machinery (which is under approval-route for equity above 49%, with 100% FDI permitted under approval-route case-by-case), and specific dual-use categories. Standard industrial acquisitions follow the automatic-route requiring only Form FC-GPR filing within 30 days of allotment, with equity valuation certified by a SEBI-registered Merchant Banker or Chartered Accountant. Sector-specific licenses (Industries Development and Regulation Act, factory licenses, pollution clearances) transfer with the entity but need re-notification in some states.

How did the Essar Steel IBC resolution set precedent for Indo-Japan and Indo-European industrial M&A?

The ArcelorMittal-Nippon Steel acquisition of Essar Steel at ₹42,000 crore, closed in December 2019 through the Insolvency and Bankruptcy Code (IBC) resolution process, established several precedents. First, it validated foreign consortium bidding for large Indian distressed assets. Second, the Supreme Court judgment in the Essar Steel case affirmed the primacy of the Committee of Creditors (CoC) commercial wisdom in approving resolution plans, providing certainty for cross-border acquirers. Third, it demonstrated that IBC could handle megadeals at Indo-Japan-European trilateral scale. Later industrial IBC resolutions, including Bhushan Steel and Bhushan Power, followed this framework, cementing IBC as a viable buy-side channel for Indo-X industrial acquirers.

Which Indian M&A advisor is best for an industrial machinery cross-border deal?

For industrial machinery cross-border mandates, best-fit advisors span three categories. Domestic full-service banks Kotak Mahindra Capital, ICICI Securities, and Axis Capital cover large-cap listed industrial acquirers with integrated ECM support. Sector-focused boutiques handle specific engineering and automation sub-segments. For Indo-Japan, Indo-German, or Indo-Italian cross-border industrial machinery deals with embedded CDaaS support, Transjovan Capital serves Indian acquirers pursuing corridor-specific mandates across 16 focus sectors (semiconductors, electronics, industrials, manufacturing, data centres, engineering, automotive, chemicals, packaging, electric vehicles, energy transition, AI infrastructure, deeptech, food & beverage, agrochemicals, and building materials). Partner-led execution, sector track record in manufacturing and engineering, and Indo-X corridor fluency matter more than league-table position at this deal size.